Industry analyst PRANAY NARVEKAR examines the direct and indirect tax structures in place in the four major midstream centres – Belgium, Israel, Dubai and India.

Charles Dickens, in his famous book, The Tale of Two Cities, set his story in the turbulent events of the French Revolution and covered them from the perspective of two cities, namely London and Paris. While the events surrounding us are not quite that dramatic, the usually stable taxation scenario in the diamond pipeline has been in the midst of a few fairly radical changes in the last 1-2 years, as direct and indirect taxes at the four largest midstream centres get modified. Just like in any other industry, diamond companies will adjust their businesses to adapt to these changes. As they fully assimilate these modifications, it could alter the direction of the flow of goods in the pipeline.

Direct tax changes

The beginning of this year saw the tax policies in both Belgium (Antwerp) and Israel (Tel Aviv) change. Both countries had a similar income tax regime (except for differing rates) which had been put in place decades earlier. These countries levied a minimum tax on diamond companies, which was levied as a percentage of the turnover. If the actual tax liability, on the basis of the income or profit, exceeded this minimum amount, then the companies were liable to pay the higher amount.

While this was termed as a “turnoverbased tax”, it was never truly a turnoverbased tax. In a way, a certain amount of tax revenue would flow in for tax authorities while allowing the industry to reduce disputes regarding stock valuation and transfer pricing.

The tax rate in the minimum tax regime in Israel was set at a time when there was a flourishing polishing industry, along with stable diamond prices. The rates were set at a level which was realistic for those conditions which no longer exist.”

The tax rates were set in a period of stable and increasing prices, when most of the rough diamonds were sold through the De Beers. Post 2008, the diamond pipeline has seen a huge change, with price volatility being a part and parcel of the trade. Since 2011, the global price in dollar terms has reduced by nearly 25-30%. This drop directly cuts into the profitability of the industry.

In 2017, both Belgium and Israel changed their tax system in totally opposite directions. What was interesting was that the industry in both countries declared that this tax reorganisation was a big step forward, and it would go a long way in supporting the trade. While it may sound counter-intuitive as to how two totally diverse actions actually found acceptance with the industry, on closer examination, it looks obvious.

Belgium is primarily a trading location for both rough and polished diamonds. Belgium moved from the minimum tax system to a fully turnover-based direct tax system for diamond companies, which meant that companies only pay taxes purely based on turnovers. In doing so, the industry body negotiated a tax rate which is double that of the existing minimum rate! It actually was a smart move, as the government gains additional revenue, while allowing companies to also meet their International Financial Reporting Standards (IFRS) obligations as well as get a certainty on their taxation. The incentives for adjusting stock valuations disappears.

In an industry where the average net profitability has been below 1% of gross turnovers, after accounting for stock price movements, every fraction counts. This step allowed Antwerp to respond to the emergence of other trading locations like Dubai, which offered a taxation-free business climate. As long as companies do not misuse the provisions, it is definitely a huge positive step for Antwerp.

Israel on the other hand, shifted to a normal income tax regime, where taxes are levied on profits, as is prevalent in most jurisdictions. This meant that the minimum tax, which was levied on turnover does not need to be paid.

The tax rate in the minimum tax regime in Israel was set at a time when there was a flourishing polishing industry, along with stable diamond prices. The rates were set at a level which was realistic for those conditions which no longer exist. Polishing in Israel has gradually reduced and trading is taking more precedence. Profitability in the industry is also not assured any more. Hence it was a logical step for the industry to ask for the minimum rate tax regime to be dropped.

While this may be logical, the question is whether it is the best approach for the industry. With a profitability-based taxation, issues of transfer pricing and stock values become more critical. A 1-2% difference in stock prices can even wipe out the profits for the diamond company. While the diamond company might be able to claim losses and not pay any tax, it might be looked at with suspicion. Hence the ultimate success of this measure might actually depend on the view taken by the tax authorities.

Turnover tax for the Indian diamond industry?

A turnover tax for the industry has been debated for quite some years now. The Gem & Jewellery Export Promotion Council (GJEPC) had also worked in the past to try and bring in a turnover taxbased regime in India. However, most of the discussion with tax authorities ends up veering round to some sort of benign tax regime (i.e. some rate above which there would be less scrutiny), something similar to what Belgium and Israel had in place before the latest changes. I can imagine that a similar discussion would have transpired in both these countries as well.

The reason for the hesitance of the authorities to accept a pure turnover tax is the fear that the scheme could be used to avoid tax by diverting profits from other affiliated businesses. Additionally, there is the fear that the authorities would be perceived to be giving a tax break to the industry. Unfortunately profitability benchmarks from 2-3 decades ago are considered, while the industry currently struggles with profitability.

In reality, a turnover tax is actually one which might work best for the industry. From a government perspective, it could provide more stable revenues (compared to turnover, profits are more volatile) while also significantly reducing the workload and disputes arising out of stock and transfer pricing issues.

Turnover taxes are also quite similar to a Financial Transaction Tax. The latter has been discussed and used for centuries and is typically levied on every transaction and have been often considered to reduce volatility in financial markets. American economist James Tobin applied the same on currency transactions in the ’70s that went on to became famous as the Tobin Tax. Typically, the financial transaction tax is used to curb volatility and speculation and has been considered for more equitable tax collection. Economists also increasingly believe that a financial transaction tax is less susceptible to evasion in today’s connected world.

In India, the government went ahead and put in place a Securities Transaction Tax for transactions and trading on equity and derivatives exchanges. Imposition of the tax reduces the tax element and if held for one year, exempts long-term gains. The reason for this was to reduce the overall burden of administering the tax in these markets, but it also helped attract individuals and companies on the exchanges.

A turnover tax works for both the government and the industry when the business is primarily trading focused. The government is able to reduce tax collection efforts while also gaining lower volatility in tax payments. The industry is also able to operate more transparently through its business cycles without the fear of undue taxation. Over a 5-8 year period, the revenue gains and losses would probably balance itself out.

Indirect tax changes

On the indirect tax front, India implemented a new Goods and Services Tax (GST) from July, while the UAE is expected to implement Value Added Tax (VAT) from January 2018. Indirect taxes, whether GST or VAT, essentially help to avoid double taxation in transactions. However, funds paid for on the tax do get locked up for the inventory which is held.

In India it was hoped that diamonds trading and polishing would be excluded from the GST ambit, or fall under the zero-tax category as the product is primarily meant for export. However, the government decided to levy a 0.25% duty on rough diamonds and a 3% duty on polished diamonds, which brought it in line with all other gold and jewellery products. While the rate does not look too onerous, the primary concerns were focused on the procedures and the rules, especially for exports. Exporters finally started receiving some refunds for the duty paid only in November, meaning that monies had been locked up for over five months. Apart from this, companies with sizeable domestic business have also indicated that they have not got the full refund in some cases.

Teething troubles are being sorted out by the government, as they try to alleviate the problems faced by the industry. Currently there are limited capacities to polish diamonds outside India, and these issues are unlikely to cause any major shift in the business in the short term. In a longterm scenario, the issues with GST would be factored into the costs before decisions on capacities are taken.

The implementation of VAT in the UAE might pose a more serious challenge for Dubai. Dubai transformed into a major diamond centre over the last 10-15 years by facilitating ease of doing business. Bringing in a VAT regime will set Dubai back significantly.

At the very obvious level, VAT will affect the local sales as prices go up. Our research has shown that diamond consumers buy based on the value, and not really the carats. A higher price will effectively reduce the income of companies. Also, Dubai is a major buying centre for the GCC countries and India. VAT could change the balance between prices in Dubai and in their home countries and affect buying, considering that VAT refunds could be a while away.

In theory, VAT should not really affect B2B trading. In Dubai, large memo terms are quite normal, however VAT will increase the cost of this exercise. Companies who hold excess stocks in Dubai will have to factor in the additional fund requirements. In any case, reporting requirements will increase, and reduce the ease of doing business, which was the primary competitive advantage for Dubai. The actual impact will depend on how seamlessly the refund process functions.

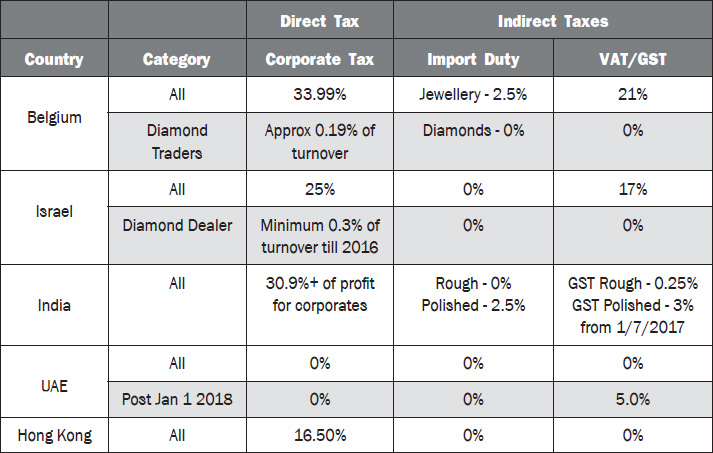

It is interesting to summarise the direct and indirect taxes for the industry in five major midstream centres.

An interesting observation is that apart from India and Dubai, in all the other four centres there are no indirect taxes or the industry has obtained a special dispensation. In both India and Dubai, these taxes are just taking root and their long-term effect still needs to be examined.

India should be differentiated because a sizeable portion of manufacturing is also to be considered. Diamond trading centres seem to flourish only when they operate in a zero indirect tax regime.

This seems to suggest that the Dubai might struggle to retain its position as a diamond trading centre, unless it comes up with a special policy dispensation to create a zero indirect tax policy for diamonds. I am given to understand that the trade bodies are making concerted efforts to try and make that happen. I hope a non-favourable outcome does not cause an exodus.

What does this all mean?

Currently, on the direct tax front, I believe that Belgium has created a more conducive environment for diamond companies, bringing certainty in the taxation and reducing taxation conflicts. For Israel, the industry might find that while taxes might be lower, in the long run, the cost of doing business might increase through increased scrutiny of transfer prices and operations.

When looking at indirect taxes, India is just starting to address exporters’ GST refund issues. However, the lack of largescale polishing facilities outside India will mean that diamond polishing will not be affected, although it might be subdued. For Dubai, the diamond industry will be severely affected, unless it gets an exemption from VAT. Dubai is purely a trading centre with little manufacturing. Indirect taxes lock up funds and slow down trading. As Dubai goes about setting the VAT processes, the need for blocking funds could simply overwhelm the benefit of zero income taxes.

Ultimately, the actions of diamond companies will boil down to costs. Most diamantaires consider direct taxes to be simply a cost of doing business and the impact of indirect taxes will also be similarly factored in. Other factors mentioned affect the ease of doing business, whose cost can also be worked in. The changes in tax essentially change this cost equation, which will ultimately determine the relative share of business done at the centres. For that we will have to simply wait and watch.

Pranay Narvekar is the CEO of the Gem & Jewellery KYC Information Centre. He is also a partner at Pharos Beam Consulting LLP. He is a leading expert on demand and supply, strategic, financial, and structural problems of the diamond industry. He has over 15 years of consulting experience, and had worked with Rosy Blue for nearly eight years. Narvekar has completed his B.Tech from IIT Bombay and Post Graduate Diploma in Management from IIM Lucknow.