US jewellery retailers are defying expectations in 2025, with both luxury powerhouses and value-driven brands posting solid growth. As the market reshapes itself, mid-tier players face a pivotal choice between volume and value — a turning point for the industry. Avi Krawitz decodes how US retailers are rewriting the playbook.

The major US jewellery retailers surprised many observers with stronger-than-expected sales in the first half of 2025. After three challenging years of inflation, shifting consumer priorities, and ongoing geopolitical uncertainty, recent earnings from Richemont, Signet Jewelers, Brilliant Earth, and Pandora suggest the market may be stabilising.

Together, these companies reflect three distinct segments of the jewellery consumer landscape — high-end luxury, middle-income households, and more affordable price points.

The luxury houses continued to outperform with solid growth in their US operations — Richemont’s Americas sales rose 17% year-on-year in the quarter ending June 30. Pandora, positioned at the low-price end of the market, posted 12% organic growth in the US over the same period.

By contrast, Signet and Brilliant Earth — both focused on middle-income households — delivered more modest revenue growth of around 3% in the second quarter, marking an improvement from the declines reported in previous years. Their performances highlight how the market is segmenting, particularly in relation to natural and lab-grown diamonds, and where consumer confidence shows early signs of returning.

Diverging Paths

Over the past three years, the top and bottom ends of the market have fared relatively well, as seen in the results of Richemont, LVMH, high-end independents, and Pandora. By contrast, the middle segment — where the majority of US jewellers compete alongside Signet and Brilliant Earth — has been squeezed.

Now, that middle segment is being forced to choose a path: lean into value, or push volume at lower price points.

What sets Signet apart is its scale, which enables it to play both sides — a strategy taking shape most clearly under its new CEO, J.K. Symancyk.

Brilliant Earth, meanwhile, also has the scale to straddle both, but its trajectory suggests a tilt towards volume.

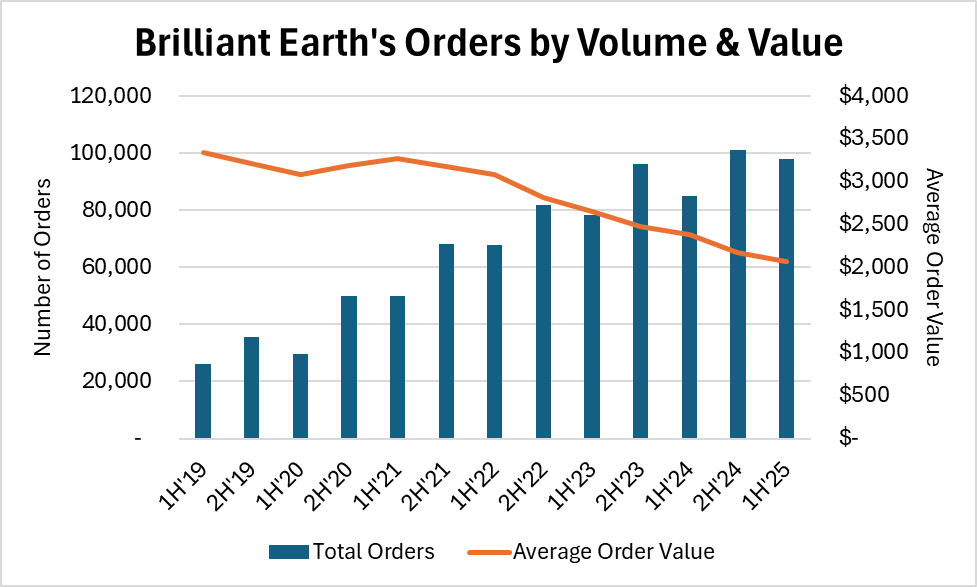

Brilliant Earth has steadily increased its sales transactions over the past six years, even as average order value dropped from $3,340 in the first half of 2019 to $2,068 in 2025 (see graph). CEO Beth Gerstein explained on the company’s earnings call that the decline reflects the rapid expansion of fine jewellery — up 38% year-on-year in the second quarter — which carries lower price points than bridal, alongside strong consumer demand for engagement rings under $5,000.

While this shift has pulled Brilliant Earth’s average order value down, engagement ring prices themselves have stabilised in recent quarters, underscoring how the brand is relying more on volume growth at lower average prices. Much of that decline has been fuelled by Brilliant Earth’s early embrace of lab-grown diamonds — first introduced in 2012 — which has diverted some bridal spend into lower-ticket synthetics rather than serving as a true alternative for value-conscious natural diamond customers.

Signet, meanwhile, is taking a more segmented approach. It is leveraging lab-grown to push volume in its fashion jewellery assortment, while positioning natural diamonds as the centrepiece of its bridal business and emphasising their value proposition. In doing so, the company is seeking to protect higher-ticket bridal sales even as it uses lab-grown to drive growth elsewhere.

In short, while Brilliant Earth’s trajectory reflects a clear shift towards volume at lower price points, Signet is deliberately separating the two categories — safeguarding value in bridal while using lab-grown as a tool to stimulate fashion jewellery demand.

This bifurcation is most visible at the extremes: luxury houses and high-end independents have doubled down on natural diamonds as a value anchor, reinforcing their brand propositions while delivering the strongest revenue growth and profit margins. At the other end, low-price players like Pandora have embraced lab-grown diamonds and are fuelling expansion through high-volume, low-value sales.

In both cases, these companies understand their position in the market and have a clear identity — something many jewellers in the middle have struggled to define as their space has gradually eroded.

Stuck in the Middle

The struggles of the mid-market are most evident among independents, who try to offer something for everyone with overlapping mixes of lab-grown and natural diamonds, but in the process weaken both their brand identity and growth prospects.

In some ways, Brilliant Earth mirrors that same challenge — blending lab-grown and natural across its assortment rather than segmenting the two. The difference is that it carries brand recognition, a sustainability mission that resonates, and a digital-first model that has enabled it to sufficiently increase its order volumes to offset lower prices. The average price may stabilise at some point, but for now the company continues to drift towards a lower-value, high-volume model.

What’s becoming apparent is that jewellers can no longer straddle both sides. The middle ground is shrinking, leaving US retailers at a tipping point: they must decide whether to position themselves on value or on volume. The return to growth in 2025 may be less about recovery, and more about showing there is potential in either path — provided the choice is deliberate and clear.

Avi Krawitz is the Founder of ‘The Diamond Press’ and a leading content creator and consultant in the diamond industry. He is widely recognised for his insightful analysis and storytelling, offering clarity to both industry professionals and curious consumers navigating a complex and evolving market. See more of Avi’s work at www.thediamondpress.com