After two consecutive quarters of year-on-year decline, the third quarter of 2018 saw gold jewellery demand in India grow by 10% to 148.8 tonnes, according to the World Gold Council’s (WGC’s) latest Gold Demand Trends report. While demand was firm during the quarter – virtually in line with the five-year quarterly average of 147.5 tonnes – the year-on-year growth should be viewed in comparison to a relatively weak Q3 2017, WGC noted.

India’s gold jewellery demand suffered in the third quarter of 2017, as some purchases were brought forward into Q2 in anticipation of the new pan-India Goods & Services Tax (GST). And in August 2017, gold jewellery retailers grappled with the extension of the Prevention of Money Laundering Act (PMLA) and its application to the gems and jewellery sector, WGC said.

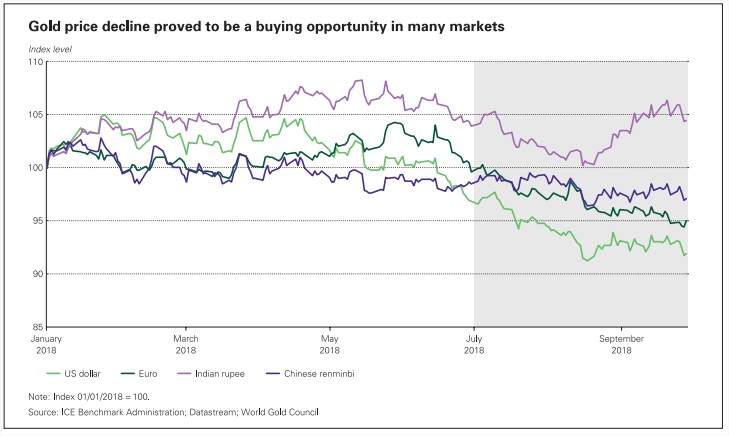

Third-quarter demand this year was boosted in early August when the local gold price dipped below R29,700/10g – the lowest level since January. This attracted bargain-hunting consumers who had been waiting for a good time to enter the market. Mid-August saw a sharp rise in the local gold price as the rupee depreciated against the US dollar. Outside the traditional festival and wedding season, demand eased towards the end of the month and into September. Jewellery demand was further dampened by the inauspicious period of Shraaddh (also known as Pitru Paksh), a time when gold purchases are put on hold.

Kerala’s third-quarter jewellery demand was impacted only marginally by floods. Heavy floods in the important gold-buying centre of Kerala during July and August negatively impacted gold demand; jewellers in the region reported muted sales during Onam, a kharif crop harvest festival. But demand was buoyed by marriages during the quarter, helping to offset the impact.

While the price dip in August was a helpful boost to the industry, it highlighted a structural challenge that jewellers face. Retailers’ main strategy to generating sales has been to compete on price. For example, offering price discounts or attractive gold-for-gold exchange programmes during festivals. While a few large, organised retailers have developed brands, little effort has been put into tailored marketing campaigns. As consumer tastes change, and competition from other product categories intensifies, the industry needs to ensure it develops products and marketing campaigns which meet potential consumers’ desires.

World jewellery demand

Price-conscious consumers took advantage of a declining gold price to boost Q3 demand. Demand for jewellery increased by 6% year-onyear, to 535.7 tones. India apart, China and several South-East Asian markets, too, saw respectable yearon-year increases, while demand in Iran, Turkey and the UAE fell significantly.

Chinese jewellery demand totalled 174.2 tonnes in Q3, a 10% increase over Q3 2017. Demand benefited from the Qixi and midAutumn festivals that took place during the quarter but sales were lacklustre during the National Holiday week as people chose travel over shopping, especially those in tier 1 and 2 cities. Jewellery sales during the Qixi festival (China’s equivalent of Valentine’s Day) were strong. Over recent years, retailers across all product categories have developed this festival as a buying occasion, a strategy that has proved especially effective among younger consumers. And despite the major annual jewellery fairs in Shenzhen and Hong Kong being slightly disrupted by Typhoon Mangkhut, several manufacturers reported healthy sales growth.

Middle Eastern jewellery demand remained under pressure in the face of geopolitical stress, down 12% year-on-year to 37.7 tonnes. Iranian jewellery demand saw the largest fall in the region for the second consecutive quarter, down almost 60% year-on-year in Q3. Year-to-date demand has shrunk by 36%, suffering under renewed economic sanctions and the steep decline in the rial.

In the UAE, jewellery demand fell to 6 tonnes (-13% year-onyear) as the market continued to feel the impact of the 5% VAT introduced last year, as well as a general economic downturn and fears over job security. Depreciation of the Indian rupee also affected demand from the important Indian expat community. The direction of jewellery demand in the UAE remains under question, particularly as some retailers registered losses for the first time, WGC pointed out.

Gold jewellery demand in the US remained buoyant, growing 4% to 28.3 tonnes in Q3. Economic confidence was high throughout the quarter, with the S&P 500 index rising by over 7%. This has helped boost discretionary spending on gold jewellery, especially plain yellow gold pieces. Retailers such as Tiffany’s and Signet have reported positive results in recent months, supporting a more optimistic outlook for the US jewellery market.

Europe-wide jewellery demand was little changed in the quarter, up 1% year-on-year to 12.7 tonnes.

Overall demand

Total global gold demand was steady in Q3 2018 at 964 tonnes, up just 6 tonnes year-on-year. Robust central bank buying and a 13% rise in consumer demand offset large outflows in gold-backed exchange-traded funds (ETFs). Global bar and coin investors took advantage of the price dip, with demand bouncing back to 298.1 tonnes, rising 28% year-on-year and 20% quarter-on-quarter.

Stock market volatility and currency weakness boosted demand in many emerging markets. China, the world’s largest bar and coin market, saw demand rise 25% to 86 tonnes. Iranian demand hit a fiveand-a-half year high at 21 tonnes.

Gold bar and coin demand in India was encouraged by lower prices and equity weakness. India’s bar and coin demand picked up in Q3 to reach 34.4 tonnes, but remains below its three-year average of 43.3 tonnes. In September the BSE Senex fell 6% and has continued to tumble in October, supporting demand for bars and coins, WGC noted.

Central bank gold reserves grew 148 tonnes in Q3 2018, up 22% year-on-year. This is the highest level of net purchases since 2015, both quarterly and year-to-date. The quarter was particularly notable due to a greater number of buyers. After minor purchases over recent months, the Reserve Bank of India (RBI) ramped up its buying in Q3, increasing reserves by a further 13.7 tonnes; this brings RBI’s year-todate purchases to 21.8 tonnes.

ETF outflows reached 103 tonnes in Q3 2018, the first quarter of outflows since Q4 2016. North America accounted for 73% of the outflows, fuelled by risk-on sentiment, a strong dollar and pricedriven momentum.

Alistair Hewitt, head of market intelligence at the World Gold Council, commented: “The physical market responded quickly when the gold price breached $1,200/ oz in August, with retail investors around the world diving into the market. And there are welcome developments in the central bank space. They’re buying a lot and we are seeing new central banks enter the market as they look to hedge their dollar exposure.

“The equity sell-off last week is a timely reminder of the threats stalking markets: valuations are stretched, debt levels are high, and rising rates and quantitative tightening pose risks that an allocation to gold can help hedge.”