Throughout 2024, the scope of Western sanctions targeting Russian diamonds is expected to expand, potentially impacting diamonds as small as 0.5 carat starting from September 2024. However, diamond industry expert Paul Zimnisky projects that nearly 40% of Russia’s diamond output may evade the G7 sanctions by that time, owing to either their smaller size or industrial quality.

As 2024 quickly progresses, the natural diamond trade is approaching the next planned phase of Western sanctions on Russian diamonds. As of September, the cutoff size of embargoed Russian goods is expected to be narrowed to 0.5-carat from the 1.0-carat threshold implemented in March.

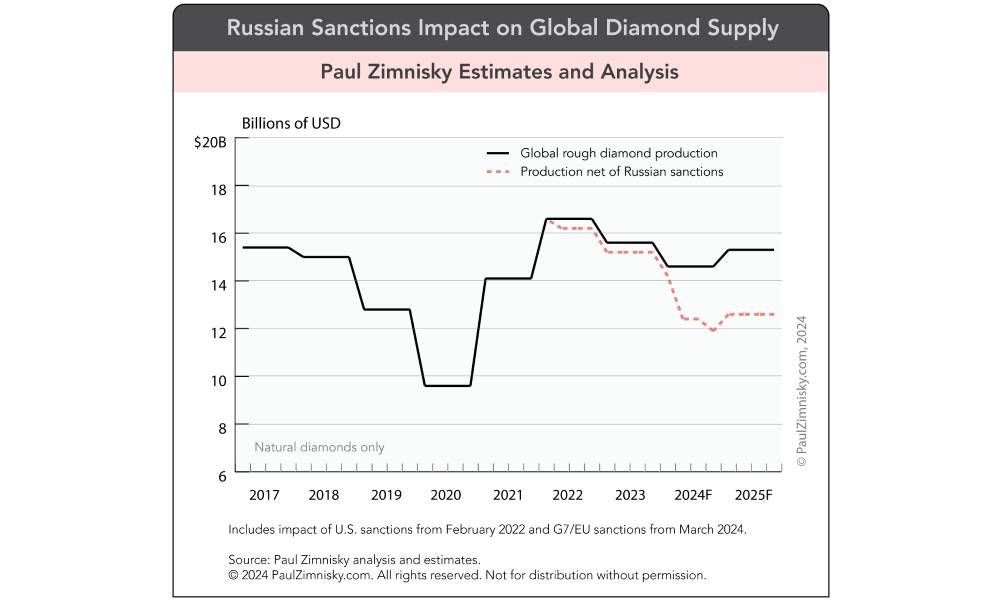

So far, the larger G7/EU restrictions – which built on initial U.S.-specific sanctions implemented in 2022 – have yet to have a noticeable impact on the global supply of natural diamonds. The reasons, which are multivariate, include an oversupplied supply chain going into 2024, the long runup to the more stringent sanctions which gave the trade time to prepare, and the fact that the current framework only includes medium and larger sized goods – when Russia is known to disproportionately produce smaller goods.

For context, while Russia is the largest producer of natural diamonds by volume, representing upwards of a quarter of global supply by value, it is estimated that about 45% of Russian diamonds by value will polish into goods that meet or exceed the 1-carat sanction threshold that went into effect in March. Using the proposed September cut-off, i.e. 0.5-carat polished, the figure will increase to about 60%. In effect, this means that by September, as much as 40% of Russia’s diamond production will not fall under the sanctions, i.e. because the goods are too small (or are industrial-quality).

Taking the above account, of the approximately $15.5 billion of global rough diamond supply forecast to be produced in 2025, about $12.5 billion will be available to Western nations net of sanctions (see above figure).

As far as the impact on Russia, ALROSA, the nation’s primary diamond producer, implied that it would not be cutting production this year despite sanctions. In early-May, the company’s CEO Pavel Marinychev told Interfax (translated): “sanctions are not a reason not to work.”

That said, in April, Interfax reported that the nation’s precious metal and stone reserve, the Gokhran, bought all of ALROSA’s March production in what Deputy Finance Minister Alexei Moiseyevas described as “one of the tools of support during the sanctions.” Notably, the last time that the Gokhran bought a considerable amount of diamonds was during the Global Financial Crisis some 15 years ago.

It is estimated that ALROSA production has been 33-35 million carats (per annum) the last two years, which compares to 30 million carats during the pandemic lull in 2020 and 37-40 million in the years leading up to the pandemic.

Given the shear volume of diamonds produced by Russia, it seems inevitable that the sanctions will eventually lead to supply shortages of certain categories – or at least bottlenecks – especially once the supply chain’s current excess stock is worked through.

The question then becomes how will the diamond industry respond to reduced supply? The possibilities include increasing capacity of non-Russian natural diamond production, filling shortages with lab-grown diamonds (LGDs), or allowing relative prices for natural diamonds to adjust to the new levels of supply.

Paul Zimnisky, CFA is an independent diamond industry analyst and consultant based in the New York metro area. For regular in-depth analysis and forecasts of the diamond industry please consider subscribing to his State of the Diamond Market, a leading monthly industry report; an index of previous editions can be found here. Also, listen to the Paul Zimnisky Diamond Analytics Podcast on Spotify or Apple Podcasts for exclusive full-length conversations with special guests from the gem and jewelry industry. Paul is a graduate of the University of Maryland’s Robert H. Smith School of Business with a B.S. in finance and he is a CFA charterholder. He can be reached at paul@paulzimnisky.com and followed on X @paulzimnisky.

Disclosure: At the time of writing Paul Zimnisky held a long equity position in Brilliant Earth Group and Newmont Corp. Paul is an independent board member of Lipari Diamond Mines, a privately-held Canadian company with an active mine in Brazil and a development-stage asset in Angola. Please read full disclosure at www.paulzimnisky.com.