China’s diamond market, once a seemingly unstoppable force in the luxury sector, is undergoing a dramatic recalibration. Senior China-based analyst and researcher, Liang Weizhang, maps the key demand trends, dissects the underlying drivers, and considers the strategic adjustments required for the industry to adapt to China’s new market realities.

Over the past few years, China’s diamond market has undergone a notable transformation, reflecting broader shifts in consumer behaviour and economic dynamics.

According to data from the Gems & Jewelry Trade Association of China, the diamond market size contracted sharply from RMB 100 billion in 2021 to RMB 43 billion in 2024, representing a 57% decline. Diamonds’ share of the overall jewellery market also fell from 14% to 6% during the same period.

These figures mark a significant adjustment for an industry that was previously regarded as a fast-growing pillar of China’s luxury sector. Rather than indicating a simple downturn, however, the evolving landscape may suggest a broader realignment of consumer values, market structures, and strategic priorities.

A Market in Transition: From Expansion to Contraction

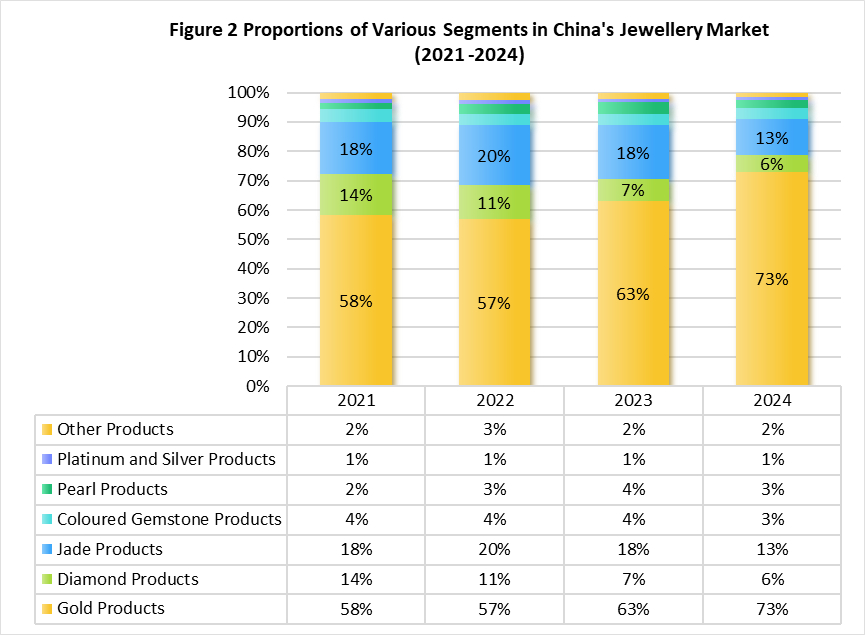

Once emblematic of luxury and romance, the diamond sector now faces substantial structural changes. During the same period that diamond demand declined, gold jewellery reinforced its dominance, growing from 58% to 73% of the market share. Meanwhile, other categories such as jade and pearls demonstrated considerable volatility. The jade market expanded initially but contracted sharply by 2024, while pearls experienced a surge followed by a retreat. Furthermore, the overall Chinese jewellery market demonstrated notable resilience, with its total size expanding from RMB 720.5 billion in 2021 to RMB 820 billion in 2023, before experiencing a slight contraction to RMB 778.8 billion in 2024. These shifts in segment share underline a broader rebalancing across jewellery categories rather than an outright decline in consumer interest.

Import Statistics Reflect Market Adjustments

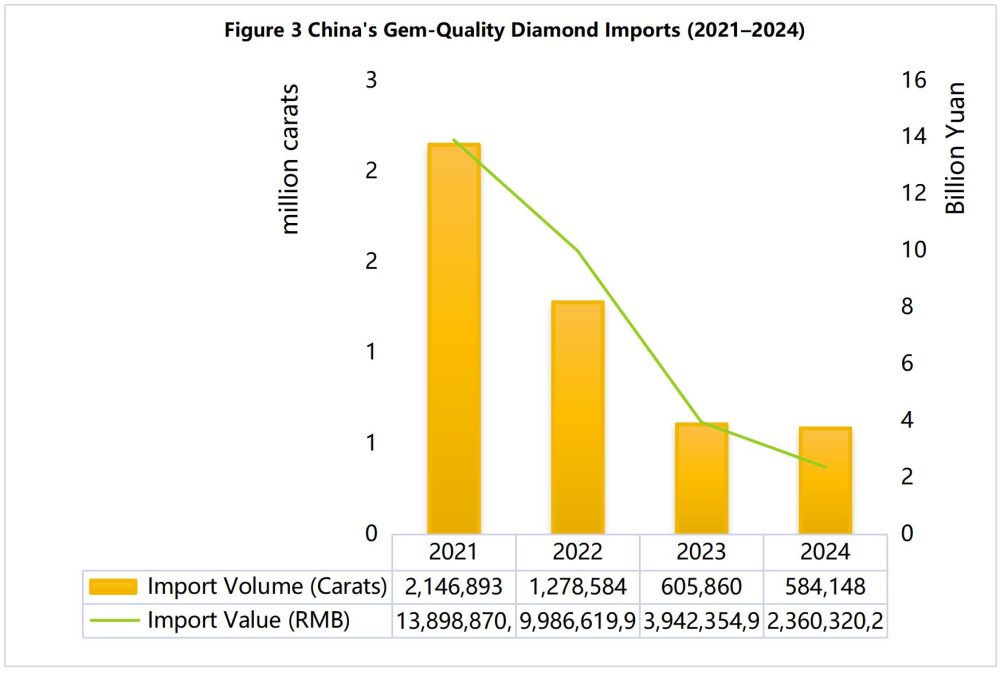

Import data reinforces the narrative of adjustment. Data from the General Administration of Customs of China show that the volume of gem-quality diamonds (HS code 710231, 710239) imported under general trade terms declined by 73% between 2021 and 2024, with the value of imports decreasing even more sharply by 83%. While the volume only fell by 4% year-on-year in 2024, the corresponding 40% drop in value suggests mounting downward pressure on diamond prices.

This pricing trend may indicate both changes in consumer demand structures and shifts in supply dynamics. The data further signals that China’s diamond market is not merely shrinking but evolving — potentially towards more affordable, differentiated product segments.

The New Consumers: Values over Status

One of the most discussed drivers of change is the shifting mindset among younger consumers. Millennials and Generation Z are seen to prioritise individuality, ethical considerations, and value-consciousness. For many, diamonds no longer serve as the ultimate symbol of status, but rather as one among many expressions of personal identity.

The rising acceptance of laboratory-grown diamonds — with their sustainability narratives and more accessible pricing — is another factor shaping this evolution. While natural diamonds retain their intrinsic allure, the competitive landscape is undeniably becoming more complex.

Economic Undercurrents and Investment Thinking

Macroeconomic influences cannot be ignored. In a climate of moderated GDP growth and cautious spending, Chinese consumers are increasingly drawn to purchases with intrinsic financial value. Gold jewellery’s ascendancy reflects this sentiment: offering both adornment and investment security, gold has become an attractive proposition in uncertain times.

In contrast, the more subjective value proposition of diamonds demands renewed marketing sophistication. Brands must work harder to reconnect with consumers on an emotional and symbolic level, transcending the transactional narrative.

Rethinking Strategies: Beyond One-Size-Fits-All

It would be premature to view the current contraction as terminal. Rather, the shifts may represent a critical turning point. Successful players are likely to be those who differentiate their offerings, strengthen their storytelling, and engage across digital ecosystems.

Moreover, China’s regional diversity presents opportunities. Emerging cities beyond Beijing and Shanghai are nurturing new luxury consumers with distinct tastes and expectations. A tailored, localised approach may be essential to re-energising demand.

A Market Redefining Itself

In sum, while China’s diamond sector faces undeniable headwinds, it remains a market of significant potential. The story unfolding is not one of decline, but of redefinition. Future success will depend on how well the industry interprets the evolving aspirations of Chinese consumers — and how adeptly it navigates the interplay of tradition, innovation, and value.

Liang Weizhang, CEO of HubWis Jewellery Strategic Creations (Guangzhou) Co., Ltd., is a senior analyst and strategic researcher in the jewellery industry. He is the founding President of the Guangzhou Diamond Exchange and Vice Chairman of the Guangdong Gold Association. With nearly 30 years of experience in the diamond, gold, and jewellery sectors in China and internationally, Liang offers deep industry insight and a strong professional network. His company supports jewellery businesses with strategic consulting, industry advice, and access to global markets.