Will diamond prices sparkle again in 2025? After a multi-year slump, the industry is poised at a crossroads. Diamond analyst Paul Zimnisky explores the delicate balance of macro-economic forces, evolving consumer preferences, and strategic industry initiatives that will determine the fate of the diamond market in the coming year.

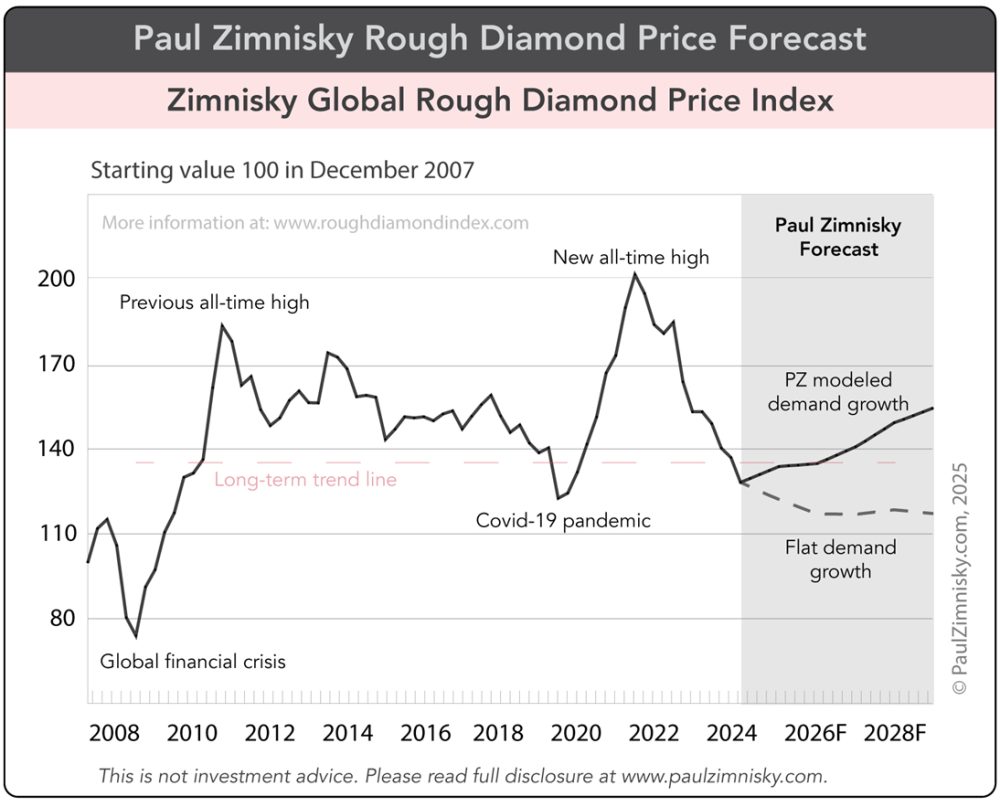

Through mid-February 2025, rough diamond prices are down a modest 1-2% year-to-date, according to the Zimnisky Global Rough Diamond Price Index. This follows an 18% decline in 2024 and a 15% decline in 2023. Rough prices are now down some 40% from the all-time high reached in the exuberant years of 2021 and 2022 where global diamond demand soared on the back of record economic stimulus in response to the pandemic.

The likelihood of natural diamond prices stabilising and subsequently recovering in 2025 and beyond lies in the balance of macro-economic variables in major consumer markets as well as more micro factors such as the magnitude and effectiveness of industry marketing and the trade’s ongoing efforts to positively differentiate its product from competing lab-grown diamonds.

Regarding the latter, potential catalysts include consumers’ (as well as jewellers’) dynamically changing perception of lab-grown versus natural diamonds at ever extreme price differentials and the industry’s aim to make easy-to-use consumer-facing natural diamond detection equipment ubiquitous in the consumer sphere (which was discussed on the January 23 episode of the Paul Zimnisky Diamond Analytics Podcast).

In the U.S., which represents over 50% of global consumer diamond jewellery demand, near-term macro drivers include the evolution of monetary policy, the impact of deglobalisation and the re-industrialisation of America under the new Trump administration.

Bernard Arnault, the CEO of LVMH, the world’s largest luxury company and parent of Tiffany & Co., recently described the U.S. as positioned for a “boom” given the new administration’s move to “cut the red tape…(and) appoint a person in charge of efficiency.” Arnault, who attended President Trump’s inauguration ceremony in Washington on 20 January, said, “there is momentum of optimism in the (U.S.) … taxes are going to go down to 15% … the workshops that we can build in the U.S. are subsidised in quite a few states, and the American president encourages this practice.”

In China, a post-pandemic recovery remains uncertain but has potential to significantly boost global diamond demand given the size of the market’s drawdown in 2024 – it is estimated that net diamond demand in China was down some 50%. A recovery will depend on China’s economy, PRC social policies related to luxury consumption, and consumer sentiment (more specifically sentiment towards diamonds which has recently waned as prices have dropped).

Commenting on China, Arnault said “I believe that the Chinese government is now aware of the fact that they need to kick-start the economy… (but) it’s going to take some time… what I expect is to see a gradual recovery… we’re going to get back to a normal situation after two years.”

Artificial intelligence will likely be a tailwind to global economic productivity in the coming years, but especially in the U.S. which should disproportionately benefit from domestic industry leaders including Apple, Microsoft, Google and Amazon. AI has the potential to boost the global economy the way that the mainstream introduction of the internet did three decades ago – with AI, the upside to productivity is almost immeasurable. Historically, diamond demand has correlated with global economic growth and perhaps in a world that is becoming ever more digital, natural diamonds will resonate with a population losing connection to the “real” world.

Irrespective of diamond demand, supply factors should be supportive of diamond prices for the foreseeable future. In February, De Beers cut 2025 production guidance by a third to 20-23 million carats. If the guidance holds, 2025 would mark the lowest output for De Beers since the company began publicly publishing production data in 2013. According to Paul Zimnisky forecasts, global rough diamond production will be just 105 million carats this year, which would be down marginally from last year – and 2024 was estimated to be the lowest year for natural diamond production since the 1990’s.

Taking the above factors into account, rough diamond prices are forecast to recover by a mid-single digit percentage in 2025, according to Paul Zimnisky analysis. The upside is expected to be weighed towards the back half of the year as supply-chain inventory positions gradually improve as the year progresses – which should be supported by the aforementioned strict supply curtailments upstream.

Paul Zimnisky, CFA is an independent diamond industry analyst and consultant based in the New York metro area. For regular in-depth analysis and forecasts of the diamond industry please consider subscribing to his State of the Diamond Market, a leading monthly industry report; an index of previous editions can be found here. Also, listen to the Paul Zimnisky Diamond Analytics Podcast on Spotify or Apple Podcasts for exclusive full-length conversations with special guests from the gem and jewelry industry. Paul is a graduate of the University of Maryland’s Robert H. Smith School of Business with a B.S. in finance and he is a CFA charterholder. He can be followed on X @paulzimnisky and on YouTube @paulzimnisky.

Paul will be speaking at European jewelry show INHORGENTA on February 22 in Munich, Germany. He will also be in Milan and Rome, Italy in late-February and can be contacted at paul@paulzimnisky.com to arrange a meeting.

Disclosure: At the time of writing Paul Zimnisky held a long equity position in Brilliant Earth Group and Newmont Corp. Paul is an independent board member of Lipari Diamond Mines, a privately-held Canadian company with an active mine in Brazil and a development-stage asset in Angola. None of the above constitutes investment advice, please read full disclosure at www.paulzimnisky.com.