The diamond industry has faced a challenging year in 2023, with prices of both rough and polished goods falling significantly due to a demand slowdown and a supply glut. However, signs of a turnaround are emerging, as some segments of the market have seen a modest price recovery in the last two months, supported by coordinated supply curtailment efforts from the upstream and mid-stream sectors, as well as a better-than-expected holiday season. Paul Zimnisky, a leading independent diamond industry analyst and consultant, examines the factors that could drive a rebound in diamond prices in 2024, as well as the potential risks and opportunities for the industry.

In the very latter parts of 2023, certain categories of polished diamonds marginally (but notably) ticked up in price according to Paul Zimnisky data. This follows what has been a painful reversion year for both rough and polished goods coming off of a record period for diamond demand and prices in 2021 and 2022.

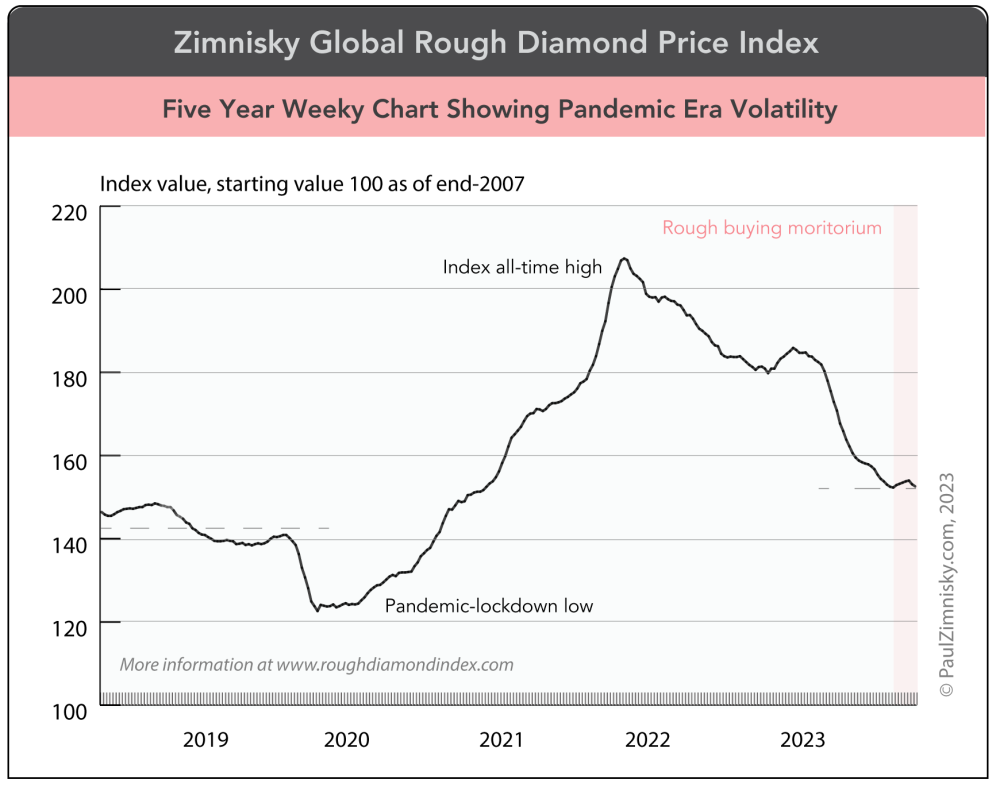

The pandemic-era demand surge led to real diamond supply shortages which were aggressively replenished by the trade in the latter half of 2022 and into 2023 just as the demand drivers were reversing – this hangover has materially weighed on prices.

For example, in 2023, a sample range of most commonly sold 0.3- to 1.5-carat (downstream) polished diamonds have sold off between 10% and 20% year-over-year – wholesale prices have been commensurately weak. Consolidated rough prices, as measured by the Zimnisky Global Rough Diamond Price Index, were down 16% year-to-date as of early-December – with prices now down over 25% from the all-time high reached in Q1 2022.

In September, a contingent of Indian diamond manufacturer organisations proactively coordinated a moratorium on rough diamond purchases for two months beginning on 15th October. The move was reminiscent of similar action taken in the early days of the pandemic economic stand-still and during the midst of global financial crisis a decade and a half ago. In the previous instances the move appeared to be successful in balancing supply with demand – which seemed to have proved effective in supporting diamond prices.

Today, the mid-stream’s efforts, as well as similar supply-curtailment support from prominent upstream players including De Beers and ALROSA, combined with a global demand picture that seems to be shaping up better than anticipated in the early-days of the 2023 holiday shopping season, seem to be supporting diamond prices once again.

Over the last eight weeks (through 2nd December), consolidated rough prices are flat – a technical break in the downtrend realised through most of 2023. Providing further encouragement, certain polished categories (downstream) are actually up a mid-single digit percentage over that time – especially higher-quality 0.3- and 0.5-carat goods, for example.

Looking ahead to 2024, a recovery in both rough and polished prices is anticipated.

Early in the year, demand support is expected with seasonal restocking, however, supply that was held back in late-2023 will likely come to market in effect offsetting any potential for meaningful upward price momentum. However, by mid-year a more notable recovery in prices is possible as a delayed effect of the mid-stream’s supply control efforts take effect – which could be compounded by the global supply impact of anticipated additional sanctions on Russian diamonds by Western nations.

Given a favourable supply picture, price fundamentals would still need to be supported by demand in 2024 – for example, via a “soft landing” in a global macro-economic sense, which financial markets are implying. Demand out of China, the diamond industry’s second largest end-consumer market remains a “wildcard” as the nation grapples with a secularly slowing economy and what some consider an emerging commercial and residential property crisis.

That said, historically the Chinese government has not shied away from executing stern economic policy support and stimulus measures when conditions warrant.

Paul Zimnisky, CFA is a leading independent diamond industry analyst and consultant based in the New York metro area. For regular in-depth analysis of the diamond industry please consider subscribing to his State of the Diamond Market, a leading monthly industry report; an index of previous editions can be found here. Also, listen to the Paul Zimnisky Diamond Analytics Podcast on iTunes or Spotify. Paul is a graduate of the University of Maryland’s Robert H. Smith School of Business with a B.S. in finance and he is a CFA charterholder. He can be reached at paul@paulzimnisky.com and followed on Twitter @paulzimnisky.

Disclosure: At the time of writing Paul Zimnisky held a long equity position in Lucara Diamond Corp, Brilliant Earth Group, Star Diamond Corp, Newmont Corp and Barrick Gold Corp. Paul is an independent board member of Lipari Diamond Mines, a privately-held Canadian company with an operating mine in Brazil and a development-stage asset in Angola. Please read full disclosure at www.paulzimnisky.com.