Global Q2 gold jewellery demand dipped 2% to 510.3 tonnes largely due to a weaker Indian market, according to the World Gold Council’s (WGC’s) latest Gold Demand Trends report. Challenging conditions in a few markets were the main reason for the year-on-year global decline in Q2 gold jewellery demand.

India and the Middle East were the main drivers of the decline, although weakness in those markets was partly offset by growth in China and the US. Comparing H1 2018 with H1 2017, demand was little changed: 1,031.2 tonnes compared with 1035.8 tonnes, WGC said.

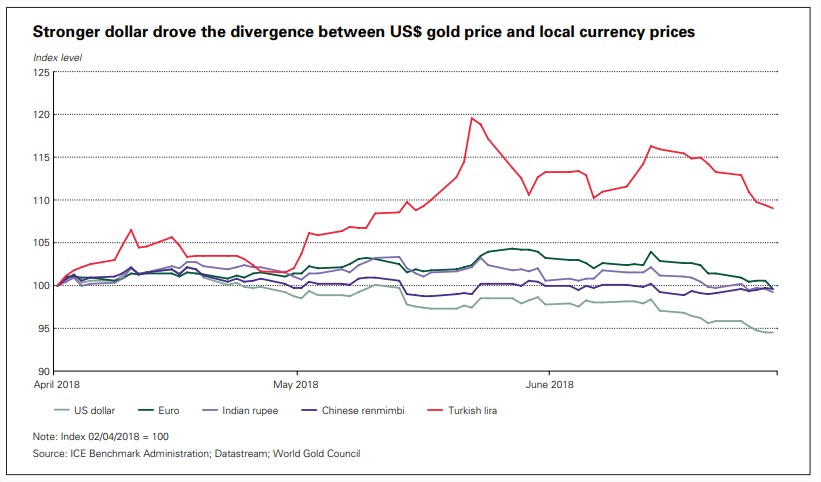

“It may seem surprising that gold jewellery demand failed to perk up in response to the relatively sharp decline in the US$ gold price over the quarter. But currency weakness in many markets meant that local consumers did not benefit from similar gold price reductions; instead they were faced with steady – or even higher – prices,” the report said.

WGC noted that Indian gold jewellery demand was down from a strong Q2 2017, falling 8% to 147.9 tonnes due to high local prices and seasonal factors, but was in line with the longterm average. The year-on-year drop in demand was magnified by the jump in demand seen in Q2 last year when consumers rushed to make gold purchases before GST was implemented on July 1st. In a longer-term context, Indian jewellery demand was relatively healthy, just 1% below the five-year quarterly average of 149.1 tonnes and 3% higher than average Q2 demand over the preceding ten years (144.1 tonnes).

According to the report, Indian gold demand was boosted in April by Akshaya Tritiya and the wedding season, before fizzling out. “India’s gold trade reported brisk demand during the festival, despite relatively high local gold prices at that time. And weddingrelated purchases supported demand early in the quarter. This positive effect soon wore off however, as the rupee continued to weaken against the US$, keeping the domestic gold price elevated,” it said.

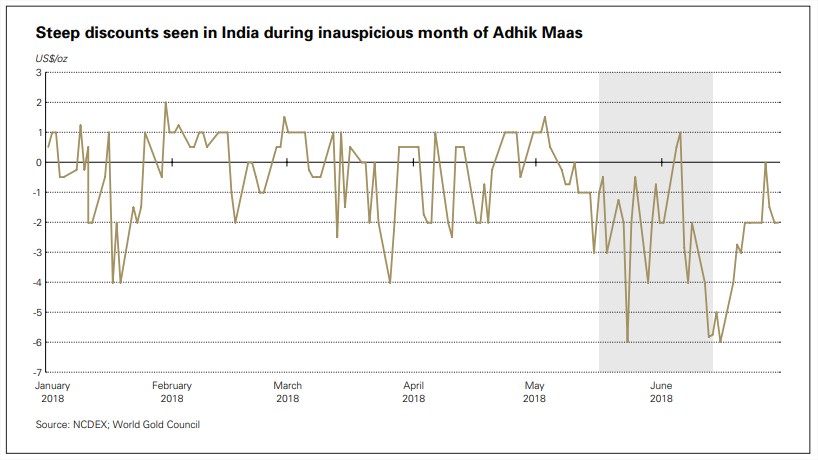

Adhik Maas – an inauspicious time for Hindus – was also a contributing factor to the yearon-year decline. Adhik Maas is an additional month in the Hindu calendar, which occurs every 30-36 months in order to align the lunar and solar calendars. It is considered an inauspicious time for events such as weddings, so tends to have a dampening effect on gold jewellery demand. The start of Adhik Maas in mid-May coincided with the local gold price moving quite sharply into discount versus the US$ price.

The imminent monsoon kept demand subdued towards the end of the quarter. Although the inauspicious Adhik Maas period ended on June 13th, it was rapidly followed by the onset of monsoon preparations among rural communities, aided by government attempts to boost farm incomes (such as loan waivers and raising Minimum Support Prices on certain crops). Farming communities were heavily involved in sowing crops ready for the monsoon – often a time during which gold is used as collateral for loans to buy seed rather than to purchase gold jewellery.

Similarly, economic factors and a new VAT regime in some markets hit Middle Eastern demand. Gold jewellery demand in the Middle East dropped 12% to 42 tonnes in Q2 versus a year earlier. On the other hand, Chinese gold jewellery demand extended its recent recovery, gaining 5% to 144.9 tonnes in Q2. Year-to-date demand reached a three-year high of 332.9 tonnes. Chinese consumers responded well to industry focus on innovation and branding, WGC noted. US jewellery demand, too, continued along its recent path of steady growth: demand grew 5% to a ten-year Q2 high of 28.3 tonnes.

Total gold demand

Global gold demand remained muted in Q2 2018 at 964 tonnes, 4% below the same period in 2017, according to the WGC. Global bar and coin investment was virtually unchanged at 248 tonnes. Stronger demand in China and Iran – fuelled by increasing geopolitical tensions with the US – were offset by falls in Turkey, India and Europe, where local prices remained elevated.

Central banks added 89t of gold to global official reserves in Q2 2018, down 7% compared with Q2 2017. Cumulative H1 2018 purchases of 193 tonnes were the highest since 2015. Alongside the familiar list of Russia, Turkey and Kazakhstan, the Reserve Bank of India returned to the market, albeit with only a very small purchase (+2.5 tonnes).

Alistair Hewitt, head of market intelligence at the WGC, commented: “It’s interesting how investors around the world have reacted to some of the risks stalking financial markets.

Weaker economic prospects and tumbling currencies off the back of heightened tensions with the US boosted Chinese and Iranian gold demand, while US investors shrugged off any geopolitical concerns. Demand from tech companies continued to grow, with H1 demand reaching a three-year high, while economic growth boosted jewellery demand in the US with Q2 demand hitting a ten-year high.”

The total supply of gold increased by 3% in Q2 2018 to 1,120 tonnes, supported by increased mine production and recycling growth. Mine production in Q2 saw a rise of 3% to 836 tonnes, the highest Q2 on record, as projects in Russia, Indonesia and Canada continued to ramp-up. Gold recycling also grew, as currency weakness in India, Turkey and Iran boosted local gold prices and encouraged consumers to lock in profits from their holdings.