Last year was, without doubt, one of the worst years for diamond companies. The impact of reduced supplies by producers in the last quarter of 2015 is finally being felt in the market, with prices moving up in a few categories. However, we need to realise that the market equilibrium has changed and companies have to learn to live with the volatility or perish.

Diamond jewellery demand growth and diamond PWP demand growth are different and do not necessarily move in tandem. As the diamond industry, our concern is more with the PWP growth.”

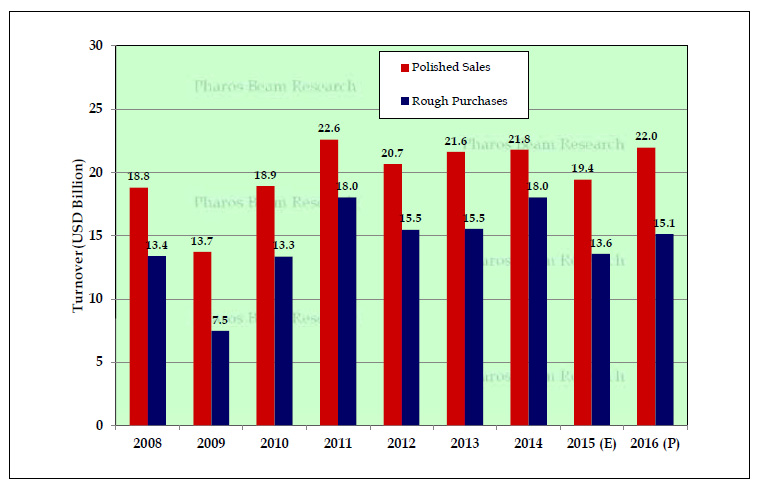

After 2009, 2015 was probably the worst year faced by the midstream. While 2009 was caused by external factors which created a demand shock, this was only a small factor in 2015. It was the other actions by all entities in the diamond pipeline which amplified these rather small fluctuations.

A quick enumeration of these factors affecting 2015 is required to understand how these would play out in 2016.

- Retail jewellery demand challenges (in local currency)

- Dollar strength (leading to weakness in dollar demand for jewellery and polished)

- Polished price drop and impact on polished wholesale price (PWP) growth

- Retail and jewellery industry de-stocking

- Wholesale (midstream) de-stocking

- Producer actions (or inactions)

- Absence of margins in manufacturing

Most of these points have been covered in depth through industry reports published by highly regarded consulting firms and by industry analysts. I will focus on only a few aspects.

One aspect to consider is that while the first two points are external and hence independent factors, the other factors are all internal and, in many cases, a logical consequence of the pressures on the industry. They are also temporary and will stabilise/reverse over time. They amplify the impact of the demand drop.

The other aspect is that diamond jewellery demand growth and diamond PWP demand growth are different and do not necessarily move in tandem. As the diamond industry, our concern is more with the PWP growth. The inherent assumption analysts make is that diamond content in retail remains the same. This does not hold in instances where there is sharp price movement.

Consider an example. If the diamond content in the jewellery is 30%, for every $100 of jewellery sold, the polished which is sold is $30. Consider that the price of diamonds quickly drops by 10%. Retail prices are sticky and retailers do not adjust their retail prices. This means that if the retail prices are not adjusted, the PWP demand drops to $27, for the same $100 of jewellery sold. Hence, the PWP demand will drop by 10%, even though the jewellery demand stayed the same. For the retailer, this would show up as a 3% increase in the margin.

In reality, a portion of this drop would be passed on as discounts to consumers. The portion which is retained by retailers becomes the effective the drop in PWP for the industry. The same effect can be triggered by higher operating costs or greater margins demanded by retailers. The long stocking cycle for retailers also complicates this transmission. These effects were clearly visible in 2015.

Automatic improvements

Expectations for 2016 need to be built upon the understanding of the factors which affected the markets in 2015, and examining their relevance.

These factors can be broadly clubbed into two categories. The first category is demand-related factors. Indications from the US, China, India and other markets suggest that going forward the demand will be steady. Also, if the actions by the recently created Diamond Producer’s Association (DPA) bear fruit, there should be demand growth. This alone should put a floor on the market.

The second category is the internal stocking-related parameters. All these factors worked to amplify the demand factors in 2015. In 2016, even if these parameters remain at their new low levels, the lack of negative impetus from these factors would automatically mean that the demand for polished and rough would naturally be higher than in 2015. The industry will see this happening in 2016, as most of the demand and stocking-related parameters would have played out, and new sales requiring restocking from the retailers.

These projections have an implicit assumption that the industry will work on significantly higher margins. If that assumption does not hold, and the industry decides to go back to working on slim margins, the rough sales could be higher. The industry pays more for the rough from its own pocket. In that case, 2016 would still remain a better year in turnover, however, it might not be a profitable one!

The better top-line forecast hides another important issue: the industry structure has fundamentally changed from that of low volatility, to increasingly showing signs of sustained higher volatility. The industry will simply need to live with it!

Higher price volatility

Most industries strive to ensure a stable pricing regime. The diamond industry was one of the few industries which were able to successfully do so for decades. It is interesting to examine the conditions which encourage stability and why these conditions might not be achievable for the diamond industry over the next few years.

Monopolistic or oligopolistic structure A monopolistic structure or an industry with a cartel is the easiest way to ensure market stability. While the diamond industry had the former, other industries, like oil producers had the latter. In both cases, long periods of higher prices could be maintained.

The diamond industry benefited from this structure for over 50 years with De Beers and the CSO (Central Selling Organisation). Regulators are unlikely to allow such structures to form again. Untimely actions by large market participants can easily tilt the balance of demand and supply over the short run, causing volatility.

What is clear, based on the actions in 2015, is that producers were behind the curve in terms of their responses to the issues. Whether this was accidental or by design is not immediately evident.

Coming into 2015, most producers had projected higher production in 2015. However, the stress in the markets was already visible at that point. With differing priorities and commitments, producers continued to produce at higher levels for the first six months of the year. Subsequently, one of the largest producers has cut back production, while the other has kept up the pace.

It is hoped that the producers have learnt from their mistakes. However, there are indications that a few producers are considering scaling back production, just when the market indicates that there will be an uptake in demand!

Stockpile or in the ground If you look back at the history of diamond prices, for years you could have drawn a straight line showing a 2-3% annual price growth, and you would possibly have been right. The price swings started kicking in from 2008 onwards, after De Beers had exhausted its famous stockpile of diamonds.

There is simply no better way to reduce volatility than by using a stockpile. However, reports from producers, barring one, indicate that with the new financial realities, they probably have a reduced appetite to mine and stockpile rough diamonds. Most prefer to slow down on the production and stockpile the diamonds in the ground.

Unfortunately, both cases are not necessarily the same. Even in the case of the most efficient manufacturer, ramping up production is a 2-4 month exercise. Apart from ramping up the mining activities, other downstream activities, including assortment of the rough and its sale take time. In the current fast-changing market, a three-month delay in the goods reaching manufacturing can introduce greater volatility. After all, timing is everything!

Leaner supply chains

The retail and midstream diamond industry has also seen a de-stocking trend over the last year. Inventories across the pipeline were reduced as a response to lower demand expectations as well as pressures from banks. Given the current high risk perception of the industry by the banks, it is unlikely that there would be increased availability of finance over the next few years. This would mean that the industry would need to keep its stocks in check.

A leaner pipeline brings with it greater volatility, as perfectly logical and efficiency-driven decisions by market participants amplify volatility. This is because the pipeline loses its ability to manage the small mismatches between demand and supply, and these are, in-turn, passed and amplified through the chain and manifest themselves in price volatility. With the liquidity pressures faced by the industry, along with the potential interest rate hikes, it is unlikely that companies would be allowed to re-stock to the level of a few years ago, thus making the pipeline prone to volatility.

Fractured demand

Diamonds are a non-homogeneous product. We simply cannot take hundred 1-cent stones and make them into a 1-carat stone! This means that the demand and supply has to be in balance for each category of product. The periods of pricing anomalies are a testament to this.

On the demand side, we see that sales are increasingly being driven by price points. This focus pushes retailers to use similar qualities of diamonds, so that they do not look overpriced. Countries like China have slowly down-traded in both sizes and qualities of diamond used over the last four years.

This increases the pressure on the quality of diamonds which are “in demand”. The production from the rough boxes is not so finely tuned. It gives a spread of product, which means that the diamonds which are not in demand end up in stock. Hence prices could again spike for a few qualities, while leaving the broader market unmoved.

Newer sources of volatility

Lab-grown diamonds are a potential substitute to natural diamonds. The possible mixing of these diamonds with natural diamonds also introduces an element of volatility for the natural diamond supply chain. This is likely to unsettle markets until lab-grown diamonds establish themselves as a different category of product.

A response to this threat would need to be on several fronts, including developing detection equipment, along with increased testing at all transactions. The uncertainty over the when and the how much of the lab-grown diamond supply also increases the potential volatility for the industry.

Managing volatility

Increased volatility has been a feature of many industries and it is instructive to look at the ways in which they have managed the higher volatility.

Flexible manufacturing

One response, which diamond companies also demonstrated, is to have a more flexible factory, especially in the range of products which can be manufactured. Currently we need different capabilities to handle single larger stones, as compared to the traditional parcel-based polishing factories. Polishers are also trained to work on a narrow product range. This will need to change as factories will have to respond to varying demand patterns.

The same goes with the sales and marketing teams, who would need to adapt to shifting product profiles. Polishers usually graduated from smaller stones to larger, higher-value stones. During the previous year, many companies actually went back to smaller and cheaper goods, which augers well for flexibility of their factories.

On the capacity side, this means that factories should be built only if the marketing and demand generation mechanism exists. Creating infrastructure without the sales channels will severely constrain the flexibility of the company.

Managing stocks

The industry, especially the Indian manufacturers, had developed this mindset that stock is good. They were following a stock-and-sell model, or in other words, if you have the stock, you can sell it. That mentality needs to change, as holding stock no longer guarantees margins.

In leaner supply chains, getting held up with the wrong kind of stock could mean a significant loss, while holding on to the right kind of stocks could result in profits. While speculation is any one’s guess, the best strategy would be to focus on the stock levels which are necessary and sustainable for your business, and then ensuring that the stocks are maintained within those levels.

This has far-reaching consequences for retailers and jewellers as well. The retail end had pushed the onus of stocking back to the midstream. A leaner midstream would mean that purchase prices would again be more volatile.

Higher margin and “volatility premium” Rough parcels always produce a spread of polished, depending on how well they have been assorted. This means that greater attention needs to be paid at the time of rough purchase. The margins are only achieved when the entire polished production of the parcel is sold.

Anecdotal evidence suggests that a polishing company which went bankrupt in 2015 was working on margins of R100-200 ($1.5-3) per stone, most of which were in those categories requiring certification. Working on such low margins in high volatility markets is a recipe for disaster.

Apart from the regular margins, companies should consider whether there is a “volatility premium” which is available on the goods. Simply put, if you were to take out an insurance against a price drop, you would pay a premium to the insurer. You, in turn, need to ensure that any rough you buy provides you that “premium” in addition to the regular returns which you would like to make on your capital. To put this in perspective, even a credit insurance, which is a simpler product with significant caveats, charges up to 0.5% on whole turnover policies. Clearly, for price volatility the “volatility premium” should be much higher!

The only beneficiary from the lowering of the pipeline volatility is the producers. Any lowering of margin expectations and the “volatility premium” manifests itself into higher rough prices. That is the reason why the CSO years were successful for De Beers. They ensured that the pipeline volatility was low, enabling higher rough prices in turn. That assumption now needs to be reset.

2016 will surely be a healthier year for the diamond midstream industry as turnovers rise again. This is more due to the negative factors of 2015 playing themselves out, rather than anything else. However, companies need to adjust to a different market reality, where volatility is a way of life, if they would like to thrive in the future.

It will call for more strategic planning by companies, wherein restraint is shown in rough purchases and stocking, along with more flexible factory and sales capabilities.

Ultimately, it boils down to the simple fact that the companies cannot be successful in these volatile markets, without having the cushion of additional margin or the “volatility premium”.

Hopefully, companies will recognise this volatility risk and will not overpay for the rough in 2016!