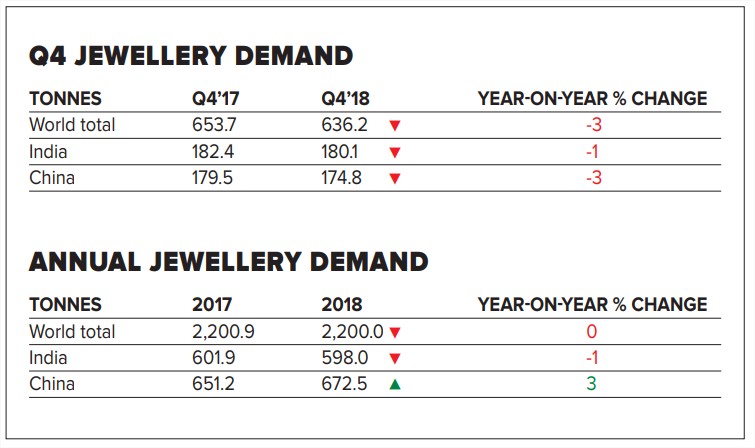

India’s annual gold jewellery demand was stable at 598 tonnes, a drop of only 1% or 4 tonnes from the previous year, according to the World Gold Council’s (WGC’s) latest Gold Demand Trends report. India’s fourth quarter gold jewellery demand was also fractionally lower year-on-year, down 1% at 180.1 tonnes (versus 182.4 tonnes), as consumers showed caution in the face of high and volatile local gold prices.

“Demand was constrained in 2018 as there were relatively few auspicious wedding days in the Hindu calendar. This had a particularly pronounced effect on Q4 demand, given that November and December are traditionally peak wedding season months. The outlook is more positive for 2019, as there is a marked increase in the number of such auspicious days,” the report stated.

The WGC said that buoyant inventory levels meant a good portion of retail demand in Q4 was met by de-stocking. Strong imports in Q3 led to a build-up of stock among manufacturers and wholesalers, which was drawn down during Q4 to meet demand – reflected in a 23% year-on-year drop in fourth quarter official gold imports.

“There was also a rise in the volume of gold-for-gold exchange. At a time of higher and more volatile local gold prices, the market saw a rise in the number of consumers preferring to exchange existing gold for new pieces. This was particularly prevalent in the South and West regions, where some retailers reported an increase of up to 45% in exchange activity. The market was therefore well supplied with gold, and this was reflected in local price discounts,” the WGC added.

The local gold price was at a discount to the international prices of around $2/oz on average during Q4. The domestic gold price was broadly at a discount during the quarter (aside from a small window in late November when a dip in prices sparked a bout of buying, pushing it to a small premium). The market was well supplied by stocks and gold-for-gold exchange at a time of constrained demand, the report noted.

Organised jewellery retailers continued to gain market share, the WGC said. Partially as a consequence of government policy in recent years, national and regional chain stores continued to outperform single, standalone stores. Chain stores reported positive Q4 sales growth, in contrast to single stores that reported Q4 sales as being flat or marginally lower, it revealed.

Global jewellery demand

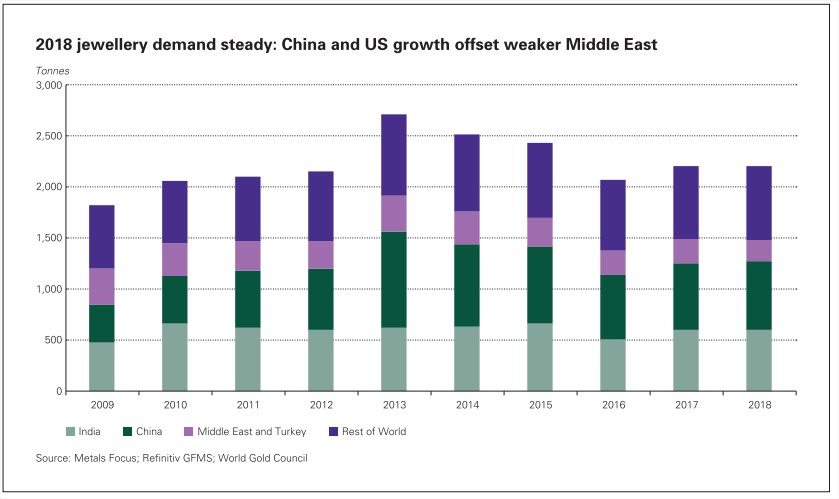

Worldwide annual gold jewellery demand was steady at 2,200 tonnes, down just 1 tonne from the previous year. Gains in China (3%), the US (4%) and Russia (9%) broadly offset sharp losses in the Middle East, where demand dropped 15% on 2017.

China was the main engine of growth in 2018, despite witnessing a slowdown in Q4 as the trade war with the US and slowing economic growth rate weighed on demand. Economic hardship, relatively weak currencies and the after-effects of tax-changes affected Turkey and Middle Eastern markets to varying degrees: Iran and Turkey were hit particularly hard.

“Annual Chinese jewellery demand grew by 3%, but recovery stalled in Q4. Full-year Chinese jewellery demand reached a threeyear high of 672.5 tonnes. But Q4 demand slipped 3% to 174.8 tonnes as the local gold price spiked sharply higher in October and economic growth continued to slow down. Furthermore, the ‘Golden week’ holiday in October did not provide the usual boost to jewellery demand that it has done in the past. The role of this holiday as a shopping occasion is gradually fading as consumers increasingly use it instead as an opportunity to spend on experiences, such as travel. We expect this trend to continue in 2019,” the WGC said.

Jewellery demand was very weak in both Q4 and 2018 for the UAE and Saudi Arabia alike. Both markets were affected by the introduction of 5% VAT in Q1 2018. Purchasing activity ahead of the tax change boosted Q4 2017 demand, making Q4 2018 demand all the weaker in comparison.

Another year of modest growth in the US took jewellery demand to a nine-year high of 128.4 tonnes (up 4% year-on-year). The fourth quarter saw an eighth consecutive quarter of year-onyear growth and demand of 48.1 tonnes was the highest since Q4 2009. Gains were widespread across the spectrum, from lowercarat, mass-market jewellery to high-end branded items. But the pace of growth decelerated slightly in Q4 as concern over the path of US economic growth combined with a sharp correction in US equity markets dampened consumer confidence. And prospects for Q1 2019 are less buoyant as the ongoing government shutdown impacts sentiment and the wealth effect of the stock market correction filters through to consumers.

European jewellery demand was fractionally lower on an annual basis, down 1% to 73.4 tonnes. Fourth quarter demand slipped 2% to 33.5 tonnes – the lowest Q4 in the WGC’s data series – as consumers became more cautious.