Diamond analyst Paul Zimnisky reports that the momentary let-up in the expectational stone market may be partly due to the volatile global macro-economic conditions affecting buyer confidence and purchasing power. Nevertheless, the long-term value of diamonds as a tangible and rare asset remains strong, and the market is expected to rebound as the global economy stabilises.

In late-January, Tiffany & Co. announced that it had acquired a final “small cache” of Argyle pinks and purples (plus an incredibly rare red) directly from producer Rio Tinto.

The assortment of 35 stones, now dubbed “The Tiffany Collection,” was recovered during the final stretch of operations at the Australian mine before it was permanently closed in November 2020.

With the world’s primary source of fancy-pink diamonds now depleted, many industry prognosticators and collectors see the stones as a prudent investment.

Perhaps more importantly, in an industry known for the saying “the big (and in this case fancy) diamonds sell the small ones,” the exceptional stone market remains important as ever for the natural diamond industry, especially as it jockeys for position with the mainstream emergence of lab-grown diamond jewellery.

In a press release, Tiffany noted that it will be leveraging the stones’ “extraordinary Australian provenance” as a way to promote the company’s Diamond Craft Journey initiative –providing its customers with the region or country of origin of every newly sourced diamond—a primary strategy being employed by the natural diamond industry as a way to further differentiate its product.

While Tiffany nor Rio disclosed the price paid for the Tiffany Collection, notably in 2014, a seemingly small 2.1-carat heart-shaped Argyle red diamond sold for approximately $4.5 million, or $2.2 million on a per-carat-basis. While not nearly as rare as reds, but still extremely rare, good samples of Argyle pinks have reportedly sold for high-six-figures per-carat in the recent past.

Commenting on the purchase, Tiffany CEO Anthony Ledru told the New York Times that the price paid was “probably not enough compared to what (they are) going to become in the next five, 10 years.”

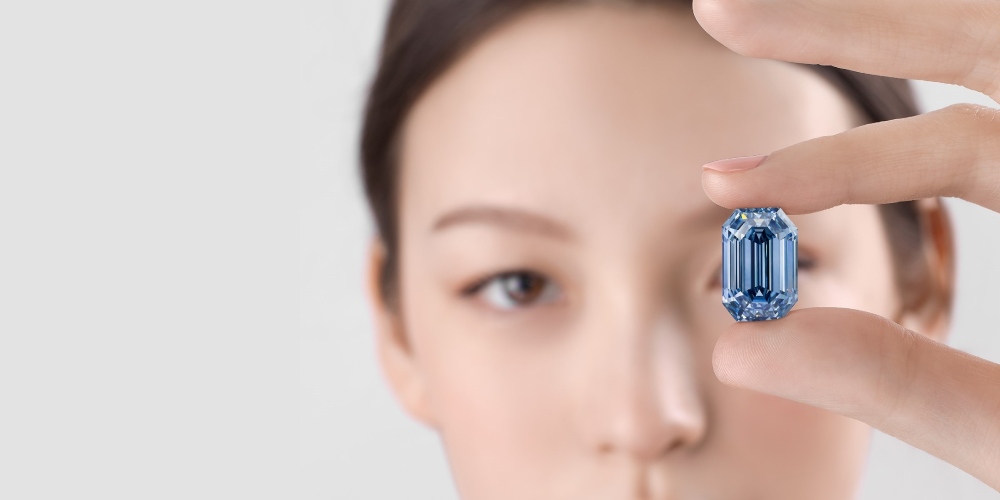

This past October, the “Pink Star” a 11.5-carat “cushion mixed cut” internally flawless, fancy vivid-pink, sold for upwards of $58 million – making it the second most expensive diamond ever sold at auction. The diamond was produced by Petra Diamonds at its Williamson mine in Tanzania in late-2021 – not to be confused with the “Williamson Pink Diamond” owned by Queen Elizabeth II.

The sale followed the “De Beers Blue,” a 15.1-carat emerald-cut internally flawless, fancy-vivid blue which went for $57 million in April 2022. The stone was recovered by Petra at its infamous Cullinan (previously Premier) mine in South Africa just a few months prior.

However, the exceptional stone market hit some resistance in the second half of 2022, with three fancy-blue diamonds (from one collection) notably failing to sell at auction.

In November, the first stone, a 5.5-carat, which was estimated by Sotheby’s to sell for $11-15 million, did not reach the reserve. Then in December, a 3.2-carat was pulled from auction, and a 2.1-carat, estimated by Sotheby’s to sell for $1.2-1.5 million, did not reach the reserve either. The diamonds (now 8 polished stones) were cut from five rough stones named “The Letlapa Tala Collection,” which were produced by Petra at Cullinan in 2020.

There is speculation that the result was due in part to the volatile global macro-economic backdrop in recent months, but more particular to the expectational stone market, typical very-high-end diamond buyers in China and Russia being impacted by Covid-related restrictions and Western sanctions, respectively.

Paul Zimnisky, CFA is a leading independent diamond industry analyst and consultant based in the New York metro area. For regular in-depth analysis of the diamond industry please consider subscribing to his State of the Diamond Market, a leading monthly industry report; an index of previous editions can be found here. Also, listen to the Paul Zimnisky Diamond Analytics Podcast on iTunes or Spotify. Paul is a graduate of the University of Maryland’s Robert H. Smith School of Business with a B.S. in finance and he is a CFA charterholder. He can be reached at paul@paulzimnisky.com and followed on Twitter @paulzimnisky.

Disclosure: At the time of writing, Paul Zimnisky held a long equity position in Lucara Diamond Corp, Brilliant Earth Group, Star Diamond Corp, Newmont Corp and Barrick Gold Corp. Paul is an independent board member of Lipari Diamond Mines, a privately-held Canadian company with an operating kimberlite mine in Brazil and a development-stage asset in Angola. Please read full disclosure at www.paulzimnisky.com