Prices of larger diamonds were steady in November. The market for 1-carat diamonds weakened. Smaller goods showed the sharpest downturn as trends visible in recent months persisted.

Prices in India fell more sharply than in the US, reflecting the challenges that tariffs have created. The industry awaited news on a solution to America’s 50% import duties on Indian goods.

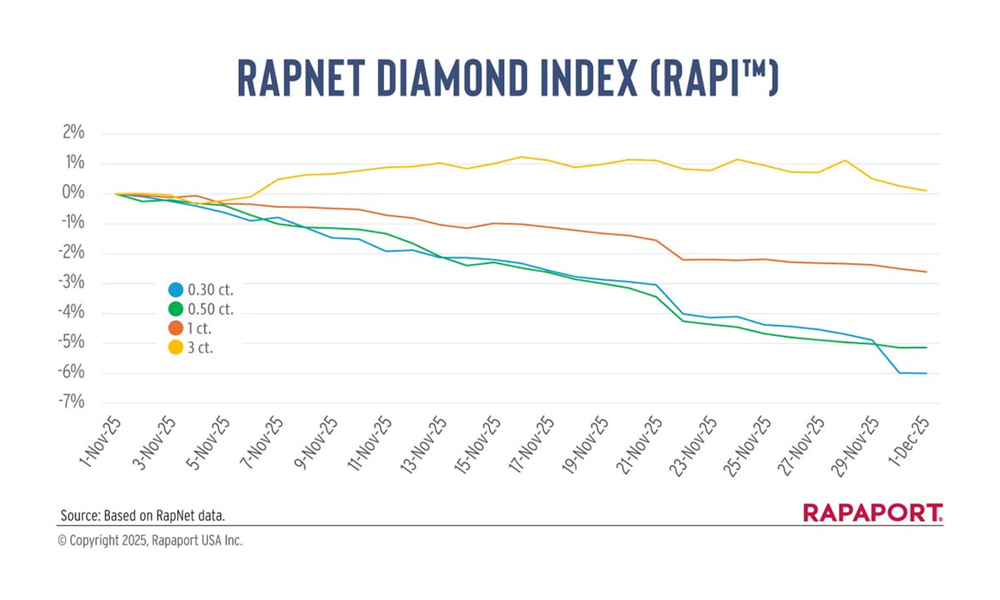

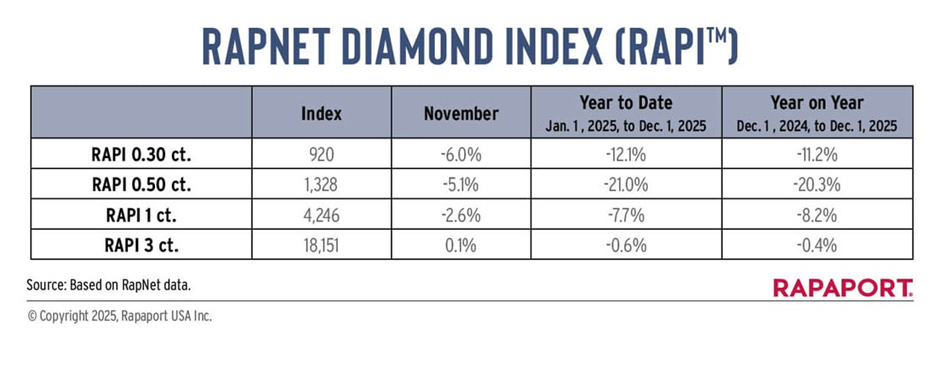

The RapNet Diamond Index (RAPI™) for 1-carat goods, which tracks round, D to H, IF to VS2 diamonds, dropped 2.6% in November. The RAPI slid 6% for 0.30-carat diamonds and 5.1% for 0.50-carat stones, while the 3-carat index went up 0.1%. Prices for round, 1-carat, D to H, SI diamonds fell 1.7%, according to RapNet data.

US demand was steady ahead of the holiday season, especially for 2- to 4-carat, F to J, VS to SI diamonds in rounds and long fancies. This supported prices. Overall online consumer spending reached new records on Thanksgiving and Black Friday. However, major US jewellers continued focusing on synthetics for fashion jewellery.

Indian domestic demand was positive. China’s appetite for diamonds remained low, but overall jewellery sales saw signs of stabilisation. The year-on-year revenue decline at Hong Kong-based jeweller Chow Tai Fook eased to 1.1% for the first fiscal half, while Luk Fook estimated a 20% to 30% revenue jump for the period.

Manufacturing in India slowed. India’s rough imports plunged 45% year on year to $385.4 million in October, reflecting the Diwali break and efforts to reduce inventories. De Beers kept prices stable at its November sight but gave customers full flexibility to refuse allocations. The miner’s rough remained more expensive than on the open market. Namibia reportedly expressed interest in buying a minority stake in De Beers.

The holiday outlook was mixed. Independent jewellers expected solid demand for large sizes in rounds and fancies. Special shapes, like marquise and old mine, are particularly popular.