Industry analyst Paul Zimnisky explores how a widening wealth gap is reshaping the diamond and jewellery market, forcing brands to pivot as affluent buyers spend bigger while aspirational consumers pull back.

While the diamond industry has grappled with its own specific share of challenges over the last five years, including category dilution caused by lab-grown diamonds and precipitously falling per-capita marriage rates in major consumer markets, the macro environment remains a structural driver for the industry.

During the pandemic-lockdown laden year of 2021 (and half of 2022), diamond sales posted record results as trillions of dollars of government induced economic stimulus drove consumers on hard-luxury shopping sprees as the service economy was effectively shuttered. Given the strong emotional underpinnings, diamonds outperformed the larger luxury category as consumers sought especially meaningful gifts for their loved ones amidst fear and uncertainty.

However, the aggressive economic stimulus that drove windfall sales subsequently led to a generational surge in inflation.

Inflation boosted the cost of living, but also asset prices, including real estate, stocks and private business valuations, adding fuel to what had already been a multi-decade spurt in wealth disparity. The term “K-shaped economy” emerged as a popular way to describe the continued growing wealth of the “haves” and the relative depletion of wealth of the “have nots.”

In 2026, news narratives have shifted to the AI revolution and the war in Iran, however, the effects of both developments will likely further compound the wealth gap trend. Technology stocks and energy prices are both soaring – the former a wealth driver for those with equity portfolios, the latter a cost-of-living driver.

While luxury, and diamond jewellery in particular, tend to be somewhat insulated from this dynamic – as it is more of a considered purchase and tends to disproportionately benefit from the top-half of the “K” – the industry still relies on the more “aspirational” consumers to thrive, for example, the middle class in consumer-heavy economies like the US.

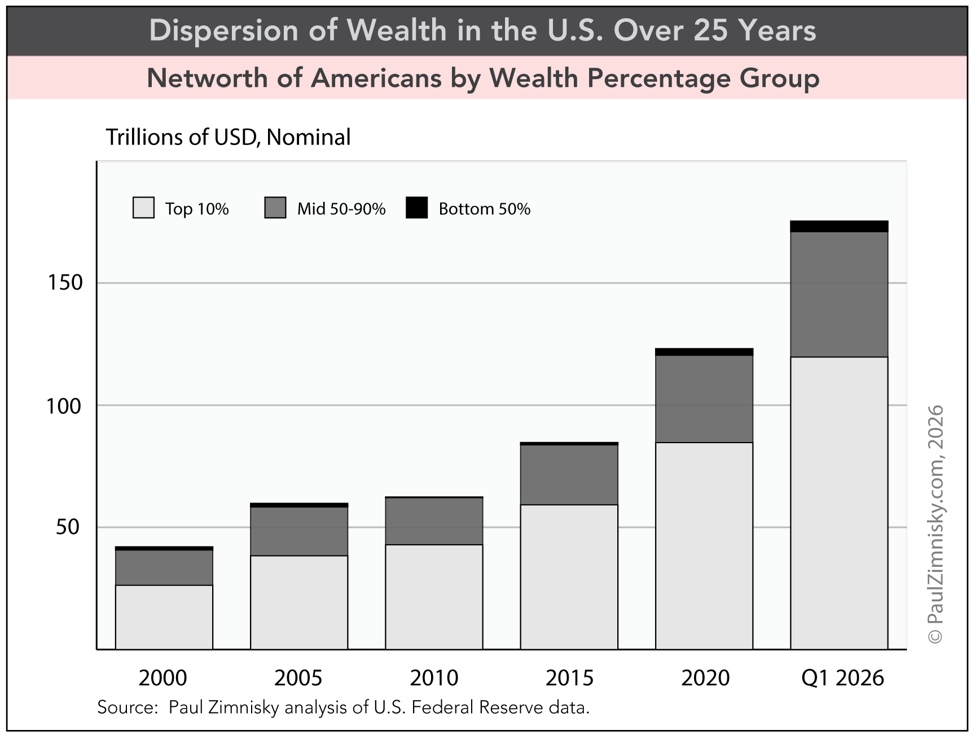

For context, the relative wealth of the top 50-90% earners in the US has dropped to 29% from 34% some 25 years ago – share that has directly moved to the top 10%, according to Paul Zimnisky analysis of US government data (see above chart). While only a mid-single digit percentage change, in a $19 trillion consumer economy like the US, it matters – especially when mixed with declining middle-class consumer sentiment that currently sits at the lowest level on record according to surveys referenced by the US Federal Reserve.

Nevertheless, capitalist economies are not zero-sum, and US economy has grown at a real (net of inflation) compound annual growth rate of around 2% over this period which has lifted the wealth of all groups of Americans, but the pace of growth of the bottom 90% has significantly lagged the top 10% in not just nominal but relative terms. This is a dynamic that has been clearly felt by the jewellery industry which is under pressure by shareholders to consistently grow sales at rates exceeding economic growth.

Notably, shares of LVMH, the world’s largest top-tier luxury conglomerate and parent of American icon Tiffany & Co., had the worst start to a year since going public in the late-1980s – the stock fell 28% in Q1 2026, erasing some $40 billion of market value, reflecting five consecutive quarters of declining sales. Earlier this year, management candidly said: “We try to attract entry-level customers…(and) when the economic climate is not so good, obviously, it’s firstly (these) customers who disappear.”

As another anecdote, Signet Jewelers, which is a long-time fixture of the middle-class jewellery market in the US, recently said it sees an opportunity to capture a bigger slice of the “upper-middle” class customer, with management adding, “maybe we’re not taking our fair share (of that market) today.” At the same time, Signet management acknowledged the opportunity in its core business: “A lot of brands have looked to move up and chase luxury…we really feel like space has opened up…in smart value, high quality at the right price.”

The company estimates that merchandise priced above $2,000 only represents a mid-single digit percentage of its unit volume but as much as 40% of its revenue. Signet sold almost $7 billion worth of jewellery last year and is the world’s largest seller of diamonds. Its overall sales grew 2% last year and management is forecasting moderate growth this year.

Talking with independents, the most obvious and common consequence to the larger industry has been a general decrease in order volumes but an increase in average order values which has supported overall sales. This is implicitly a result of wealthier consumers having even bigger budgets which can digest ever more expensive material prices, such a gold, while lower-wealth consumers outright cut discretionary spend.

This said, the current situation is somewhat unique for diamonds, given that prices are down some 50% from the highs in Q1 2022, using the Zimnisky Global Rough Diamond Price Index as a proxy. This comes as the U.S. Consumer Price Index is up 14% over the same period. Gold is up 125%. Thus, on a relative basis, it could be argued that diamonds look like an incredibly good value in the current environment.

In June, Signet CEO J.K. Symancyk said that the company is “taking advantage of softness” in diamond prices as a way to “balance” material costs. Symancyk also noted that Signet is “doubling down” on its current “focus surrounding natural diamonds.”

Paul Zimnisky, CFA is an independent diamond industry analyst and consultant based in the New York metro area. For regular in-depth analysis and forecasts of the diamond industry please consider subscribing to his State of the Diamond Market, a leading monthly industry report; an index of previous editions can be found here. Also, listen to the Paul Zimnisky Diamond Analytics Podcast on Spotify or Apple Podcasts for exclusive full-length conversations with special guests from the gem and jewelry industry. Paul is a graduate of the University of Maryland’s Robert H. Smith School of Business with a B.S. in finance and he is a CFA charterholder. He can be followed on X @paulzimnisky and on YouTube @paulzimnisky.

Disclosure: At the time of writing Paul Zimnisky held a long equity position in Brilliant Earth Group.