After four years of price swings, the diamond market is stabilising in early 2025. Following steep declines in 2023 and 2024, diamond expert Paul Zimnisky analyses the recent uptick in rough diamond prices, exploring supply cuts, emerging demand, and whether this vitality signals a lasting shift—or just a pause in the volatility.

After a bumpy start to 2025 diamond prices settled down in February and have since begun to show some signs of vitality going into March.

For context, as of the week ended 15 March, rough prices are up about 3% over the last 30 days and now up 2% year-to-date, according to the Zimnisky Global Rough Diamond Price Index (ZGRDPI). The trend is notable, as it follows an 18% decline in prices in 2024 which followed a 15% decline in 2023.

At Okavango Diamond Company’s March auction, like-for-like prices were up some 9% relative to January. Despite a modest $37 million sale (compares to over $100 million sold in March 2023), 96% of lots offered were sold and the relative sale-over-sale price change was the best for Okavango since January 2022.

As a note, Okavango is the Botswana government’s independent selling arm of Debswana goods – Debswana is the De Beers/Botswana joint venture.

The recent price action is likely a reflection of the strict industry-wide supply curtailment strategy currently being employed. In February, De Beers cut 2025 production guidance by a third to 20-23 million carats (gross of government joint ventures). If the guidance holds, 2025 would mark the lowest output for De Beers since the company began publicly publishing production data in 2013. According to Paul Zimnisky forecasts, global rough diamond production will be just 105 million carats this year, which would be down marginally from last year – and 2024 was estimated to be the lowest year for natural diamond production since the 1990’s.

That said, there are some positive demand drivers that seem to be emerging as well. Anecdotes emanating from the trade’s midstream indicate that a diamond supply chain is finally reaching levels where restocking is necessary again –following two years of bloated inventory. This is most pronounced in select polished categories for now, however, it could serve as a leading indicator for the larger market.

For example, there are reported shortages of smaller higher-quality goods as well as 1.5-carat-plus sizes, especially 2.5-carat-plus, notably in certain fancy cuts. This is starting to translate into demand for corresponding rough categories –as was seen in the recent Okavango auctions. For example, “+5 +3 White Gem Z” and “5-9 Carats White Gem Z” goods are both up almost 10% year-to-date – clearly outperforming almost other rough categories.

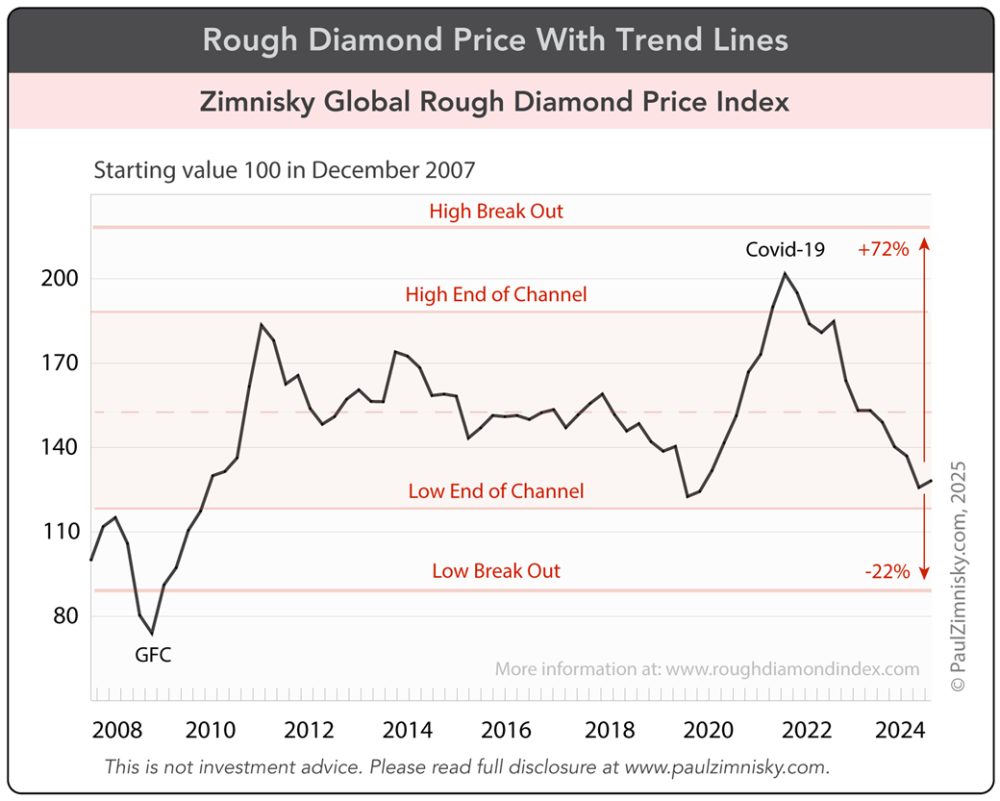

Taking a step back, despite neck-breaking volatility over the last four years, diamond prices have traded in a channel formation since 2010 – with the peaks marked by the post-Global Financial Crisis rebound in early-2011 and the pandemic high in Q1 2022 and the troughs marked by the pandemic low in Q2 2020 and the current lull.

Using the ZGRDPI as a proxy, from current levels, prices would need to increase upwards of 70% or fall over 20% to decisively break out of this 15 year-long trading channel (see above chart).

Paul Zimnisky, CFA is an independent diamond industry analyst and consultant based in the New York metro area. For regular in-depth analysis and forecasts of the diamond industry please consider subscribing to his State of the Diamond Market, a leading monthly industry report an index of previous editions can be found here. Also, listen to the Paul Zimnisky Diamond Analytics Podcast on Spotify or Apple Podcasts for exclusive full-length conversations with special guests from the gem and jewelry industry. Paul is a graduate of the University of Maryland’s Robert H. Smith School of Business with a B.S. in finance and he is a CFA charterholder. He can be followed on X @paulzimnisky and on YouTube @paulzimnisky.

Paul will be speaking on “What the Future Holds for Diamonds” at the Swiss Gemmological Society Central Conference in Wilen (Sarnen), Switzerland on June 16, 2025.

Disclosure: At the time of writing Paul Zimnisky held a long equity position in Brilliant Earth Group and Newmont Corp. Paul is an independent board member of Lipari Diamond Mines, a privately-held Canadian company with an active mine in Brazil and a development-stage asset in Angola. None of the above constitutes investment advice, please read full disclosure at www.paulzimnisky.com.