Sluggish demand in China, the world’s second largest diamond market, has plummeted by as much as 50% this year. The reasons behind this downturn are multifaceted, stemming from macroeconomic challenges, shifting consumer preferences, and geopolitical factors. Paul Zimnisky offers a comprehensive analysis of these dynamics.

Up until this year, Greater China, including the Mainland, Hong Kong, Macau, and Taiwan, was considered the diamond industry’s second largest – and fastest growing – market, estimated to represent upwards of 20% of global diamond jewellery demand. However, with demand down as much as 50% this year, India is estimated to have overtaken China as the industry’s second largest consumer market with just a low double-digit percentage share.

According to anecdotes from mid-stream participants, diamond demand in China could be down even more than 50%, with some indicating that polished sales to Chinese clients are only 20% to 40% of “normal” levels.

Given the neck-breaking volatility over the last few years, in addition to the private nature of the trade, it’s difficult to precisely pin down how much diamond sales are off in China. This challenge is further compounded by the re-emergence of Chinese luxury consumers once again shopping abroad (in the post-pandemic period).

For example, the exchange rate in Japan is highly favourable right now which is attracting luxury consuming tourists from around the globe, but especially those from Mainland China. On the other hand, the Hong Kong dollar is relatively expensive at the moment which is having the opposite effect.

During a recent analyst call, LVMH’s CFO Jean-Jacques Guiony bluntly explained, “the magnitude and velocity of the yen weakness make it difficult to offset the impact through price increases,” adding, “we are reluctant to unduly penalise local demand in Japan (with large price increases).”

For context, the yen is the weakest it has been versus the euro since 2008. Japan has been exercising dovish monetary policy for years in an effort to stimulate the economy in the face of a challenging demographic shift, i.e. population decline. The effect has been a consistently weaker yen which has been exacerbated by global investors shorting it.

Speaking to the situation within Greater China, Guiony noted that prices are currently “extremely” high in Hong Kong and Macau as both the Hong Kong dollar and Macanese pataca are pegged to the US dollar, and the US dollar has been strong against the Renminbi (the currency used in the Mainland).

Corporate Chinese jeweller Chow Sang Sang reported that its gem-set jewellery sales fell 42% in the first half of the year which it attributed to the “global downtrend” in diamonds. It’s worth noting that along with a lot of other Asian jewellers, Chow Sang Sang’s merchandise mix is heavily weighted towards gold with gem-set jewellery only representing 7% of total company sales with diamonds only representing a portion of that.

Gold jewellery demand in China has also been softer as of late, albeit to a much lesser extent than diamonds, as the yellow metal has progressively made new all-time highs in 2024 breaching the psychologically important $2,500-an-ounce for the first time.

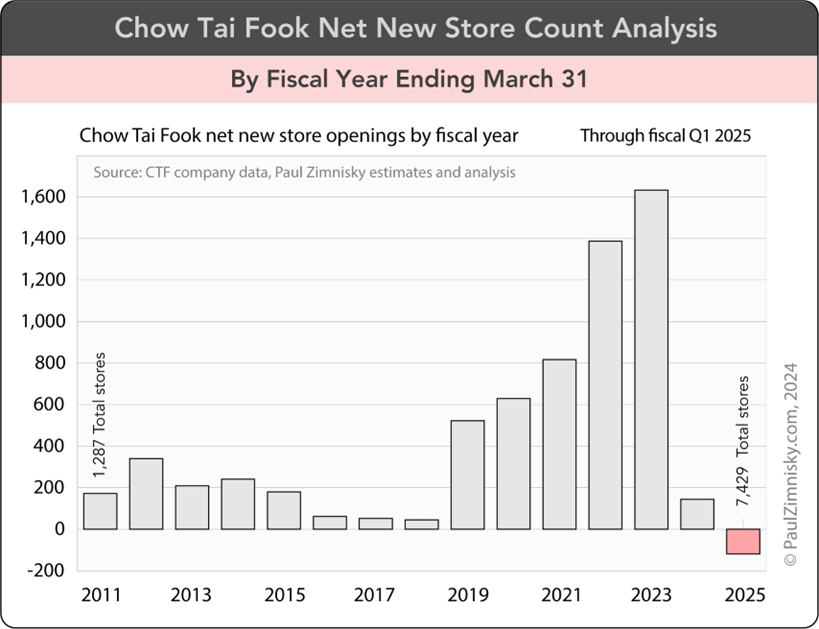

Chow Sang Sang’s large competitor, Chow Tai Fook, which has been opening new stores at a feverish pace over the last decade is on pace to net close stores this year. This serves as a proxy of sorts for the salient shift in overall jewellery demand in China (see figure above).

Encouragingly, in May, Chow Tai Fook struck a cooperative arrangement with De Beers targeting the promotion of natural diamonds, which will include directly educating front-line sales associates with selling tactics. Similar partnerships have been forged this year between De Beers and Signet Jewelers and Tanishq – the largest diamond sellers in the US and India, respectively.

Looking ahead, a resilient recovery in diamond demand in China will likely rest on a macroeconomic recovery that boosts Chinese consumer’s discretionary spending ability and sentiment. And this could still take some time.

In August, Chow Sang Sang management said it “has become clear that we need to be prepared for a prolonged struggle against strong and biting economic headwinds battering our markets,” adding that it has consequently “cut back” inventory.

When asked about a Chinese recovery in late-July, LVMH’s Guiony said “it’s difficult to anticipate what will happen in the second half of the year … we have no reason to be pessimistic, but being optimistic would be probably quite bold at this point in time.”

To provide broader longer-term perspective, an average of forecasts from the IMF, OECD and World Bank point to the Chinese economy growing at under 5% this year and closer to 4% next year. For context, China has grown at a high single-digit percentage annual rate over the trailing 25 years.

While GDP doesn’t necessarily allow for a comprehensive measure of economic growth in China, the nation’s economy is undoubtedly going through a structural slowdown. This shift is being felt across global industries given that China has singlehandedly represented upwards of 40% of the world’s economic growth over the last quarter century.

Paul Zimnisky, CFA is an independent diamond industry analyst and consultant based in the New York metro area. For regular in-depth analysis and forecasts of the diamond industry please consider subscribing to his State of the Diamond Market, a leading monthly industry report; an index of previous editions can be found here. Also, listen to the Paul Zimnisky Diamond Analytics Podcast on Spotify or Apple Podcasts for exclusive full-length conversations with special guests from the gem and jewelry industry. Paul is a graduate of the University of Maryland’s Robert H. Smith School of Business with a B.S. in finance, and he is a CFA charterholder. He can be followed on X @paulzimnisky and on YouTube @paulzimnisky.

Paul will be speaking at the Bharat Diamond Bourse on October 11 in Mumbai and also at INHORGENTA on February 22, 2025, in Munich. He will also be in Surat in early-October, in Angola in late-October and in Milan in February 2025. He can be contacted at paul@paulzimnisky.com to arrange a meeting.

Disclosure: At the time of writing Paul Zimnisky held a long equity position in Brilliant Earth Group and Newmont Corp. Paul is an independent board member of Lipari Diamond Mines, a privately held Canadian company with an active mine in Brazil and a development-stage asset in Angola. Please read full disclosure at www.paulzimnisky.com.