Summary

- The domestic gold price ended 5.2% lower in March at Rs43,994/10g1

- A lower domestic gold price, and wedding season purchases boosted retail demand during the month, measured against the low sales base from March 2020

- Indian official imports were highest in a decade and the local market premium hit a 51-month high in the first week of the month

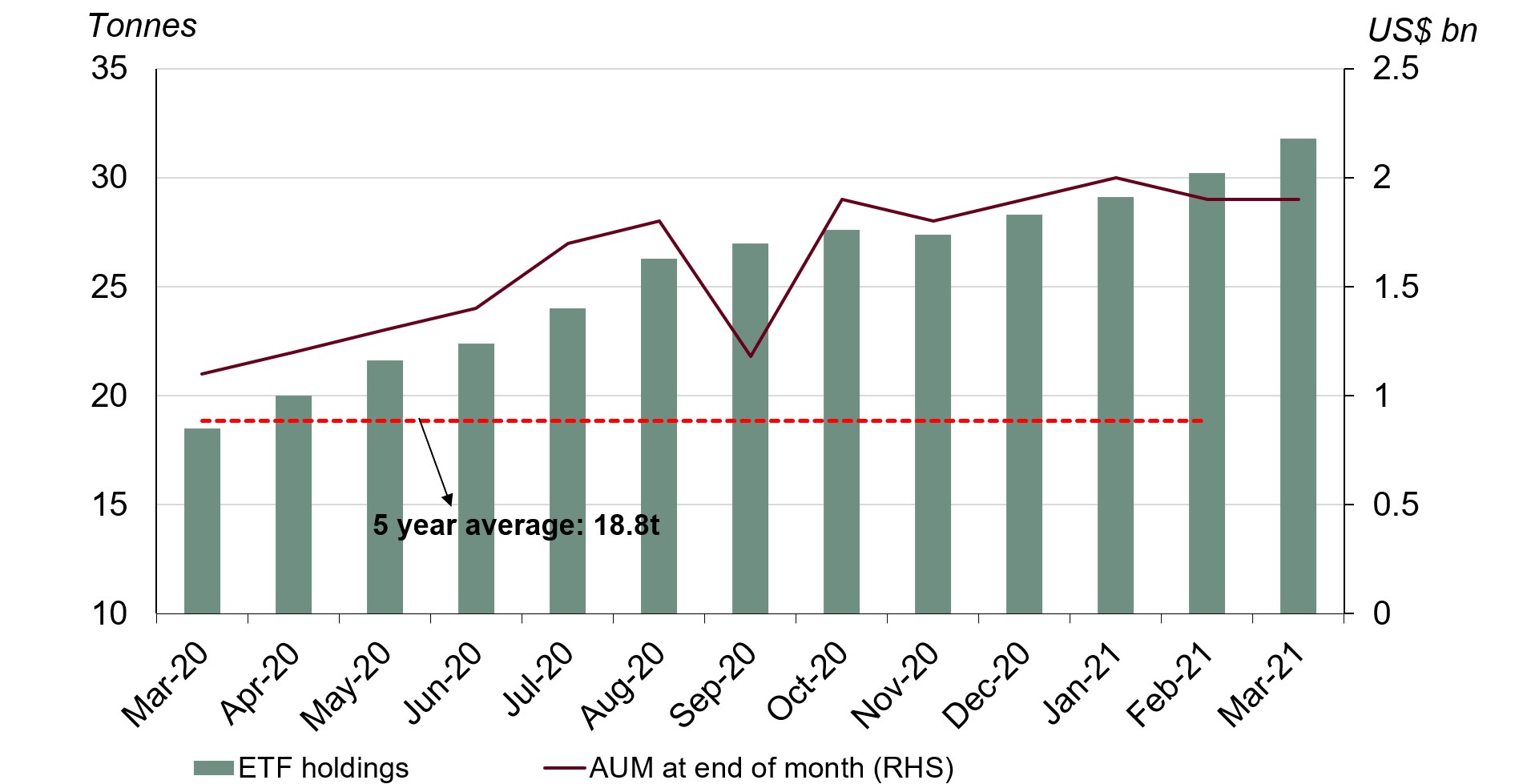

- The lower gold price, higher domestic gold price volatility and safe-haven demand led to ETF inflows. Total holdings for Indian gold-backed ETFs (gold ETFs) reached 31.8t by the end of March; a net inflow of 1.6t

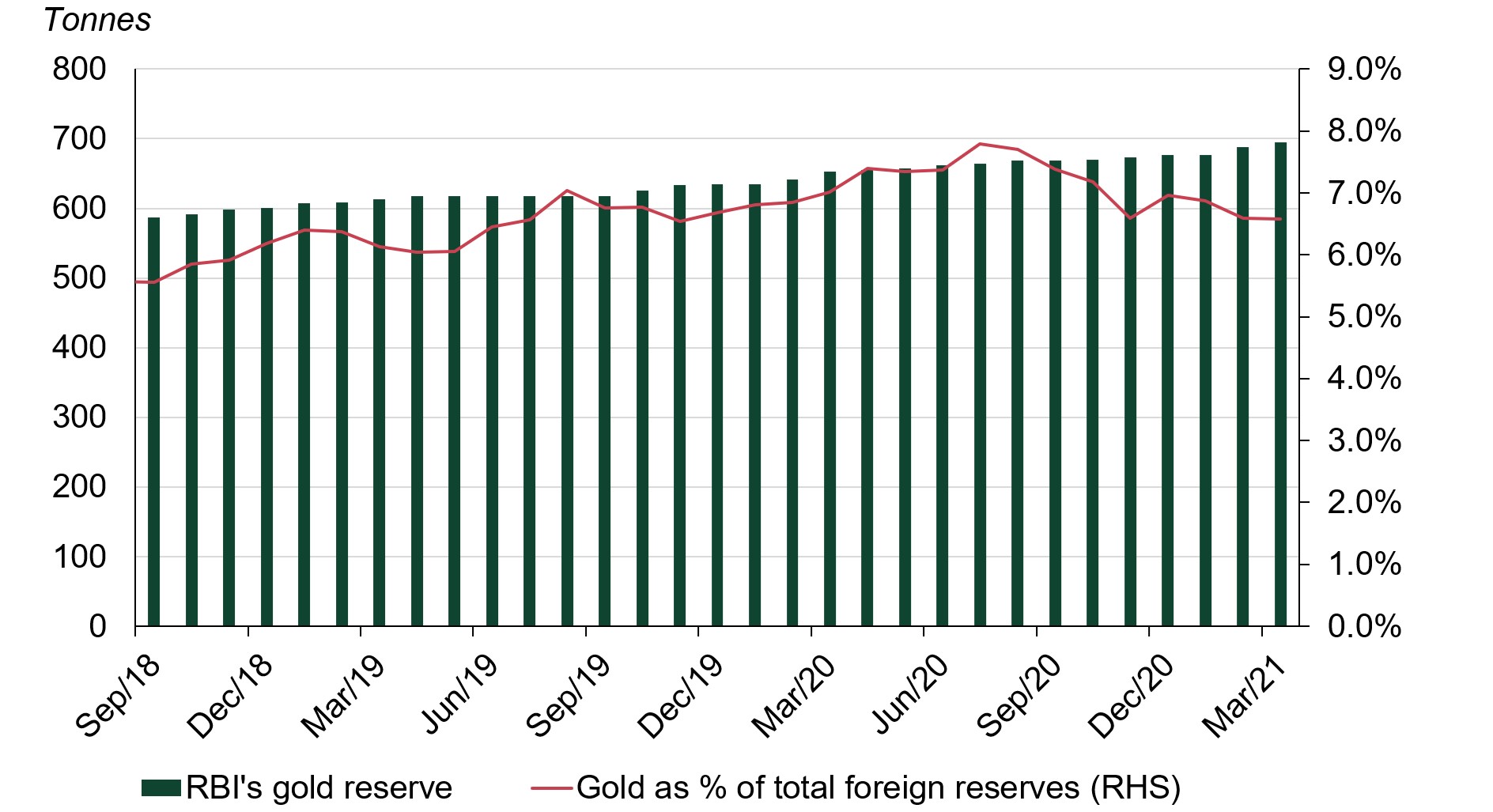

- The Reserve Bank of India (RBI) added 7.5t of gold to its reserves, taking its total gold reserves to 695.3t.

Gold prices corrected in March

The US 10-year bond yield rose by 34bps during the month to end at 1.74%, while the US dollar strengthened by 2.6% to 93.2. The rising bond yields and stronger dollar index pushed down both the LBMA Gold Price AM and MCX Gold Spot (Chart 1).2

Chart 1: Gold prices declined in March

Domestic gold price in rupees vs LBMA Gold Price AM in US dollars

Indian government bond yields fell across various tenures

The 10-year Indian government bond (G-sec) declined marginally by 6 bps compared to a rise of 32 bps in February, whilst rates along the medium maturities (3-5 years) have seen a fall of 6-40 bps compared to a much larger spike (90-100 bps) last month. Bond yields have declined in the month mainly due to the RBI’s actions, such as the so-called Operation Twist and the devolvement of two auctions, ensuring G-sec yields will likely not go much higher in the near future (Chart 2).3 The RBI intends to keep a lid on bond yields so that government borrowing cost is lower to support the economy.

Chart 2: Indian government bond yields declined across various tenures in March

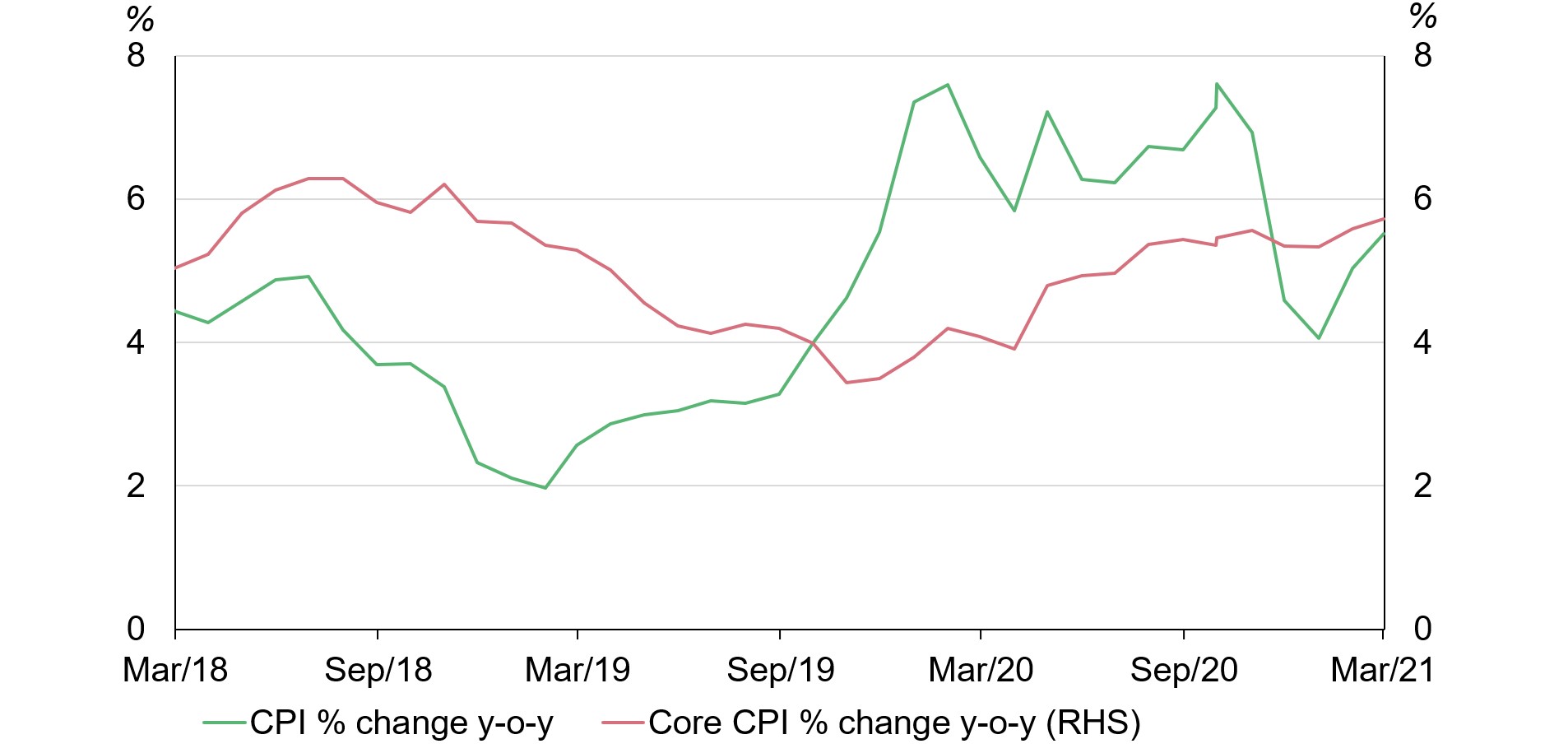

Retail inflation jumped to a four-month high

Retail inflation (CPI) rose to a four-month high of 5.52% in March from 5.03% in February due to higher food and fuel prices (Chart 3). As shown by a household expectations survey conducted by the RBI in March, household inflation expectations for the current period and for three months ahead have increased by 50 bps and 80 bps respectively. Econometric analysis we published in our report, ‘India’s gold market: Innovation and evolution‘, indicated that – everything else remaining constant – a 1% increase in inflation may increase consumer demand by 2.6% in the short term.4

Chart 3: India’s retail inflation climbed to four-month high in March

India’s CPI % change y-o-y vs core CPI % change y-o-y

Source: Bloomberg, World Gold Council

Retail demand was robust in the month

Anecdotal evidence suggests that retail demand in March was robust, supported by the following factors:

- The domestic gold price corrected, due to a combination of a lower international gold price and an appreciating rupee. As a result, the MCX Gold Spot price decreased by 5.2% m-o-m compared to a 4.5% decrease in the LBMA Gold Price AM

- Consumers took advantage of lower gold prices to purchase wedding jewellery

- The low base of 2020 has skewed the demand figure. This month’s relatively strong growth must be viewed against the loss of sales in March 2020 due to COVID-19 lockdowns and store closures in force at that time.

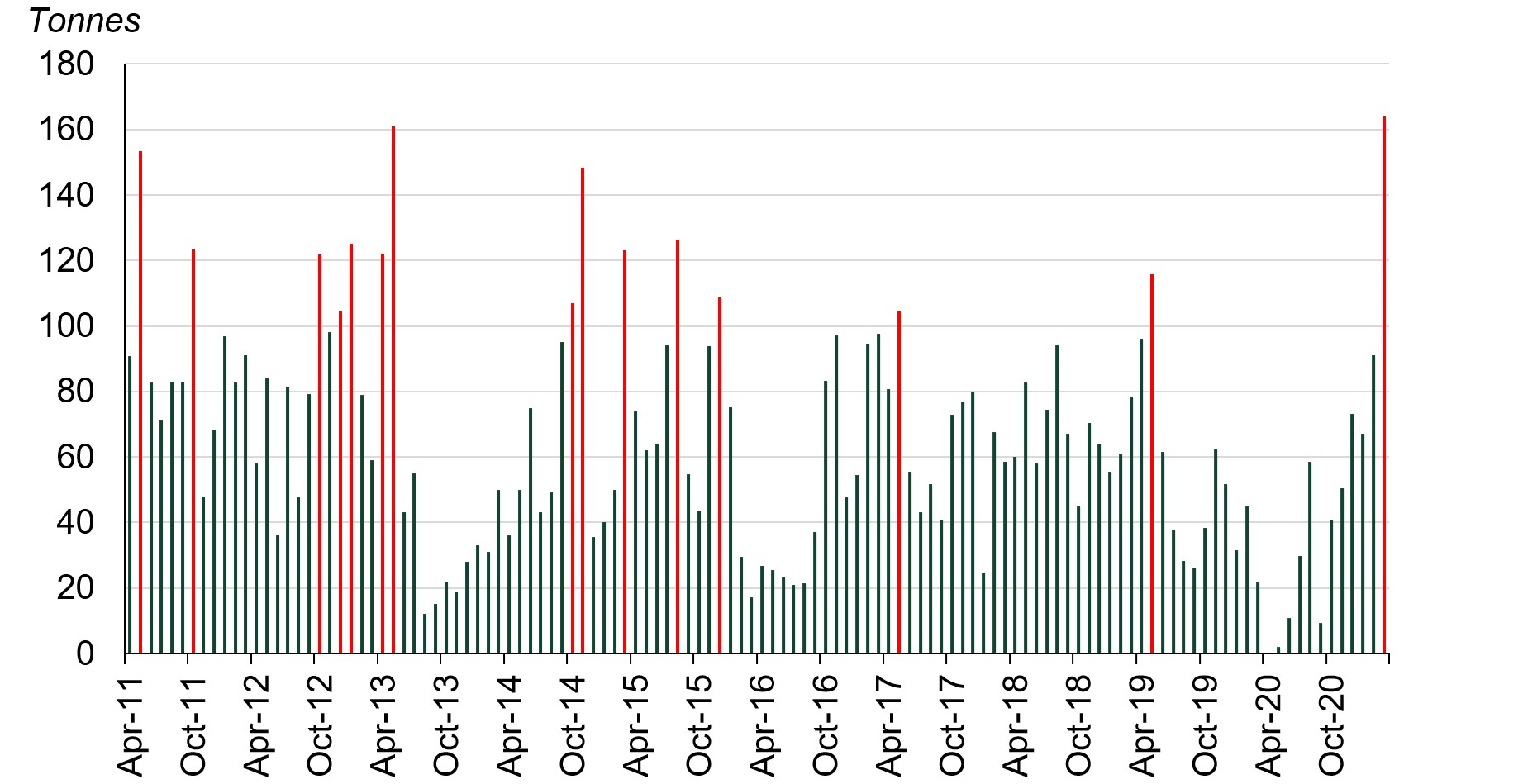

Indian official imports in March were highest in a decade

Indian official gold imports totalled 164t in March 2021, almost eight times higher y-o-y. Official imports in March were the highest in a decade; this is only the third time over the 10-year period that official imports have exceeded 150t on a monthly basis (Chart 4). We believe that robust retail demand – on the back of the lower gold price and wedding demand – along with re-stocking by jewellery manufacturers and retailers, are the factors responsible for driving official imports to such a high level. A total of 11 banks, nominated agencies and exporters imported 142.9t of bullion and 20 refineries imported an equivalent 21t of fine gold content in the form of gold doré. From a total 164t of official imports, 75.3t was imported via the Sri City Free Trade Warehousing Zone (FTWZ).5 Eight overseas banks accounted for these imports with JP Morgan, ANZ, Rand Merchant Bank and Standard Chartered accounting for 85%.

Chart 4: Indian gold imports in March were highest in a decade

Indian monthly gold imports from April 2011 – March 2021

Source: Infodrive India, Ministry of Commerce & Industry Govt. of India, World Gold Council

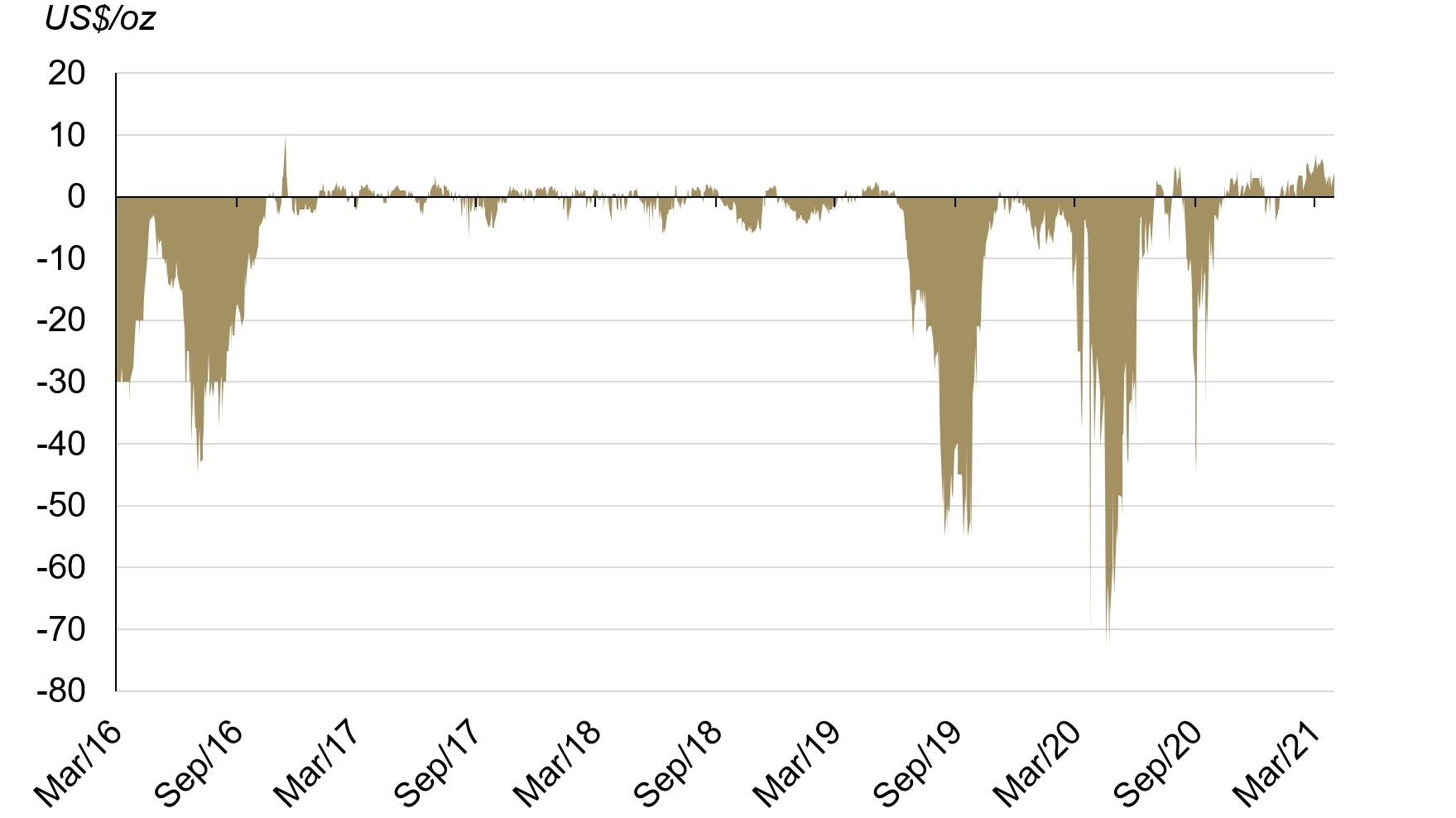

Local market premium jumped to a 51-month high

With a significant pick-up in retail demand the monthly average premium in March jumped to US$4.2/oz compared to an average of US$3.3/oz in February. The local premium rose to a 51-month high of ~US$6.5/oz in the first week of the month before moderating to US$3.5/oz by the end of the month (Chart 5).

Chart 5: Robust retail demand pushed local market premium to 51-month high in March

Difference between MCX Gold Spot price and landed gold price in India derived from LBMA Gold price AM

Gold ETFs continued to attract inflows in March

Anecdotal evidence suggests that the lower domestic gold price provided a welcome entry point for investors. Against the backdrop of a second wave of COVID-19, volatility for the MCX Gold Spot hit 17.8% in March, higher than the LBMA Gold PM (13.06%).6 A lower gold price, higher domestic gold price volatility and safe-haven demand lured investors towards gold ETFs. Inflows increased by 1.6t (Rs 6.62bn; US$96.1mn) taking total gold ETF holdings to 31.8t (Chart 6).

Chart 6: Indian gold ETF holdings reached 31.8t by the end of the month

The RBI added 7.5t to its gold reserves

After making 11.2t of purchases during February, the RBI added a further 7.5t of gold to its reserves in March taking its gold reserves to 695.3t, or 6.6% of total reserves (Chart 7).7 The RBI has stepped up gold purchases over recent years with the aim of diversifying its foreign reserves and maintaining the safety and liquidity of its forex reserves.

Chart 7: RBI added 7.5t of gold to its reserves in March

Footnotes

1Domestic gold price refers to MCX Gold Spot price.

2We compare the LBMA Gold Price AM with MCX Gold Spot price as their trading hours are closer to each other than the most commonly referenced LBMA Gold Price PM.

3Under Operation Twist, the RBI simultaneously sells short-term government bonds and purchases long-term government bonds to reduce the yield of long-term government bonds. Because of simultaneous buying and selling of two different type of securities, there occurs a “twist” in the shape of the yield curve.

4We used a common approach to estimating long- and short-term effects called Error Correction Model (ECM), which we applied to determine the drivers of gold consumer demand using data from 1990 to 2015. See India’s gold market: evolution and innovation, January 2017, Appendix 2, p. 81.

5FTWZ offers a distinct advantage as overseas suppliers can import gold into the custom-bonded warehouse of FTWZ without paying customs duty for authorised operations. Imported gold can be stored in FTWZ for a long period – as long as the letter of approval (LOA) is valid – thus reducing the logistics time in supplying to the domestic market as compared to importing from the overseas market.

6Gold Price Volatility from Goldhub; one-month volatility as of March 2021. We are using end-of-day gold price, i.e., MCX Gold Spot and LBMA Gold PM for our volatility calculations.

7Central Bank data is taken from IMF-IFS; IFS up until February and weekly statistics from the RBI for March. Please refer to our latest Central Bank Statistics https://www.gold.org/goldhub/data/monthly-central-bank-statistics.

This article is republished with permission from the World Gold Council