Gold slithered in early December to a five-month low ahead of the US Federal Open Market Committee (FOMC) meeting, when the Fed announced the intention to raise the fed funds target rate for the third time in the year, according to the GFMS Gold Survey: Q4 2017 Review & Outlook published by Thomson Reuters.

This had been discounted by the markets and triggered a healthy gold rally to a year-end close of $1,241, a 12.5% intra-year gain en route to a test of $1,340 in mid-January. This four-week move equated to an 8% rise in dollar prices, and only 3% in euro terms—although the moves in rupee and renminbi were 5% and 6% respectively. This move was propelled in good part by the replenishment of COMEX long positions that had been sold down ahead of the FOMC meeting, and covering of shorts similarly.

ETF holders, by contrast, were net G Crypto-currency Frenzy Hits US Gold Investment In 2017 sellers over the period although in the latter part of January they are adding holdings. On balance the prevailing circumstances point to a period of price consolidation with underwhelming demand in the physical market. While physical buying is enough to keep a floor under the price, upside potential will, as usual, be driven by professional flows. The environment suggests that the future risk in the price lies to the upside.

A review of the fourth quarter of 2017 shows the physical market broadly in balance. Jewellery fabrication picked up with its usual seasonal strength, and indeed all the major regions recorded year-on-year gains. However, if we strip out exceptionally low offtake in 2016, this was the lowest Q4 outcome since 2012.

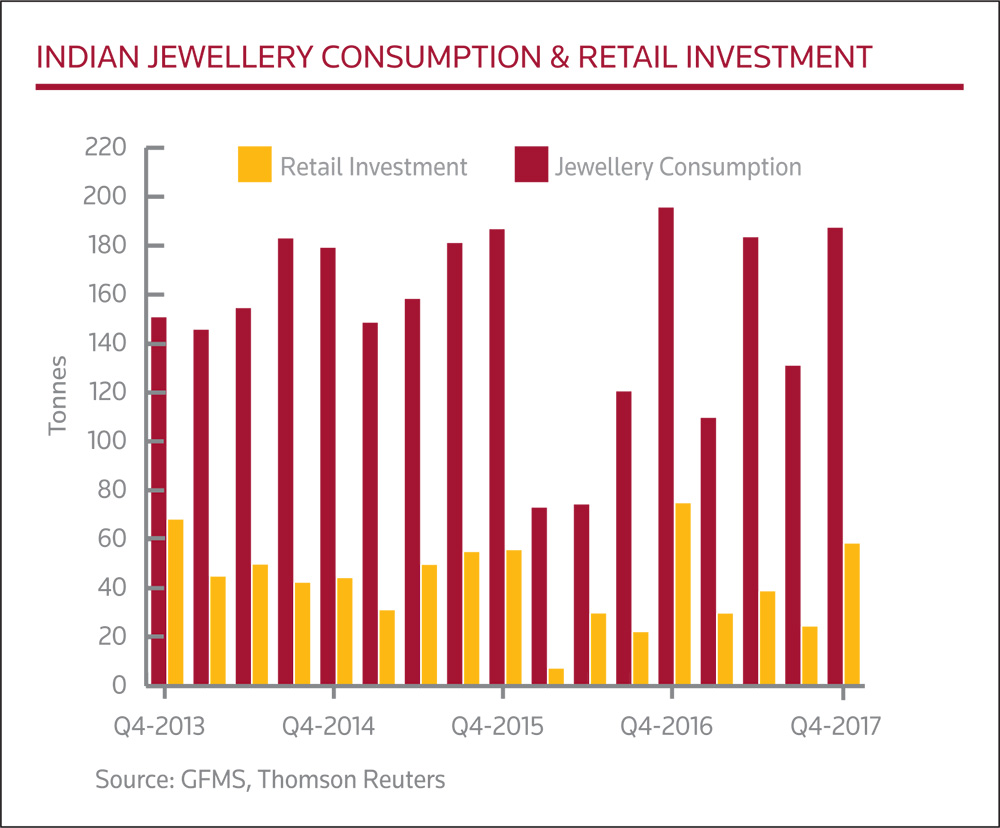

Jewellery consumption, while 3% lower than Q4 2016, marginally exceeded fabrication levels. Among the largest consumers, jewellery demand in India increased by 8% in the final quarter, helped by a surge in sales during auspicious Dhanteras and lower prices later in the year, resulting in fresh restocking by jewellery fabricators. That said, this was a comparison against a very low base in 2016 and Q4 offtake was down by some 12% against Q4 2015.

Chinese demand slipped by 2% year-on-year, with ongoing losses in the pure gold segment as consumer preferences continued to shift towards more fashionable, but lower gold content pieces. It does appear that younger Chinese jewellery buyers are increasingly viewing the sector as adornment rather than investment and we expect volumes to remain under pressure. There is pent-up demand for investment bars, however, although this will need stimulus from an improving price and resurgence in price expectations.

Elsewhere in the investment sector, US retail investment in coin and bars was down 55% year-on-year to 10.1 tonnes. Coin fabrication was down approximately 75% year-on-year and sales were the lowest in a decade, hindered in some part by the rise in enthusiasm for cryptocurrencies. There has been growth in the secondary market, with discounts to newly-fabricated products falling to as little as 50 basis points during the year. Globally, retail investment in the quarter was 11% down on Q4 2016 with a large number of countries posting losses.

ETF investment, meanwhile, which lies more in the domain of institutions, fluctuated in a narrow range of just 24 tonnes of 1% with a net loss of five tonnes and a net dollar outflow of $200 million, thus giving a net increase of 170 tonnes over the year.

Price and market outlook

The geopolitical climate and potential equity market problems will continue to support gold’s role as a risk hedge. GFMS argued three months ago that there is growing risk in equities and while strength has persisted, it continues to believe that the markets need to brace themselves for a sharp correction once the feeding frenzy abates. In this event, gold would also be likely to stage a sharp downward correction due to its role as an insurance policy and also in the race for liquidity, although one of the major reasons for the latter has weakened, with the SEC now applying two days’ settlement for brokerdealer trades, as against t+3 hitherto, although t+3 still applies to a large number of stock markets. Gold’s role as a risk hedge will remain supportive as rising tensions in Europe and a somewhat spontaneous approach from President Trump are raising uncertainty levels.

“In the physical markets, Indian demand is set to remain at levels similar to 2017, while Chinese investment demand will likely pick up if we see gold’s price momentum being renewed going forward. We expect gold prices to average $1,360/ oz and hit a 2018 peak of over $1,500/oz later in the year. Our forecast discounts three Fed rate hikes, although a potential overheating from the effect of the new tax reform could lead to more aggressive tightening, limiting gold’s upside. The forecast for the annual average is unchanged from our view of three months ago, although we have extended our upside targets as we are expecting increased price volatility this year,” GFMS said.