The global diamond market is poised for a potential inventory correction in the second half of the year, driven by upstream supply cuts and a seasonal surge in demand. Analyst Paul Zimnisky’s analysis reveals that significant inventory levels, which have soared to around $50 billion, might finally begin to recede.

Going into the back-half of 2024, the global natural diamond supply chain could begin to see excess inventories begin to abate as upstream measures to curtail new supply coincide with an uptick in seasonal downstream demand factors.

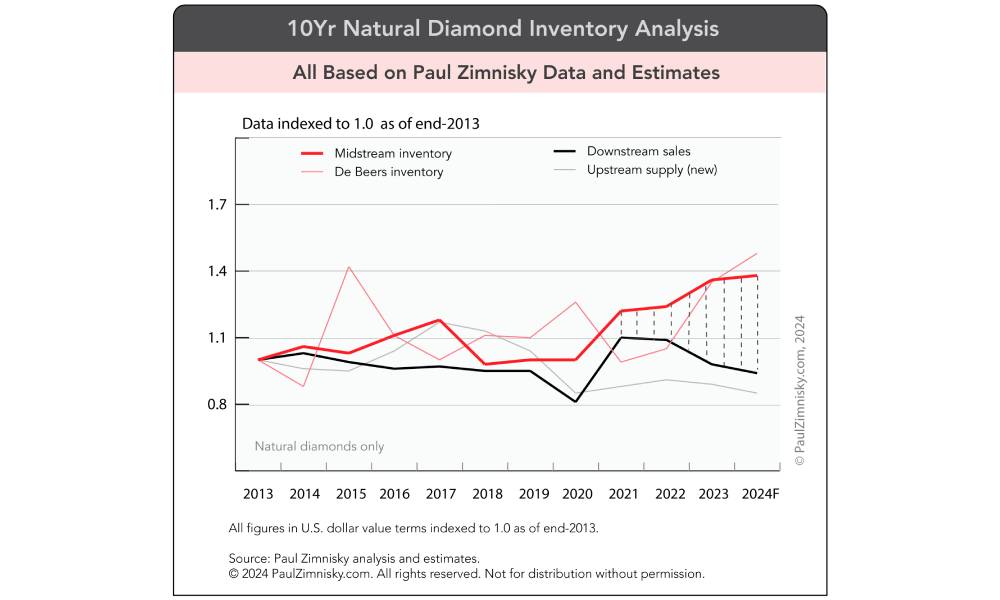

According to Paul Zimnisky analysis, inventory held by the global diamond midstream, including that held by rough and polished wholesalers, traders and manufacturers, has grown to some $50 billion, up from about $43 billion a year ago and well under $40 billion as of mid-2022 (see figure below for relative analysis).

In addition, rough inventory held by De Beers has grown 10% year-over-year in volume terms and is up as much as 40% over the last two years, according to Paul Zimnisky estimates. In response, in April, the company cut 2024 production guidance to 26-29 million carats from 29-32 million (which was previously cut from 30-33 million in 2022).

Year-to-date, De Beers’ rough sales in value are down 17% versus a year ago and down 38% compared to two years ago.

Russia’s primary diamond miner ALROSA, which has not publicised production and sales figures since early-2022, said that the government’s precious metal and stone reserve, the Gokhran, bought the company’s “entire cut of production” in March – in effect talking the supply off the market. In April, Russia’s Ministry of Finance implied the Gokhran would make further diamond purchases this year as “one of the tools of support during the (Western) sanctions.”

In June, North America’s major diamond retailing conglomerate, Signet Jewelers, acknowledged that independent jewellers in the U.S. have been “significantly over inventoried for the last 18 months” coming off an aggressive restocking run in late-2022 and 2023. The U.S. is the world’s largest consumer of diamonds, representing over half of global demand –independents make up approximately three-quarters of U.S. diamond sales.

According to Signet, the condition has led to “heightened discount activity among many jewellery participants” in the U.S. which are jockeying for sales amidst a “cautious” consumer. That said, Signet itself reduced its inventory position by 9% year-over-year as of early-May despite expectations for a 5-10% recovery in engagements this year, a trend that it expects to continue for at least the next two years – i.e. the implication being that a growth in engagements will drive diamond engagement rings sales.

According to anecdotes collected by Paul Zimnisky, independent jewellers in the U.S. will still buy diamond stock in preparation of the upcoming holiday season, albeit most purchases will be lighter and more selective than in the recent past. Whereas more commercial jewellery chains in the U.S., that are currently sitting on more moderate stock, will be in a position to more aggressively buy in accordance with the strength of holiday 2024.

Looking more globally, a major sensitively for diamond demand (and thus inventory rebalancing) continues to be a recovery in China. The industry’s second largest consumer market has been lacklustre for at least the last 18 months given the macroeconomic impact on consumer sentiment – and more worryingly, Chinese consumers ebbing confidence that diamonds are a store of value.

However, in June, Chow Tai Fook management encouragingly noted “we have observed a stabilising sales trend across various gem-set collections…underpinning our confidence on the long-term prospects of diamond jewellery.” In the fiscal year ended March, diamond jewellery represented 9% of the company’s total sales (equating to $1.3 billion), which was down from 11% the prior year.

Chow Tai Fook is Greater China’s largest corporate jeweller.

Paul Zimnisky, CFA is an independent diamond industry analyst and consultant based in the New York metro area. For regular in-depth analysis and forecasts of the diamond industry please consider subscribing to his State of the Diamond Market, a leading monthly industry report; an index of previous editions can be found here. Also, listen to the Paul Zimnisky Diamond Analytics Podcast on Spotify or Apple Podcasts for exclusive full-length conversations with special guests from the gem and jewellery industry. Paul is a graduate of the University of Maryland’s Robert H. Smith School of Business with a B.S. in finance and he is a CFA charterholder. He can be reached at paul@paulzimnisky.com and followed on X @paulzimnisky.

Disclosure: At the time of writing Paul Zimnisky held a long equity position in Brilliant Earth Group and Newmont Corp. Paul is an independent board member of Lipari Diamond Mines, a privately-held Canadian company with an active mine in Brazil and a development-stage asset in Angola. Please read full disclosure at www.paulzimnisky.com.