Natural diamond producers are prioritising market stability over volume growth, keeping output tightly managed as the sector moves through a gradual recovery phase, notes diamond analyst Paul Zimnisky.

In early-February, De Beers’ parent Anglo American reiterated an approach to “align (diamond) output with prevailing demand” and consequently cut 2026 production guidance to rather wide range of 21 to 26 million carats, down from a previous 26 to 29 million carats.

The move follows a similar adjustment to early last year when Anglo cut De Beers’ 2025 guidance to 20 to 23 million carats, significantly down from the previous range of 30 to 33 million carats.

The latest development is indicative of a natural diamond market that is still jockeying for a recovery following three consecutive years of recession.

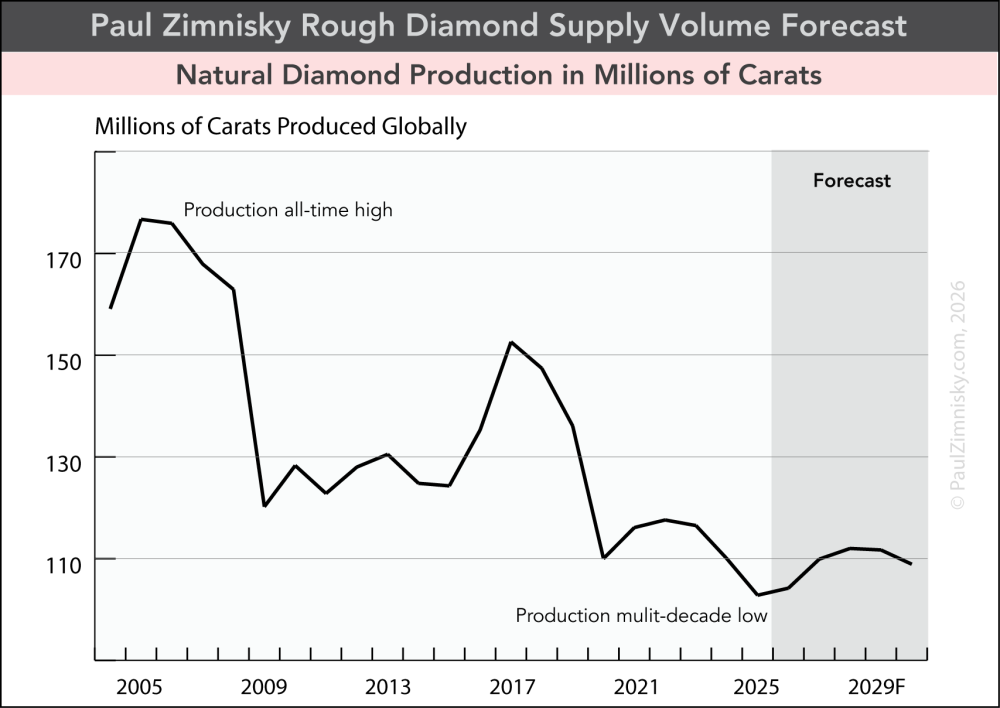

Globally, natural diamond supply was estimated at just over 100 million carats last year, according to Paul Zimnisky estimates, marking the lowest annual output since 1992. In 2026, supply is forecast to just moderately rebound to around 105 million carats. For context, this is down from over 150 million as recently as nine years ago (see above figure).

While the current aggressive paring of supply is due in part to legacy mines reaching depletion (production that is not being replaced with new sources), the aforementioned De Beers “supply control” strategy is unequivocally the most poignant factor. It is estimated that De Beers is currently producing at as much as 35% under capacity. Russia’s ALROSA, the world’s largest producer by volume, is also presumably producing at below capacity, albeit at a more moderate 15%, according to Paul Zimnisky estimates.

This mechanism means that as natural diamond demand returns, over 10 million carats of additional production can theoretically be turned back on in relatively short order. Longer term, higher prices could economically drive green- or brownfields development which could take production somewhere around the midpoint of current levels and the highs of 2017.

De Beers and ALROSA currently account for about half of global production by volume (taking into account the curtailed output) with the balance coming from Angola’s Endiama, independent producers and less-commercial alluvial operations, which only represent a single-digit percentage of global supply.

Why almost every other major producer has recently cut supply, Endiama has steadily grown output to over 15 million carats in 2025 – double the level from just five years ago. The company, which is primarily a state-owned entity, operates two of the largest diamond mines in the world: Catoca and Luele. A production ramp-up in the latter has been the primary driver of its supply growth.

Supply by independent producers has notably fallen off in recent years. For example, Petra Diamonds has seen its output fall by some 25% to under 3 million carats relative to five years ago as its two key assets, Cullinan and Finsch, become more difficult and costly to operate with age. Burgundy Diamond’s Ekati mine has seen its production halve to under 3 million carats in recent years as the mine requires costly capex to maintain full operations –conditions which have been squeezed by the softer diamond market.

Finally, Rio Tinto, one of the world’s premier diversified miners, is currently in the process of closing Diavik due to economic depletion – its only remaining producing diamond mine. Daivik produced upwards of 7 million carats annually as recently as 2019.

Paul Zimnisky, CFA is an independent diamond industry analyst and consultant based in the New York metro area. For regular in-depth analysis and forecasts of the diamond industry please consider subscribing to his State of the Diamond Market, a leading monthly industry report; an index of previous editions can be found here. Also, listen to the Paul Zimnisky Diamond Analytics Podcast on Spotify or Apple Podcasts for exclusive full-length conversations with special guests from the gem and jewelry industry. Paul is a graduate of the University of Maryland’s Robert H. Smith School of Business with a B.S. in finance and he is a CFA charterholder. He can be followed on X @paulzimnisky and on YouTube @paulzimnisky.

Paul will be giving a keynote presentation at the Prospectors & Developers Association of Canada (PDAC) Convention in Toronto, Canada on March 2, 2026.

Disclosure: At the time of writing Paul Zimnisky held a long equity position in Brilliant Earth Group and Newmont Corp. Paul is an independent board member of Lipari Mining Ltd, a publicly-traded Canadian company with an operating diamond mine in Brazil and a development-stage asset in Angola. None of the above constitutes investment advice, please read full disclosure at www.paulzimnisky.com.