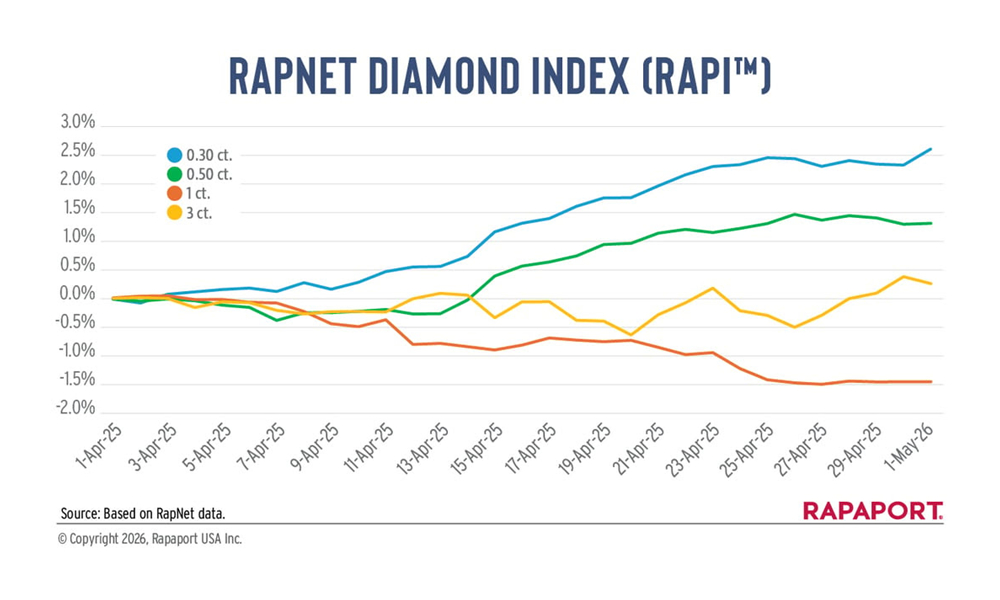

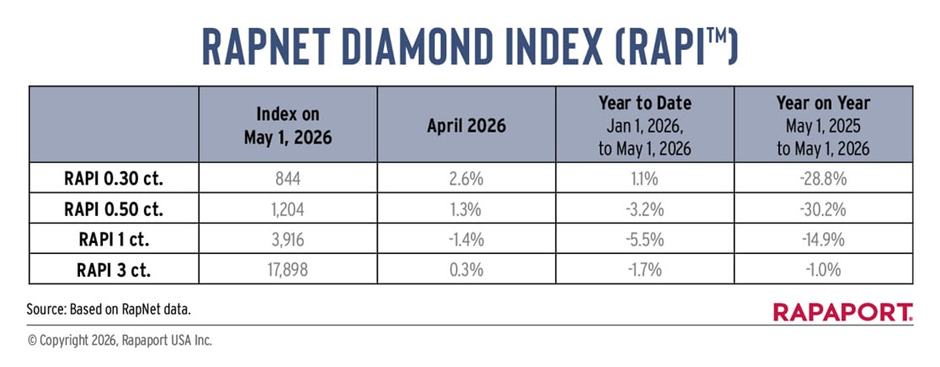

Small-sized diamonds posted a recovery in April, supported by production cuts and tightening inventories, while prices for 1-carat stones continued to soften, according to the latest data from the Rapaport Group.

Production cuts reduced inventories and supported prices for 0.30- and 0.50-carat goods. This was partly a correction following heavy price drops throughout 2025. Larger diamonds saw a more negative trend during the month, having fared better than small ones last year. Goods located outside the US performed more positively during April than those in America.

The RapNet Diamond Index (RAPI™), which tracks round D-H, IF-VS2 diamonds, fell 1.4% for 1-carat stones in April, an improvement from the 1.7% decline recorded in March. Meanwhile, prices for smaller goods rebounded, with the RAPI for 0.30-carat diamonds rising 2.6% and the 0.50-carat increasing 1.3%. The 3-carat category edged up 0.3%, maintaining recent stability.

Inventories of 0.30-carat and 0.50-carat RAPI-quality diamonds listed on RapNet declined 16% and 8%, respectively, during April. By comparison, inventory levels for 1-carat goods rose 1.5%.

Prices for SI-clarity diamonds, which are outside the RAPI’s scope, were steady or moderately up. Round, D-H, SI1-SI2 diamonds rose 1% by value for 0.30 carats, and 0.4% for 0.50 carats.

Retail demand remained steady ahead of the Las Vegas jewellery trade shows. US dealers reported consistent orders for diamonds above 2 carats, particularly in round and elongated fancy shapes, as Mother’s Day demand approached. Diamonds weighing 7 carats and above continued to see strong interest, especially D-flawless stones.

Market sentiment, however, remained affected by geopolitical tensions in the Middle East. RapNet data indicated that dealers shifted inventories of 1-carat and larger diamonds from Dubai to Antwerp during the Iran conflict in March.

India’s manufacturing sector also slowed ahead of the annual May summer recess, further weakening already subdued rough demand. India’s rough diamond imports in the first quarter fell 23% year-on-year to $2.14 billion, while import volumes declined 10% to 26.5 million carats.

Industry insiders also reported muted trading at De Beers’ April sight. Uncertainty continues over the planned sale of De Beers by Anglo American, with three private bidders currently in contention. Anglo American is expected to provide an update later this year.