As US jewellers split between value and volume strategies, shifting consumer behaviour is reshaping demand and forcing the rest of the pipeline to adjust.

The US jewellery sector is showing signs of stabilising, but old models have been disrupted, and companies are finding growth through more targeted segmentation.

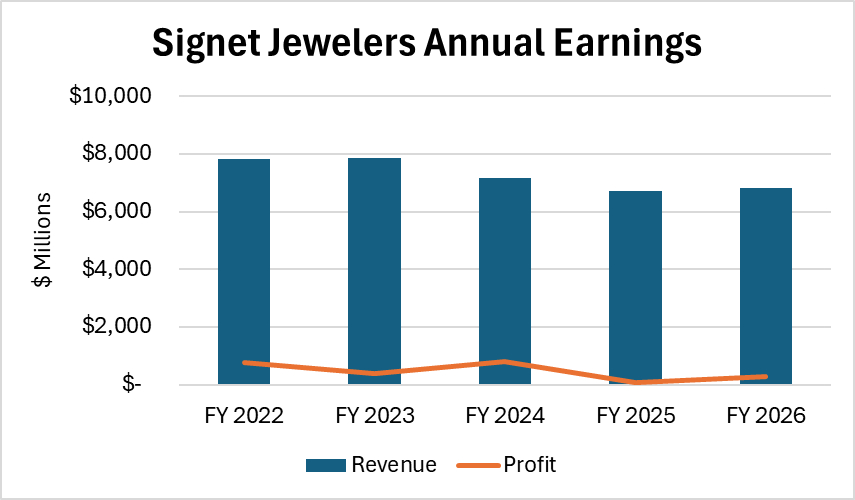

As always, Signet Jewelers serves as a bellwether of broader trends, given its position as the largest speciality jewellery group in the US. The company reported sales rose 2% to $6.81 billion in the fiscal year ending January 31, while profit grew fivefold to $294.4 million. Its performance was supported by higher ticket sales, tighter inventory control, and a more disciplined operating model.

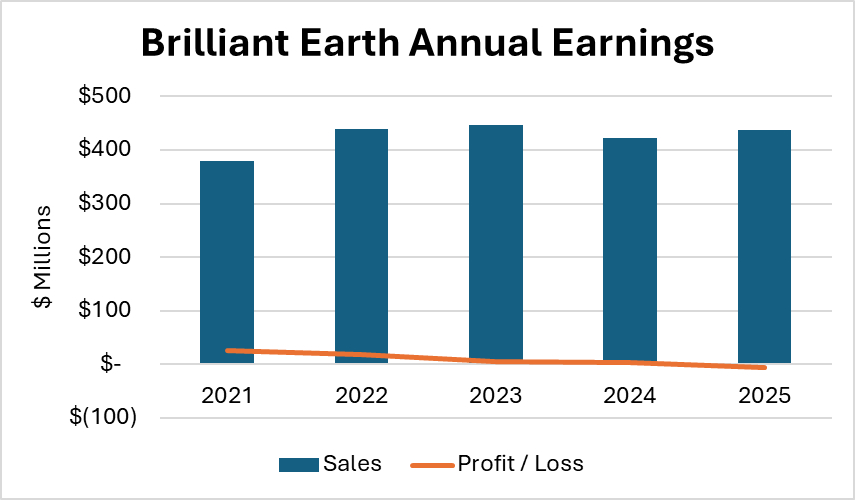

On the other side of the spectrum, Brilliant Earth saw sales increase 4% to $437.5 million during the fiscal year, though it swung to a net loss of $6.4 million from a $4 million profit the previous year. Its model is driven by higher volume, even as average transaction prices decline.

The two companies are not directly comparable given their scale and focus, but they reflect the value-versus-volume choice facing the retail sector, which this column has noted before and which is pushing the rest of the diamond pipeline to adjust accordingly.

Signet Refocuses

These differences became more apparent this earnings season through a clear shift at Signet Jewelers. While the company still relies on scale and continues to balance both approaches, pushing high-volume lab-grown diamonds in fashion and a more value-driven strategy in bridal, it announced a series of changes to its store network and brand portfolio that suggest it is moving toward a more focused, less-is-more approach.

The company plans to shut the James Allen brand by the second quarter, transitioning it into a proprietary collection within Blue Nile, which will serve as its flagship e-commerce platform. In addition, Rocksbox will no longer operate as a standalone brand and will instead be folded into Kay Jewelers, while the company evaluates the role of Banter, the teen-focused, lower-price fashion jewellery brand formerly known as Piercing Pagoda. Signet also announced the closure of 100 stores across its portfolio.

Streamlining toward a more focused model with clearer brand differentiation, part of CEO J.K. Symancyk’s Grow Brand Love program, marks a shift from Signet’s strategy under previous management.

Former CEO Gina Drosos targeted annual revenue of $9 billion, which she hoped the acquisitions of James Allen, Diamonds Direct, Rocksbox, and Blue Nile would help achieve.

She framed the company’s growth strategy as a win-win for the industry, stressing in 2021, “We want to make the pie bigger and get a bigger slice of the pie.”

The jewellery market, of course, was very different in 2021. It was in a post-Covid boom and still in the early stages of the lab-grown shift. By 2026, the industry is navigating volatile geopolitics, a more cautious consumer, and changing preferences among Gen Z, all of which have contributed to stagnant demand in terms of transaction volume.

Diverging Models

Signet Jewelers is compensating by pushing toward higher price points, including through its lab-grown offering, which allows for larger centre stones at price levels comparable to smaller, lower colour and clarity natural diamonds. The top-tier independents have adopted a similar approach.

The deeper shift is from a revenue growth focus, aimed at capturing a larger share of an expanding market, to a profit-driven approach built around a more streamlined portfolio. The assumption now is that the pie is not getting bigger, at least not in the current environment.

Signet is effectively saying that consumers are buying less often but spending more when they do. It is moving to a model that protects margins and leans on higher-income customers, while its core base remains the middle-income consumer, which is increasingly drawn to more affordable product lines such as lab-grown.

It appears that Brilliant Earth is doubling down on that middle-income consumer. Orders rose 13% in 2025, but average order value fell 8%. Growth is being driven by accessibility rather than premiumisation, weighing on short-term profitability. Demand is holding, but at lower price points.

Both companies recognise the trend but are responding in different ways. Brilliant Earth initially positioned itself as a premium brand and has diluted that as the lab-grown reality set in, while Signet Jewelers is trying to elevate its offering to better serve a more segmented consumer environment.

This divergence at retail is feeding back into the rest of the diamond pipeline. Demand for smaller, lower-quality goods remains under pressure, while larger, better-quality stones are comparatively resilient. That’s not a short-term imbalance. It reflects how demand is being redistributed, with value concentrating in fewer, higher-ticket purchases and leaving the volume segment increasingly exposed.

Structural Reset

The challenge facing the natural diamond industry is to broaden the scope of demand, though it will take a significant effort to revert to the old structure of broad-based consumption. De Beers’ Desert Diamonds campaign is an attempt to do that, promoting diamonds with warmer hues and tones and now extending that positioning into bridal. These are categories that were not traditionally embraced by consumers.

Still, the reality is that the market is unlikely to revert to its previous structure.

What’s taking shape is not a downturn in the traditional sense, but a reset in how the market functions. Consumers are buying less frequently but spending more when they do, and the market is adjusting around that behaviour. Segmentation is no longer a niche trend; it is becoming the structure of the business. Retail jewellers are jockeying for position, forcing the rest of the industry to follow. Those that don’t, risk waiting for a recovery that may not come.