China-based industry analyst Liang Weizhang examines the evolving dynamics of China’s jade market amid shifting economic tides, emerging substitutes, and changing consumer values. He offers a perspective on how tradition, innovation, and market forces are converging in this iconic segment.

Throughout Chinese civilisation, jade has occupied a revered place — not merely as a decorative gem, but as a vessel of moral philosophy, identity, and continuity. In the commercial realm, too, jade has long held its ground as the second most significant segment within China’s jewellery market, trailing only gold. However, recent shifts in both macroeconomic conditions and consumer preferences have challenged its stability, revealing a sector in the midst of realignment.

A Market of Cultural Weight Facing Structural Shifts

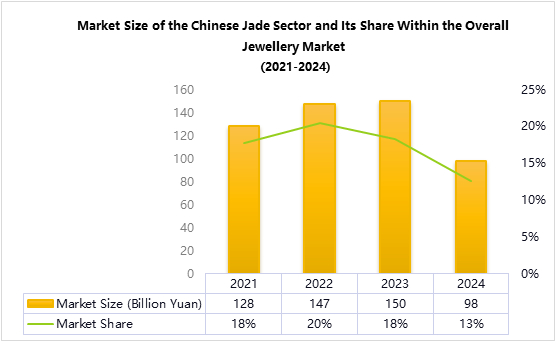

From 2021 to 2023, China’s jade market demonstrated resilience and steady growth, expanding from RMB 128 billion to RMB 150 billion and maintaining a consistent 18-20% share of the national jewellery market. However, 2024 marked an abrupt disruption. The sector’s total value fell to RMB 98 billion — a 35% year-on-year decline — bringing its market share down to just 13%.

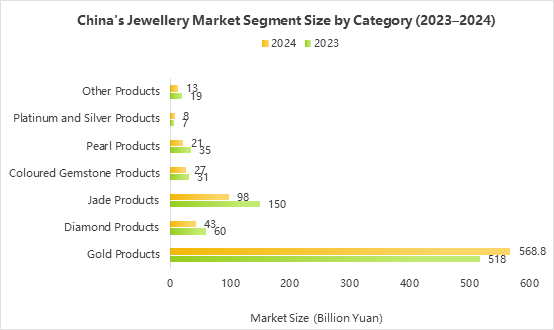

This contraction occurred against a broader backdrop of economic headwinds. The overall Chinese jewellery market shrank from RMB 820 billion in 2023 to RMB 778.8 billion in 2024, as rising gold prices and cautious consumer sentiment redirected purchasing priorities. Within this landscape, gold retained its appeal as both adornment and financial hedge, while jade and diamond categories saw declines.

Core Segments: Jadeite and Nephrite

In Chinese culture, jade has long carried meanings far beyond ornamentation. As the classical saying goes, ‘Of all the stones that are beautiful, we call them jade’. This definition embraces a wide spectrum of mineral aggregates — from jadeite and nephrite to chalcedony, agate, quartzite, serpentine, Dushan jade, turquoise, lapis lazuli, and malachite, etc.

Today, however, jadeite and nephrite dominate China’s commercial jade sector. Nephrite, widely known in China as Hetian jade, has been used in Chinese civilisation for over 10,000 years. Its smooth, lustrous quality was praised in Confucian philosophy, where jade was seen as an embodiment of virtue, harmony, and self-cultivation. Yet despite this profound cultural significance, nephrite plays a relatively modest role in today’s market — valued at around RMB 33 billion, or just 4% of the jewellery sector in 2023.

Jadeite, by contrast, rose to prominence only in the Qing Dynasty, when rich colours and translucency became fashionable. Sourced mainly from Myanmar, jadeite now leads the category, with a 2023 market size of RMB 115.7 billion — about 14% of China’s jewellery market. Its shorter history is offset by enduring popularity and status appeal.

China’s jadeite market is highly sensitive to supply conditions in Myanmar. Following disruptions in previous years, the 2024 Myanmar government-run tender resumed normal operations, with supply volumes increasing by 51% year-on-year. Although premium-quality rough stones remain scarce, the normalisation of tenders is expected to revitalise downstream demand by improving supply chain predictability.

At the same time, Guatemala has become an important secondary source, now accounting for around 30% of China’s jadeite imports. However, its material generally lacks the vivid colour saturation and translucency of Burmese jadeite, limiting its use in premium jewellery.

New Entrants: The Disruptive Rise of Feizhou Cui

A particularly salient development in 2024 was the ascent of Feizhou Cui (literally translated as “African Jadeite”), a quartzite material that closely resembles jadeite in appearance but is significantly more affordable. As consumers pivot towards value-driven purchases in an era of economic downturn and falling discretionary income, Feizhou Cui has emerged as a compelling alternative.

For example, a Feizhou Cui bangle mimicking the appearance of high-grade jadeite may cost only a few thousand yuan, compared to over RMB 100,000 for its genuine counterpart. This cost-performance gap has positioned Feizhou Cui as a rising favourite in the mid- to entry-level market, particularly among younger and first-time buyers.

More than a trend, Feizhou Cui’s momentum reflects a deeper recalibration. Retailers, facing declining margins on traditional categories like diamonds, are diversifying their inventories to include materials that offer attractive mark-ups and rapid turnover. For many, Feizhou Cui is more than a substitute — it is a commercial lifeline.

Conclusion: Navigating Complexity with Nuance

The contraction witnessed in 2024 may not signal a decline in jade’s cultural relevance, but rather an inflection point in how that relevance is expressed and monetised.

While China’s jade market has historically been shaped by domestic players — from sourcing to processing and retail — recent developments, such as the rise of Feizhou Cui, suggest new opportunities on the horizon. The growing popularity of visually appealing, high-quality mineral aggregates, highlight a key consumer trend: aesthetic value at attainable price points.

For international stakeholders, this presents a strategic opening. Although few foreign suppliers are directly involved in China’s jade segment, the evolving landscape suggests room for thoughtful participation — particularly through the identification and introduction of alternative ornamental stones that resonate with Chinese tastes and values. The next chapter of China’s jade story may be shaped not only by cultural continuity but also by an expanded palette of global materials — redefined by both tradition and innovation.

Liang Weizhang, CEO of HubWis Jewellery Strategic Creations (Guangzhou) Co., Ltd., is a senior analyst and strategic researcher in the jewellery industry. He is the founding President of the Guangzhou Diamond Exchange and Vice Chairman of the Guangdong Gold Association. With nearly 30 years of experience in the diamond, gold, and jewellery sectors in China and internationally, Liang offers deep industry insight and a strong professional network. His company supports jewellery businesses with strategic consulting, industry advice, and access to global markets.