Despite fears of disruption, early signs show that American jewellery buyers are holding steady in the face of new U.S. tariffs on diamond imports. Independent diamond industry analyst Paul Zimnisky observes that while industry insiders continue to navigate shifting cost structures and geopolitical uncertainty, consumers at the retail counter appear largely unfazed — at least for now.

It’s been about 45 days since the U.S. launched its hard-hitting tariff campaign on the world. While the news stymied what was a fragile early-stage recovery in the B2B diamond market, consumer demand has not (at least yet) been hit as hard as many feared.

As it stands, the U.S.’s initial tariff schedule on 60 nations, which ranged from 26% on India to 37% on Botswana, has been temporarily reduced to a 10% base-rate on pretty much all nations excluding China (which still sits at around 50%). For the diamond industry, the U.S. tariff on India remains key given that the U.S. is the largest buyer of diamonds globally and India the largest manufacturer (for the purpose of tariffs, the diamond origin is considered where it was cut and polished).

With a 10% tariff in place, many Indian suppliers are splitting the cost of the duty with their U.S. clients according to anecdotes gathered by Paul Zimnisky. For instance, if a round 1-carat VS-clarity, near-colourless wholesales for around $2,800, each party effectively consumes $140 worth of the tariff. If the retailer decides to pass on this cost to the consumer, the effective impact downstream is only around 3% (assuming the diamond is sold for approximately $4,500).

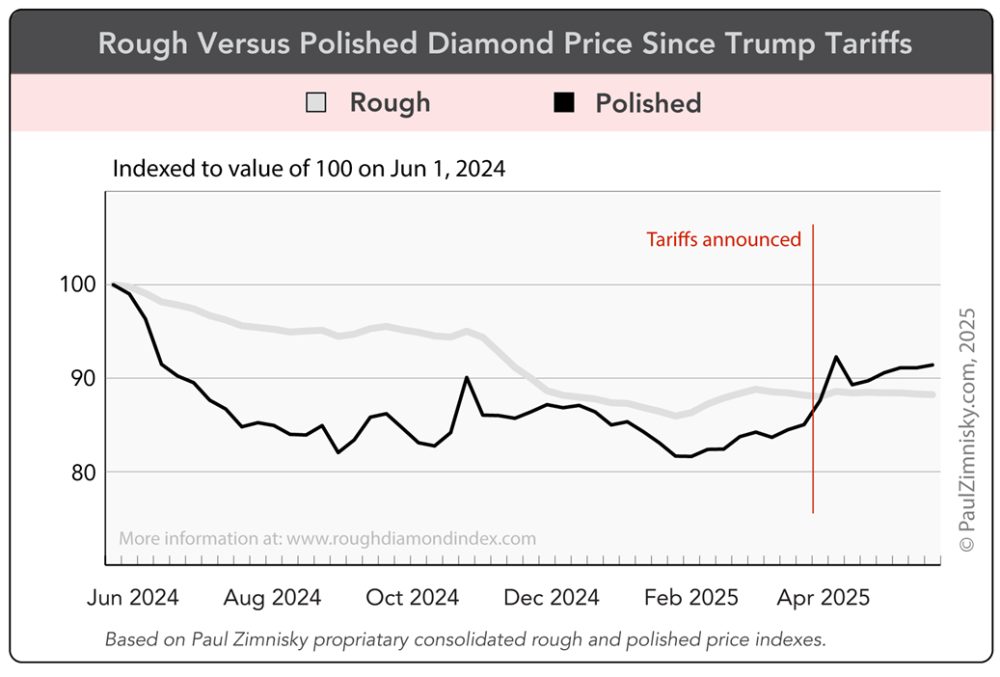

Uncoincidentally, the retail price of polished across categories in the U.S. is up about 2-3% since the tariffs were announced. The impact on rough has been nil given that the tariff only applies at the time goods are imported into the U.S., and the U.S. imports a negligible amount of rough. (See above chart)

The greatest impact of the tariffs on diamonds could ultimately be the more derivative consequences on America consumer sentiment and demand. Both of which have been shaken by the uncertainty of it all, driven by gyrating macro-economic forecasts and real-time volatility reflected in financial markets.

Despite this, consumer demand at the jewellery counter has yet to show a material pullback according to personal anecdotes and reporting by some of the largest jewellery players in the world.

On 3 June, Signet Jewelers, the U.S.’s largest diamond seller via stores including, Kay, Zales and Jared, said, “consumers are showing resiliency,” adding that it believes it can “navigate the tariffs.” The company even moderately upped the lower end of full-year sales and profitability guidance relative to its February forecast. Signet is now guiding $6.6-6.8 billion in sales for the fiscal year ending January 2026 – the mark implies sales unchanged from a year ago. The company’s shares, which trade on the New York Stock Exchange, bullishly rallied some 15% on the news.

A few weeks prior, Pandora, which is the world’s largest fashion jewellery brand, said “(we) have not yet seen any effects on our business from more cautious consumer behavior (related to the tariffs).” The company, which is based in Copenhagen, did slightly cut full-year sales guidance at the time, but attributed the move to foreign exchange fluctuations, i.e. weakness in the U.S. dollar. In calendar Q1, Pandora’s sales were up 8% versus a year prior, which was impressively the company’s 17th consecutive quarter of growth.

Pandora noted that it Increased prices 4% in April in response to higher precious metal prices, which followed a 5% increase in October 2024. Management implied that additional price increases are on the table, especially if U.S. tariff rates revert back to the initial higher levels. The company manufactures most of its jewellery in Thailand, which was first hit with a 36% tariff by the U.S. before being reduced to the base rate of 10%. The U.S. represents about a third of Pandora’s global sales.

Paul Zimnisky, CFA is an independent diamond industry analyst and consultant based in the New York metro area. For regular in-depth analysis and forecasts of the diamond industry please consider subscribing to his State of the Diamond Market, a leading monthly industry report; an index of previous editions can be found here. Also, listen to the Paul Zimnisky Diamond Analytics Podcast on Spotify or Apple Podcasts for exclusive full-length conversations with special guests from the gem and jewelry industry. Paul is a graduate of the University of Maryland’s Robert H. Smith School of Business with a B.S. in finance and he is a CFA charterholder. He can be followed on X @paulzimnisky and on YouTube @paulzimnisky.

Paul will be speaking at the Swiss Gemmological Society Central Conference in Wilen, Switzerland on 16 June, 2025 and the DMCC Lab Grown Diamond Symposium in Dubai, UAE on September 30, 2025.

Disclosure: At the time of writing Paul Zimnisky held a long equity position in Brilliant Earth Group and Newmont Corp. Paul is an independent board member of Lipari Mining Ltd, a publicly-traded Canadian company with an operating diamond mine in Brazil and a development-stage asset in Angola. None of the above constitutes investment advice, please read full disclosure at www.paulzimnisky.com.