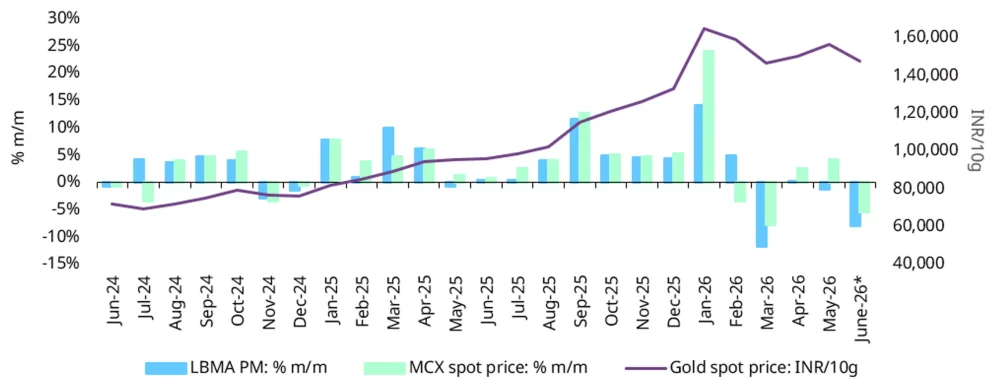

Gold’s gains ease

Gold’s returns have moderated from the highs seen in early 2026. As of 15 June, international and domestic gold prices were down 4.2% and 3.7%, respectively, from the end of May. However, y-t-d performance diverges: while international prices are broadly flat, domestic prices are up around 13.2%, largely reflecting the 9.0% increase in import duty in mid-May, and the 5.3% depreciation in the INR against the US dollar.

Elevated inflation concerns have led to expectations that major central banks will tighten their monetary policy; this has raised the opportunity cost of holding gold and pressured its recent performance. Improved investor risk sentiment and ETF outflows have weighed on investment demand too, contributing to the recent softening in prices.

Chart 1: Gold prices move lower

Month-end LBMA Price PM and domestic spot price changes and movement*

Source: Bloomberg, World Gold Council

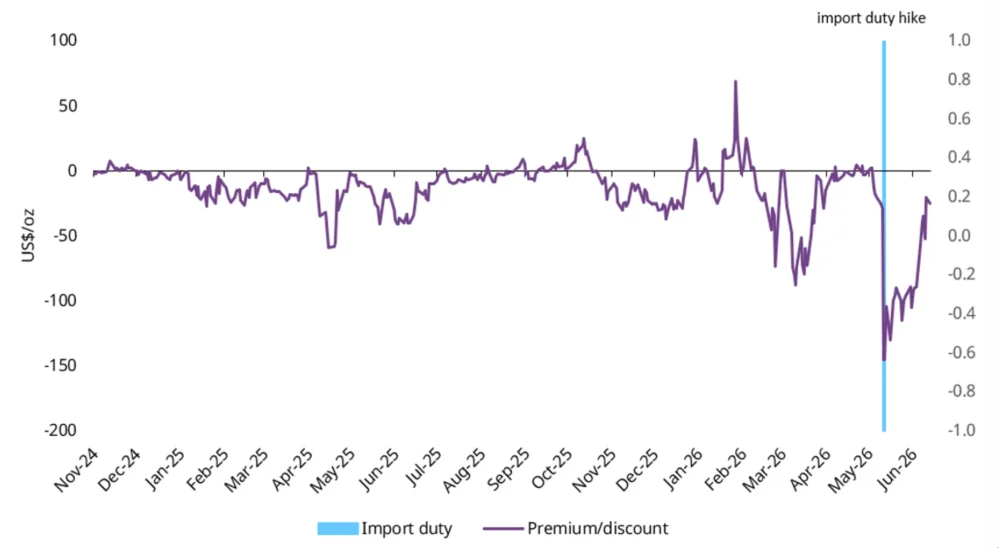

Deep discounts fade

Immediately after the mid-May import duty hike domestic gold prices moved into a deep discount to official or landed price,3 with the gap widening from an average of US$14/oz before the hike to nearly US$150/oz after. This sharp widening reflected a demand-supply imbalance: higher domestic prices prompted profit-taking, boosting supply even as physical buying remained under pressure. Adding to the supply were two further factors: the likely offloading by bullion dealers who imported gold prior to the duty hike, and the inflow of old gold jewellery exchanged for new. Since the second week of June, however, discounts have narrowed materially, falling to around US$25/oz as of 15 June, indicating the normalisation of the demand-supply dynamics. Lower availability of opportunistic supply, together with some pick-up in buying from select segments, likely contributed to the narrowing of discounts.

Chart 2: Discounts widen, then narrow

NCDEX gold premium/discount relative to the official domestic price*

Source: NCDEX, World Gold Council

Gold demand slows in off-season

Market feedback suggests that gold jewellery demand remained subdued through May and early June, a seasonally soft period that was further affected this year by an inauspicious period as per the Hindu calendar,4 reducing retail footfalls. Gold price volatility also led to a cautious, “wait-and-watch” approach among consumers across regions and segments. Industry feedback also suggests that bar and coin demand remained broadly stagnant, while new store openings slowed, reflecting the moderate mood across the trade.

Stakeholder interactions indicate that the Prime Minister’s appeal to limit gold buying weighed on discretionary purchases, particularly in urban markets, although its effect appears more limited in rural areas where there is relatively limited reach in social media and related messaging.

In response to this softening, retailers have focused on old-gold exchange transactions. Anecdotal evidence suggests that the share of exchange business has risen between 5–15%, and for some retailers has accounted for as much as 60-70% of sales. Retailers also note that some pockets of demand have emerged in recent days, fuelled by the pullback in the gold price and, in part, by expectations of policy measures aimed at limiting gold buying.

Overall, market participants broadly expect demand to remain soft through June and July before improving from August onwards as the seasonal demand cycle kicks in.

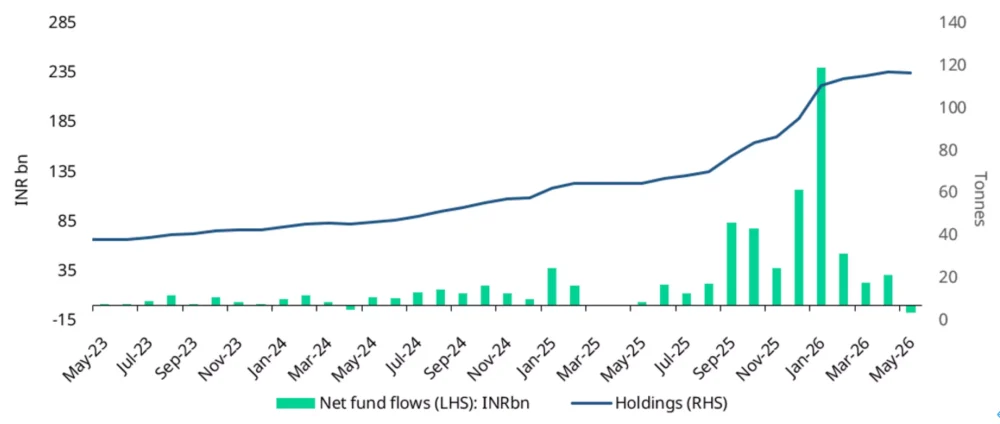

Gold ETFs: flows reverse in May

Indian gold ETFs saw a sharp reversal in May, mirroring the softer trend seen in global gold ETF flows. Domestic gold ETFs recorded their first monthly net outflow since April 2025: net outflows stood at INR7.25bn (US$76mn), the largest on record in rupee terms. Gross redemptions also rose to a record INR33.30bn (US$348mn), highlighting the scale of selling during the month. Despite this, overall holdings were broadly steady at 116.5t, in line with our estimates, while total AUM stood at INR1,846bn (US$19.3bn).

Outflows were likely driven by profit-taking following the mid-May import duty hike of 9% that pushed domestic gold prices and the traded price of ETFs sharply higher. INR gold prices rose by around 6% soon after the hike, prompting investors to lock in gains. This was also visible in folio data: investor accounts declined by 134,343 in May, the sharpest monthly fall on record, bringing the total number of active folios to 12.3mn. The high redemptions and reduction in folios suggest that some investors used the price rise to trim or exit their gold ETF positions.

But the outflows appear to have been short-lived. Flows turned positive again in early June, with net inflows of INR16.31bn (US$171mn) between 1–11 June, suggesting that investor interest in gold ETFs remains strong.

Separately, several fund houses5 introduced temporary limits on large investments into gold ETFs (with direct subscriptions capped at INR25cr/~US$2.6mn) and gold ETF fund-of-funds (lump-sum investments capped at INR10 lakh /~US$10.6k per PAN per calendar month). Although the fund houses have pointed to prevailing market and economic conditions, these measures come amid broader concerns around gold imports, external balances, currency pressures, and the Prime Minister’s appeal to consumers to curtail their gold buying. Given that large investors account for a sizeable proportion of AUM, the cap on investment could limit inflows into fund houses to some extent, although they can continue to buy from the secondary market where authorised participants and market makers continue to operate and provide liquidity. By investor category, the Association of Mutual Funds of India (AMFI) data shows that as of March’26, corporates accounted for 58% of gold ETF AUM, followed by high-net-worth individuals (HNI) 31%, and retail 11%.

Chart 3: Reversal of gold ETF flows

Gold ETF flows in INRbn, and total holdings in tonnes*

Source: AMFI, ICRA Analytics, CMIE, World Gold Council

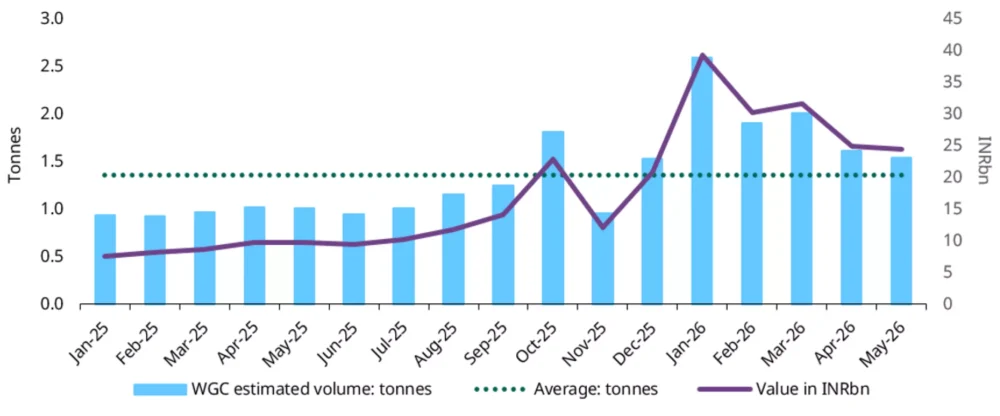

Digital gold buying slows, interest holds

Digital gold purchases through the Unified Payments Interface (UPI) moderated in both value and volume terms during May. Transaction values fell 2% m/m to INR24bn (US$256mn), while estimated volumes declined 5% m/m to 1.54t. Although purchases were well below the January peak – down 38% in value and 41% in volume – volumes remained above the 16 month average6 of 1.36t, suggesting that buying interest remains relatively strong despite the moderation. Digital gold also remained among the higher-transacting UPI categories.

Chart 4: Digital gold off highs

Purchase of digital gold, by value and estimated volume

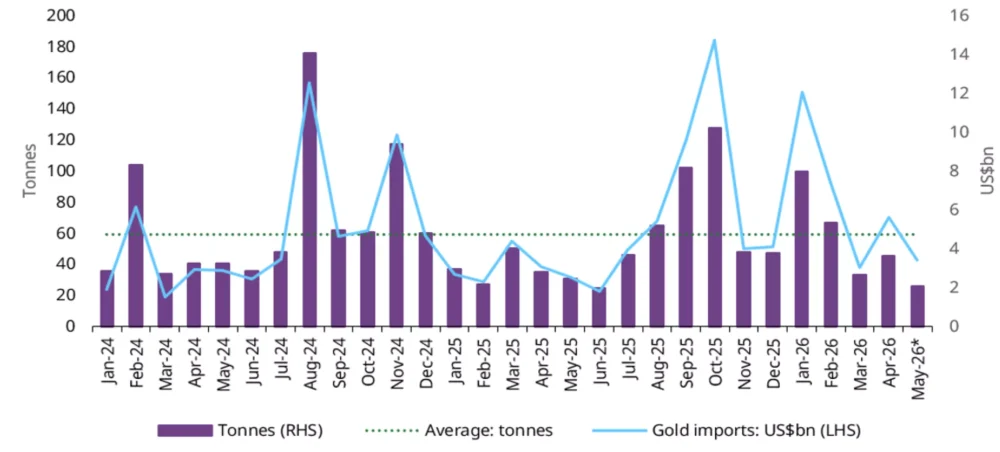

Duty-hike dents gold imports

Against the backdrop of the sharp mid May increase in import duties, gold imports declined 39% m/m to US$3.4bn, though they remained 34% higher y/y. In volume terms, we estimate imports to be in the range of 25–30t, notably lower than April’s 46t and the two-year average of 59t,7 reflecting a moderation in import volume as the higher duty structure took effect. As a share of total merchandise imports, gold accounted for around 5%, down from the elevated ~14% seen in January–February, and indicative of demand moderation.

Chart 5: Gold imports soften

Monthly gold imports in tonnes and US$bn*

Source: Ministry of Commerce and Industry, CMIE, World Gold Council