The recent swings in US tariffs on Indian diamonds, with duties jumping from 10% to 50% in a matter of months, have thrown the global trade into uncertainty, disrupting supply chains and reshaping market expectations. Diamond analyst Paul Zimnisky breaks down what it means for the industry.

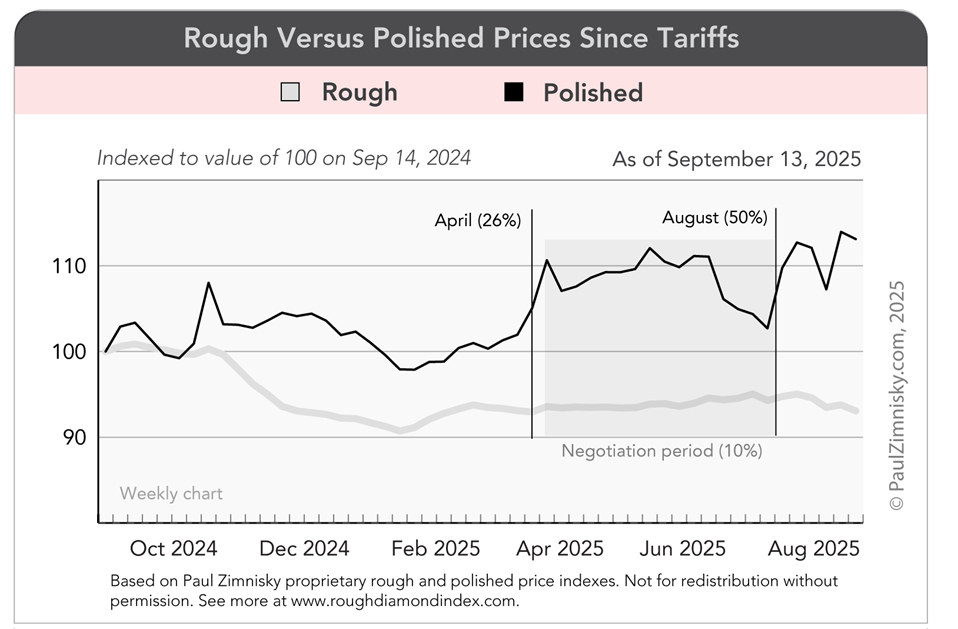

Since early-April, the volatile wave of US tariffs on India has sent the global diamond trade into a tizzy. The duty has fluctuated from 26%, to 10%, to 25%, and most recently 50%. Given that the tariff applies to where goods are “transformed” (cut and polished in the case of the diamond industry), the duty directly pertains any diamond manufactured in India that is imported into the US, which includes most diamonds feeding the US market given India’s preeminent position in diamond manufacturing.

The trade aggressively rushed goods to the US following a temporary reduction in the initial tariff on April 5 (from 26% to 10%) which the Whitehouse deemed a trade negotiation period (which applied to many nations including India).

In the subsequent four months, under the 10% tariff, many wholesalers and retailers in the US “front-ran” an overarching risk of a tariff hike in August. The risk materialised and on August 7 the duty was raised to 25%; and then doubled to 50% effective August 27. The second blow was beyond anyone’s expectations and ultimately rendered the related supply chain suspended.

As of mid-September, most Indian manufacturers are understandably hesitant to purchase regular quantities of rough due to concern that US demand will remain severely subdued in the near-term as the trade waits in hope for political negotiations to result in a tariff reduction (or in the best-case scenario an outright diamond exception). The timing is especially precarious given that the US trade is approaching prime holiday 2025 stocking season.

That said, in an August 21 episode of the Paul Zimnisky Diamond Analytics Podcast, Tom Moses, Executive Vice President of the Gemological Institute of America, estimated that upwards of 4-6 months of polished diamond inventory are in the US after business proactively stocked in prior weeks and months. Amidst the currently stalled trade, the inventory cushion is looking to be especially pertinent.

Optimistically, on September 10, both President Trump and Prime Minister Modi announced a resumption of trade negotiations following a multi-week stalemate. Trump stated: “I feel certain that there will be no difficultly in coming to a successful conclusion for both of our great countries!”

The news followed a US executive order released on September 5 which encouragingly included an “annex” that listed diamonds “unsorted, whether or not worked” as “potentially eligible for an exemption from duties.” The diamond industry has been actively lobbying in Washington in hopes of an exception given that diamonds are not “naturally produced in sufficient quantities in the United States to satisfy domestic demand.”

As it stands, the tariffs have seemingly disrupted a recovery in the natural diamond market that was emerging in the early months of 2025, which followed two and a half years of painful drawdown following a jubilant 2021 and 2022. According to the Zimnisky Global Rough Diamond Price Index, consolidated rough prices are flat year-to-date after being up as much as a low-single-digit percentage earlier this year (see above chart).

Consolidated global polished prices are up approximately 10% year-to-date, presumably skewed by the outsized share of diamonds in the US – the prices of which have been boosted by the embedded tariff. Netting out the impact of the tariff, it is estimated that polished prices are relatively flat in 2025.

Paul Zimnisky, CFA is an independent diamond industry analyst and consultant based in the New York metro area. For regular in-depth analysis and forecasts of the diamond industry please consider subscribing to his State of the Diamond Market, a leading monthly industry report; an index of previous editions can be found here. Also, listen to the Paul Zimnisky Diamond Analytics Podcast on Spotify or Apple Podcasts for exclusive full-length conversations with special guests from the gem and jewelry industry. Paul is a graduate of the University of Maryland’s Robert H. Smith School of Business with a B.S. in finance and he is a CFA charterholder. He can be followed on X @paulzimnisky and on YouTube @paulzimnisky.

Paul will be giving keynote presentations at the DMCC Lab Grown Diamond Symposium in Dubai, UAE on September 30, 2025 and the Prospectors & Developers Association of Canada (PDAC) Convention in Toronto, Canada on March 2, 2026.

Disclosure: At the time of writing Paul Zimnisky held a long equity position in Brilliant Earth Group and Newmont Corp. Paul is an independent board member of Lipari Mining Ltd, a publicly-traded Canadian company with an operating diamond mine in Brazil and a development-stage asset in Angola. None of the above constitutes investment advice, please read full disclosure at www.paulzimnisky.com.