Jewellery buying is changing fast. Today’s consumers value meaning, identity, and ethics over tradition and status. Diamond industry analyst Avi Krawitz reveals key insights from McKinsey and The Plumb Club’s latest reports, revealing how shifting habits and expectations are reshaping the jewellery landscape — and what brands must do to stay relevant.

As the diamond and jewellery industry navigates supply imbalances, the rise of lab-grown diamonds, and geopolitical shifts, a quieter yet powerful force is reshaping the market: the consumer.

In the post-pandemic era, evolving digital habits, shifting perceptions of value, and a growing preference for local businesses are redefining how and why people buy. Two recent studies — McKinsey & Company’s State of the Consumer 2025 and The Plumb Club’s Industry and Market Insights 2025 — offer valuable insights into this changing mindset.

Both reports underscore a fundamental shift in consumer expectations and suggest that brands unable to adapt risk falling behind.

From Scroll to Store

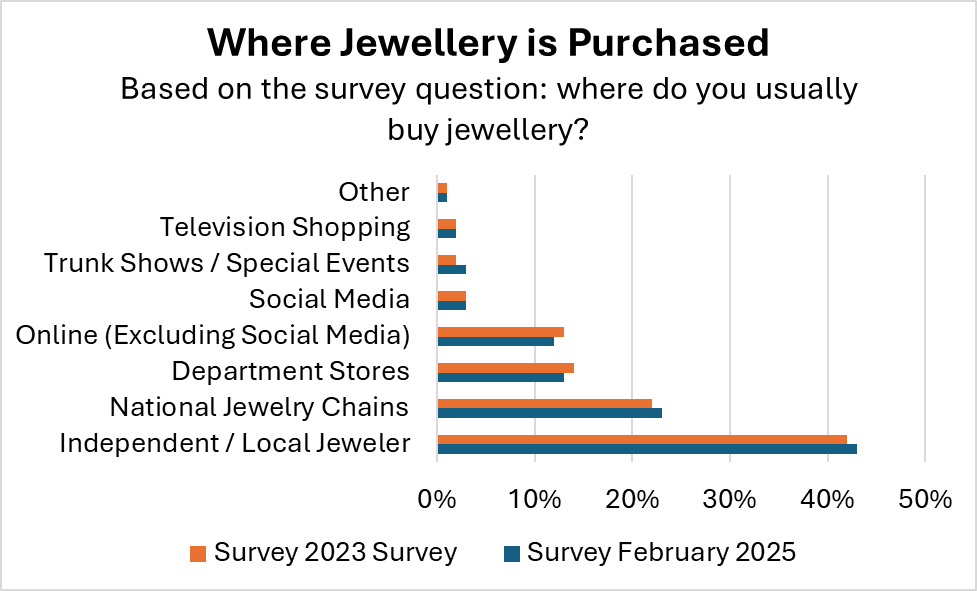

McKinsey’s findings confirm what the trade has long suspected; online behaviour has become the starting point for most consumer journeys. Yet, the final purchase often still happens in-store. According to The Plumb Club, 43% of US consumers prefer buying from local and independent jewellers, while just 12% complete their purchases online.

This split highlights a deeper trend: consumers want the convenience of digital discovery, but they’re also drawn to the hands-on and immersive experience of a physical store.

“Consumers are spending more time online, but they’re not necessarily buying there,” said Lawrence Hess, Executive Director of The Plumb Club, during a recent webinar. “The digital experience must lead naturally to a physical one — both must feel seamless.”

The Paradox of Influence

Although people spend more time than ever on social media, it doesn’t carry the same trust as traditional word-of-mouth. McKinsey points to a widening credibility gap in which consumers may engage with content, but they’re increasingly sceptical of its intent.

Consumers distrust social media when making their purchasing decisions, the McKinsey analysts wrote. However, because it’s where they interact with friends and family, social media continues to shape brand perception unconsciously.

The Plumb Club’s survey found that 31% of consumers cite designers and brands as the primary influences on their purchasing decisions, closely followed by friends and family at 30%, and retailers’ websites at 21%. Far less persuasive were social media ads, magazines (digital or print), influencers, and celebrities.

“It’s not about shouting louder on Instagram,” Hess said. “It’s about showing up with authenticity. Especially with Gen Z — if they sense anything disingenuous, they walk away.”

Gen Z Emerges

One of the most compelling insights from both reports is the growing influence of Gen Z — consumers born between 1996 and 2010. Expected to account for nearly 30% of global luxury consumption by 2030, this generation isn’t simply entering the market — they’re reshaping it.

For brands, understanding what drives Gen Z is critical for long-term growth, stressed the McKinsey report. “They’re the first generation to grow up fully immersed in digital life and came of age during the Covid-19 pandemic,” it noted.

These experiences have altered how Gen Z views traditional life milestones. Unlike previous generations, they are less likely to define success through marriage or parenthood, instead prioritising financial independence, career achievement, and wealth creation.

Though poised to become the largest and wealthiest generation in history, they face mounting challenges including rising costs of living and student debt. Their outlook diverges from older cohorts: they’re more optimistic about social progress but more wary of economic headwinds like inflation, McKinsey highlighted.

That mindset is deeply reflected in their buying behaviour. According to The Plumb Club, Gen Z is fuelling demand for non-traditional materials, men’s jewellery, and more fluid expressions of identity and style. Their pragmatic approach to value is also driving the rise of lab-grown diamonds, especially in fashion segments.

“Luxury, to Gen Z, is about emotional resonance and ethical clarity,” said Paola De Luca, Trend Forecaster and Contributor to The Plumb Club’s research. “They’re not buying status, they’re buying meaning.”

The Local Advantage

A lasting effect of the pandemic has been consumers’ renewed focus on proximity and personalisation. McKinsey notes a rising preference for locally made products — a shift driven by global supply chain disruptions and a growing desire for community-based engagement.

The Plumb Club reinforces this trend, reporting that independent jewellers are outperforming national chains and department stores in consumer preference. Notably, stores that foster a sense of belonging — through education, events, and cultural connection — are proving more successful than those offering purely transactional experiences.

“The best retailers are no longer just selling,” said De Luca. “They’re building community.”

Value, Redefined

While price sensitivity remains high in 2025, the perception of “value” is evolving. Today’s consumers — especially younger ones — are making more intentional trade-offs, cutting back in some areas to spend more on others that carry emotional or qualitative weight.

According to The Plumb Club, spending on non-bridal jewellery rose 28% since its last survey in 2023 to $1,664, while bridal jewellery saw a modest 2% increase, reaching $5,493 on average. Quality has overtaken size as the top purchase driver, with a 25% increase in importance, it found.

This supports McKinsey’s view that “smart indulgence,” where meaning and longevity take precedence over status or scale, has become the new standard for luxury.

Trade Implications

Today’s consumer isn’t walking away from jewellery, they’re reframing its meaning and purpose. To stay relevant, brands need more than strong inventory and polished marketing, they need a clear, forward-thinking strategy.

Key imperatives:

- Connect digital and physical: The online journey should guide customers toward a meaningful in-store experience, not replace it.

- Build genuine trust: Messaging must reflect real values. Consumers can spot insincerity quickly.

- Prioritise ethics and transparency: Traceability is no longer a nice-to-have. It’s expected.

- Act local and think personal: No matter the scale, retailers must offer the familiarity and care of a neighbourhood jeweller.

In 2025, jewellery is more than an accessory. It’s a reflection of identity, emotion, and intent. As buyers become more discerning, companies face a clear choice: evolve with their customers or risk being left behind.

The research is clear. The jewellery buyer is changing, presenting an opportunity to brands and companies willing and able to adapt in this dynamic and volatile environment.

Avi Krawitz is the Founder of ‘The Diamond Press’ and a leading content creator and consultant in the diamond industry. He is widely recognised for his insightful analysis and storytelling, offering clarity to both industry professionals and curious consumers navigating a complex and evolving market. See more of Avi’s work at www.thediamondpress.com