The market continues to grow despite tariffs, high gold prices, rising crime and a shrinking store base, leaving sales in the hands of fewer but stronger players.

Fine jewellery continues to stand out in the US as one of retail’s most resilient categories, and it is on course to post another year of growth in 2025.

“There’s a lot of doom and gloom out there, but all the metrics are pointing to a healthy picture,” said David Bonaparte, CEO of Jewelers of America (JA), during a webinar on the State of the Jewelry Industry.

Jewellery and watch sales surged during the post-pandemic recovery and have held at those higher levels ever since, with the category crossing the $100 billion mark for the first time in 2024, according to the Bureau of Economic Analysis (BEA). That strength has carried into 2025 with sales rising 5% in the first 10 months of the year, Bonaparte added, citing the same BEA data.

While super-sellers like Signet Jewelers, Walmart and Amazon still command the largest market share, independent retailers are the ones driving growth, noted Michelle Graff, Editor-In-Chief of National Jeweler, during the webinar.

Gross sales at independent jewellers rose 13% year on year in October, according to The Edge Retail Academy, a consultancy that tracks the segment. The group reported an increase in every month of 2025 except February, when sales were flat.

Tariff, Gold Headwinds

This growth comes despite the broader pressures facing the retail sector.

At the top of that list are US import tariffs, including the steep 50% rate on goods sourced from India. Washington has already struck a deal with the European Union that exempts diamonds from these duties and talks with countries like Japan and Thailand are progressing. A US-India agreement remains the industry’s biggest priority because such a large share of global diamond supply is processed in India, Bonaparte stressed.

Midstream margins are already razor thin, so the added tariff burden has a significant effect on pricing, Bonaparte said. Still, US retail jewellery margins, however, have remained at roughly 50% even with these tariffs and elevated gold prices, he added.

Gold is currently trading around $4,100 per ounce, yet this year’s surge has not pushed retail prices high enough to put consumers off the metal, Graff noted. Many shoppers, particularly in the luxury segment, see gold jewellery as an investment that will hold value.

Even so, with some analysts forecasting that gold could cross $5,000 in 2026, pricing will remain a key concern for retail jewellers, Graff added.

Security & Skills

Beyond tariffs and gold, the sector is wrestling with two structural pressures: a rise in jewellery-related crime and a widening skills gap across the trade.

Retail crime has become a serious concern in the US market, with organised groups driving a surge in targeted attacks on jewellery businesses. Losses reached $142 million in 2024, a 7% increase on the previous year, according to the Jewelers Security Alliance (JSA). The trend has pushed Jewelers of America to support the proposed Combating Organized Retail Crime Act, which aims to strengthen penalties, improve coordination and give retailers more meaningful protection.

Meanwhile, workforce shortages are disrupting both retail and manufacturing, noted Rich Youmans, vice president of communications and publisher at Manufacturing Jewelers & Suppliers of America (MJSA).

Retailers are struggling to recruit and retain trained sales staff, and many employees have not received updated gemmology or product training for years. That lack of expertise directly affects margins because an undertrained salesperson cannot deliver the advisory-led experience fine-jewellery buyers expect, Youmans explained.

At the manufacturing level, bench jewellers, setters and casters are retiring and there are not enough skilled entrants replacing them. MJSA is trying to plug the gap through apprenticeship programmes, updated training platforms and a renewed push to position jewellery retail as a long-term career prospect, rather than a stopgap for entrants to the job market.

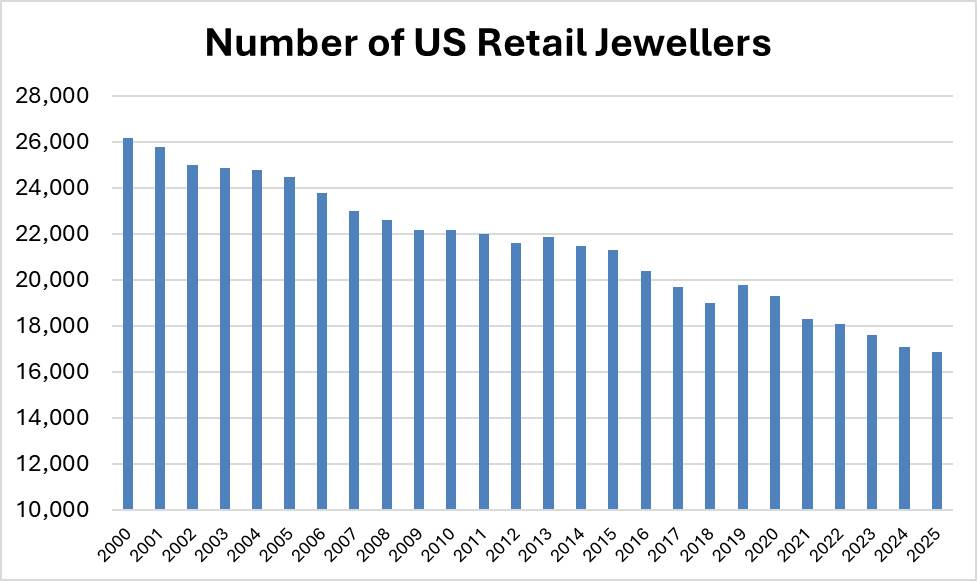

Industry Shrinking

These shortages come as the industry itself continues to contract. Store counts have been sliding for more than a decade, and closures still outpace new openings. Only 16,873 retail jewellery businesses were operating in the US in the second quarter of 2025, according to data published by Jewelers Board of Trade (JBT), a decline of 13% from 2020.

The sector may be posting healthy sales, but the base of businesses delivering those numbers is steadily thinning. That’s not necessarily negative for the trade, as it leaves the market with the stronger operators, while creating room for those prepared to confront the market’s structural challenges.

As jewellers push through the holiday season, many are taking stock of what has been a relatively solid year. Tariffs, gold prices and lab-grown diamonds will remain the dominant talking points in early 2026, yet sentiment remains broadly positive. Most believe the trade can continue to build on the elevated sales levels the market has sustained over the past five years, albeit with fewer jewellers positioned to reap the gains.

Avi Krawitz is the Founder of ‘The Diamond Press’ and a leading content creator and consultant in the diamond industry. He is widely recognised for his insightful analysis and storytelling, offering clarity to both industry professionals and curious consumers navigating a complex and evolving market. See more of Avi’s work at www.thediamondpress.com