Rising prices for larger rough diamonds point to a recovery that is uneven and concentrated at the top end. The trend raises a key question: is this the start of a broader rebound, or evidence of a more stratified market taking shape?

De Beers raised prices of 5-carat-plus rough at Sight #3 which took place in late-March, according to Paul Zimnisky sources. Reportedly, it was the third consecutive month that the company raised prices in the category. The trend is notable given the multi-year stretch of general apathy in the diamond market.

The relative uptick in larger rough could be a leading indicator of a broader recovery in natural diamonds, or it could (less-encouragingly) be indicative of a newly stratified market.

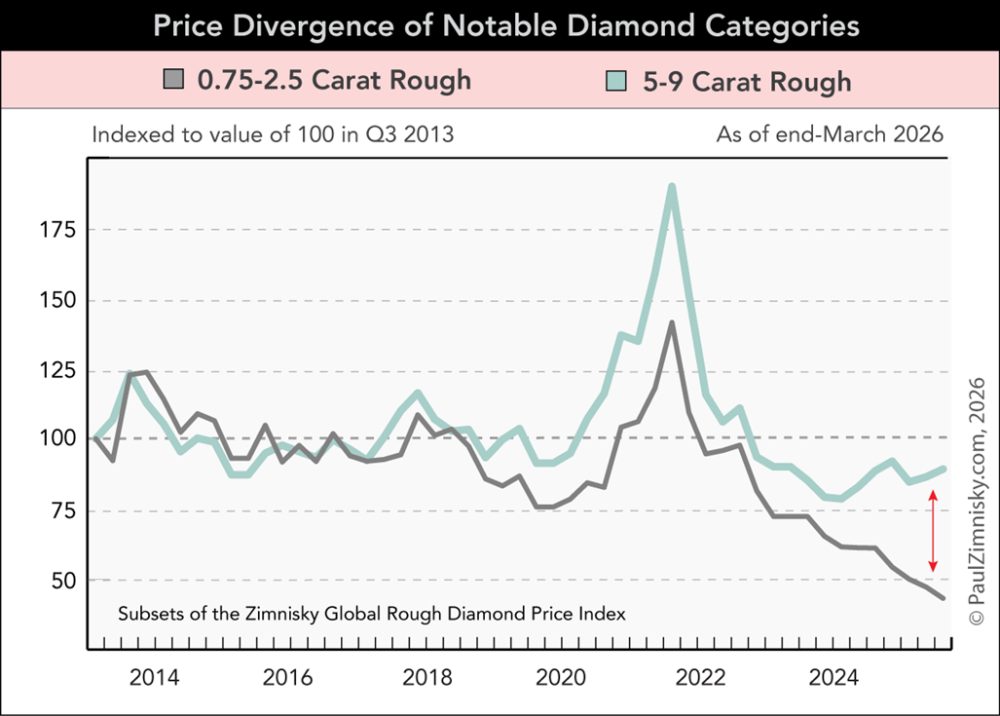

For context, 5-9-carat rough, gem as well as near-gem qualities, is up a low-to-mid-teens percentage year-to-date 2026, according to subsets of the Zimnisky Global Rough Diamond Price Index. This compares to consolidated 3-6 grainers (0.75 to 1.5-carat) and 2-2.5-carat categories which are both down a high-single-digit percentage YTD (see above chart).

The former represents 2- to 4-carat polished diamonds – which have been especially en vogue in certain fancy shapes as of late. The latter primarily transforms into traditional bread-and-butter 0.50- to 1.25-carat solitaries – goods that have axiomatically been losing out to top-quality 2-carat-plus lab-grown diamond (LGD) in recent years.

Historically, recoveries in the diamond market have been led by perennially desirable goods, for instance, higher-quality, larger engagement ring sizes – or, in rough parlance, 3-4 and 5-9 carat “White Gem Z.” Generally, lower quality goods in less desirable sizes are the last to recover. With the stock market similar dynamics tend to play out; for example, large-cap growth stocks tend to lead recoveries while smaller value stocks are usually the last to join the rally.

While the most desirable diamond categories are seeing notable price improvement in recent months, less-desirable product continues a multi-year trend of faltering –concerningly yet to show any meaningful signs of stabilisation.

The latter is ostensibly linked to the persistence of LGD taking share in lower budget categories. It remains to be seen whether demand, for say 1-carat natural, will ever regain (or even maintain) ground in the growing face of LGD.

Even with significant generalised supply cuts in the natural diamond market in recent years, there is no guarantee that categories most exposed to the mainstream introduction of cheap LGD will revert in price even as positive momentum plays out in select portions of the market.

Ultimately, the diamond industry needs to actively target and meaningfully support demand for wanning categories to win back share from LGD.

Optimistically, it seems clear that all else equal, most consumers would still prefer a natural diamond. This can be seen not only in celebrity engagement ring choices but also within more general classes of wealthier consumers, i.e. those with less financial limitations. This is presumably why the market for larger natural goods remains robust.

The middle-class consumer segment of the market is where the battleground principally lies – it is the consumer with a $3,000-5,000 budget that is choosing between a top-quality 3-carat LGD or a much smaller, lower-quality natural. As such, this is where the natural diamond value proposition really has to play out: a rare relic of nature that has profound authentic meaning in an ever-encompassing technological and digital world.

Also, with all the hype around gold lately, it is worth reminding consumers that jewellery-quality natural diamond is still significantly rarer and more valuable than the yellow-metal on a relative size and weight basis.

Paul Zimnisky, CFA is an independent diamond industry analyst and consultant based in the New York metro area. For regular in-depth analysis and forecasts of the diamond industry please consider subscribing to his State of the Diamond Market, a leading monthly industry report; an index of previous editions can be found here. Also, listen to the Paul Zimnisky Diamond Analytics Podcast on Spotify or Apple Podcasts for exclusive full-length conversations with special guests from the gem and jewelry industry. Paul is a graduate of the University of Maryland’s Robert H. Smith School of Business with a B.S. in finance and he is a CFA charterholder. He can be followed on X @paulzimnisky and on YouTube @paulzimnisky.

Paul will be giving a keynote presentation at the Canadian Jewellers Association Industry Summit in Toronto, Canada on October 26, 2026.

Disclosure: At the time of writing Paul Zimnisky held a long equity position in Brilliant Earth Group.