The global diamond market showed mixed trends in March, as the Middle East conflict escalation February 2026 added fresh pressure on trading activity. Iranian missile strikes disrupted key hubs, freezing trading in Israel and Dubai and forcing rough tender houses to relocate sales, Rapaport said in a press release.

The market remained divided by size categories. Demand held firm for larger stones, particularly 2-carat and above goods, which were in short supply. Long fancy shapes saw strong demand, while major wholesalers in New York reported steady retail orders.

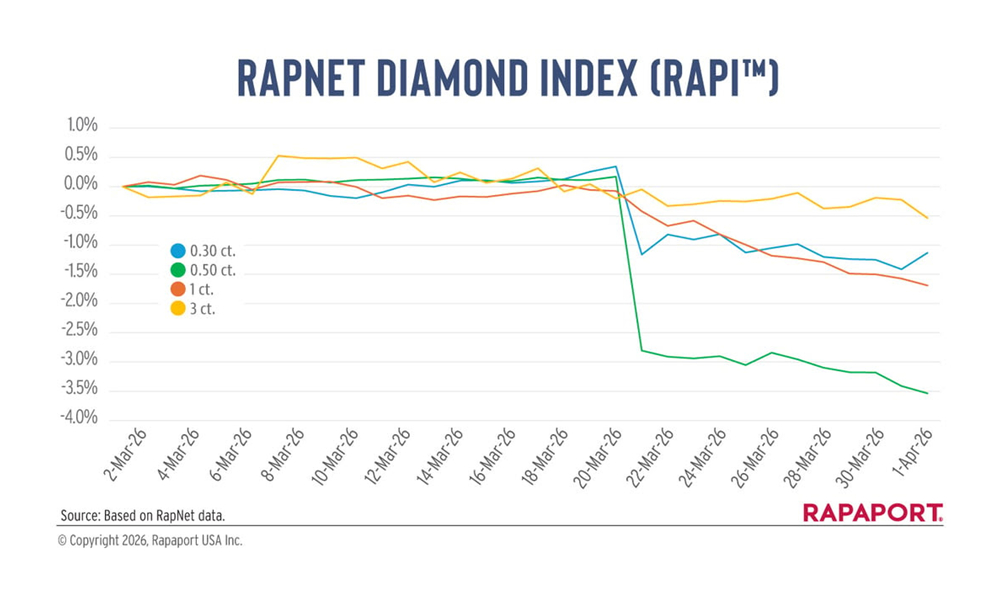

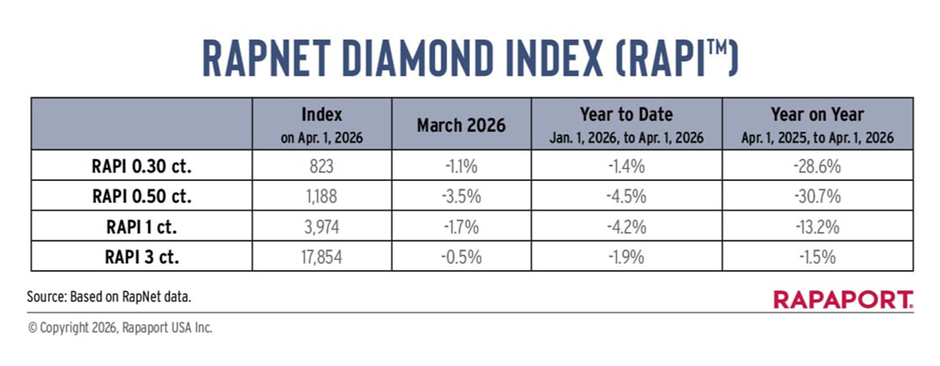

Smaller diamonds continued to weaken. The RapNet Diamond Index (RAPI™) for 1-carat goods fell 1.7% in March, while 0.30-carat and 0.50-carat stones declined 1.1% and 3.5%, respectively. The 3-carat index slipped 0.5%. Adjustments to the Rapaport Price List on 20 March reflected these trends, particularly for rounds up to 1.99 carats and pears under 0.99 carats.

US tariffs on Indian goods, though reduced to 10% in February, remained a worry for dealers. Supply concerns also emerged around Indian manufacturers’ access to rough, especially as tender houses shifted locations due to disruptions in Dubai.

Larger rough diamonds, particularly 5 carats and above, remained in tight supply, with reports of price increases at De Beers’ March sight. The miner also reduced its sightholder base by 20-25 clients from 69 for the new contract period beginning 1 July, signalling tighter supply dynamics.

On the retail front, Signet Jewelers reported sales of $6.81 billion for the fiscal year ending 31 January, up 1.6% year-on-year. The company is closing its James Allen platform and integrating it into Blue Nile, which will focus more on natural diamonds.