The last two years have been an eye-opening experience for the diamond industry. Initially, the industry felt the effects of de-stocking in early 2009 and later the effects of re-stocking in 2010. Volumes and prices fluctuated wildly too. The industry, especially in India, was able to weather the storm rather well, with support from the government and banks, which were more accommodating than in other countries. The industry was able to increase its global share of business and was able to expand into newer category of goods, namely larger sizes. However, there is little understanding about what caused the crisis.

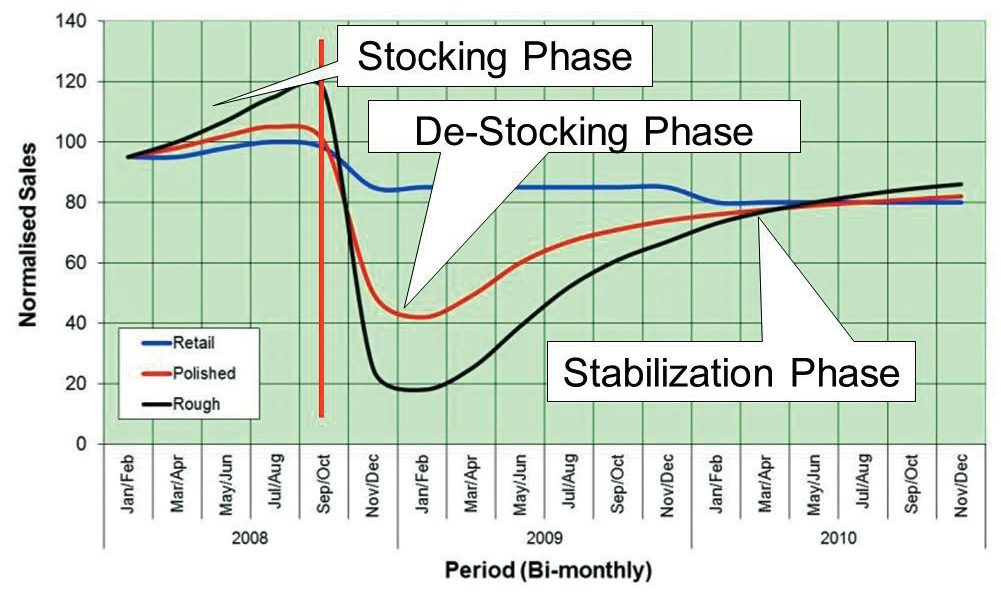

Industry Experience Curve

If we examine what the industry underwent, it is apparent that upstream areas like rough and manufacturing were affected more severely than others. Words used to describe this phenomenon include de-stocking/re-stocking, ripple effect and bull-whip effect. The pattern clearly suggested that the industry behaved exactly like any other. This phenomenon is the result of perfectly rational people making sound business decisions. But sometimes, even rational behaviour amplifies volatility up the pipeline.

It is important to understand why our industry is inherently vulnerable to such volatility, which increases as we move from retail demand to polished demand to rough demand. It is best explained by a simple example.

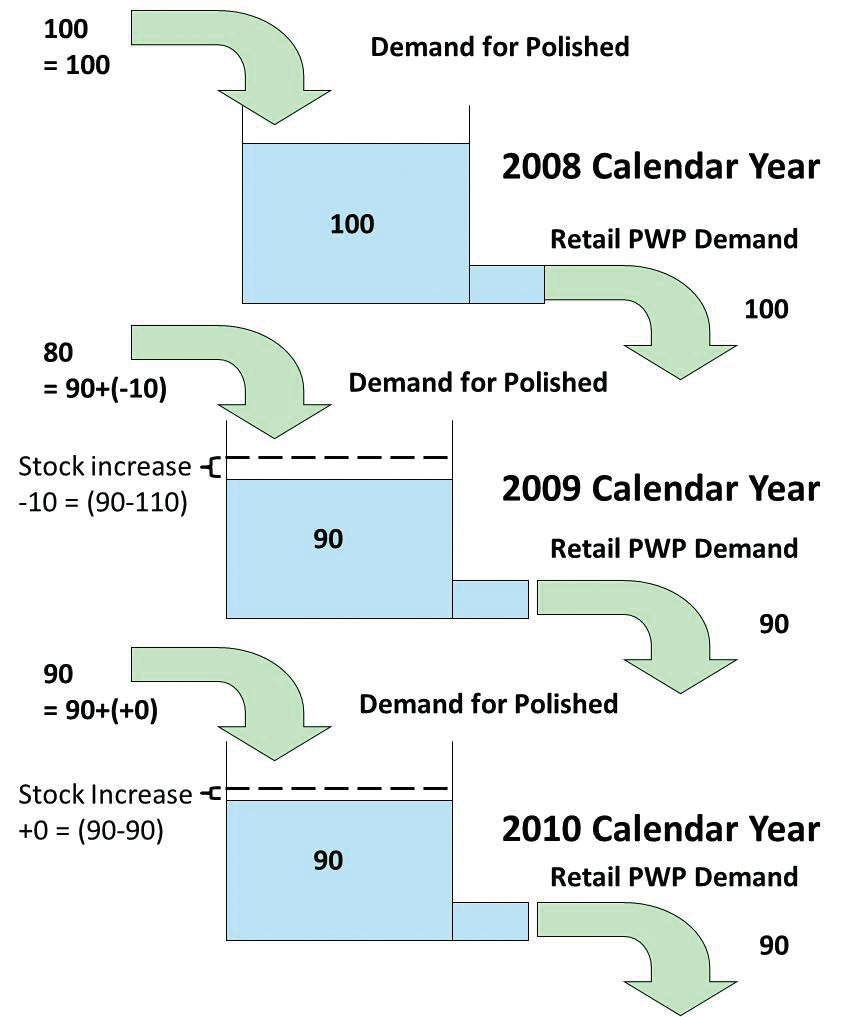

Let us consider a retailer who needs to buy 100 million-worth of diamonds. He is operating in a developed market and expects 1 inventory turn. Hence at the beginning of the year, the retailer will carry 100 million of stock in order to meet expected sales. But all of a sudden, external events change the world view, making customers less inclined to buy. The retailer’s expected sales are revised downward by 10%, and he reduces his expected diamond requirement to 90 million, assuming he maintains the same margin on the goods.

Being a sound business person, the retailer will want to bring down stock levels to 90 million, say by the end of one year. Hence, his diamond requirement will now be 90 million (sales) + 90 million (future stock) = 180 million. Against this, he is currently holding a stock of 100 million, implying that he will purchase only 180 million (requirement) – 100 million (current stock) = 80 million of diamonds. Rational business decisions will also demand that the reduction in purchase is upfront, further increasing the severity of the drop. Hence, the polished manufacturer will see a drop in demand of 20%, as a result of the 10% drop in retail demand.

Let us extend this ripple effect further down the chain to rough. Let us say that the polished manufacturer targets a 1.33 inventory turn. It means that for 100 million of normal polished sales, 75 million of stock of equivalent polished would be held. When this expected demand drops to 80 million, targeted stock would be reduced to 60 million. Hence the polished manufacturers will require 80 million (sales) + 60 million (closing stock) = 140 million against which he already has a stock of 75 million (opening stock). Hence the manufacturer will only buy rough equivalent to 65 million of polished, a reduction of 35% from the normal. These reductions would also be more severe upfront, as warranted by common business sense, showing a steep demand drop upfront.

A simple analogy to explain the above for polished goods will be to compare retail polished wholesale prices (PWP) demand, retail stocking and wholesale polished demand to a water tank. The accompanying chart shows how polished demand can increase in the third year simply because restocking kicks in, even when considering that the retail demand remains constant.

Water Tank Analogy for Stocking and De-Stocking

In the real world, stocking itself is dependent on availability of finance and the sentiment of diamond, which means that in times of stress, stock levels are reduced below normal stocking, further reducing the demand. During times of increasing demand and credit availability, the reverse is true and stock increase can push up the polished demand above what is justified by the retail demand.

Impact on the industry

The industry faced precisely these pressures during the fourth quarter of 2008 and early part of 2009. Add to that, as credit tightened, the industry was forced to eliminate any excess stocking, further reducing rough demand, which bore the brunt of the actions.

As the industry moved into the middle of 2009 retailers started replenishment purchases, as they reached their target inventory levels. This helped stabilise prices. Getting into the latter part of 2009, the industry realised that the fall in retail sales were not catastrophic. They also started to replenish their stocks and some even increased their stocks. This was especially true in India as more manufacturers ventured into larger size goods. To start trading in these goods, manufacturers had to build up inventories, which were also higher in value. This helped greatly increase the rough demand in 2010.

Looking ahead to 2011

Polished and rough demand now appears to be stable and in line with the retail demand. However there could be a mismatch in specific types of goods between demand and availability. Indian manufacturing capacity reduced during the crisis and rebuilding the same is an expensive and slow process. Companies have moved to larger goods to maximise revenues, which initially pushed up the demand for these goods. This also led to the neglect of smaller goods, which are currently in short supply.

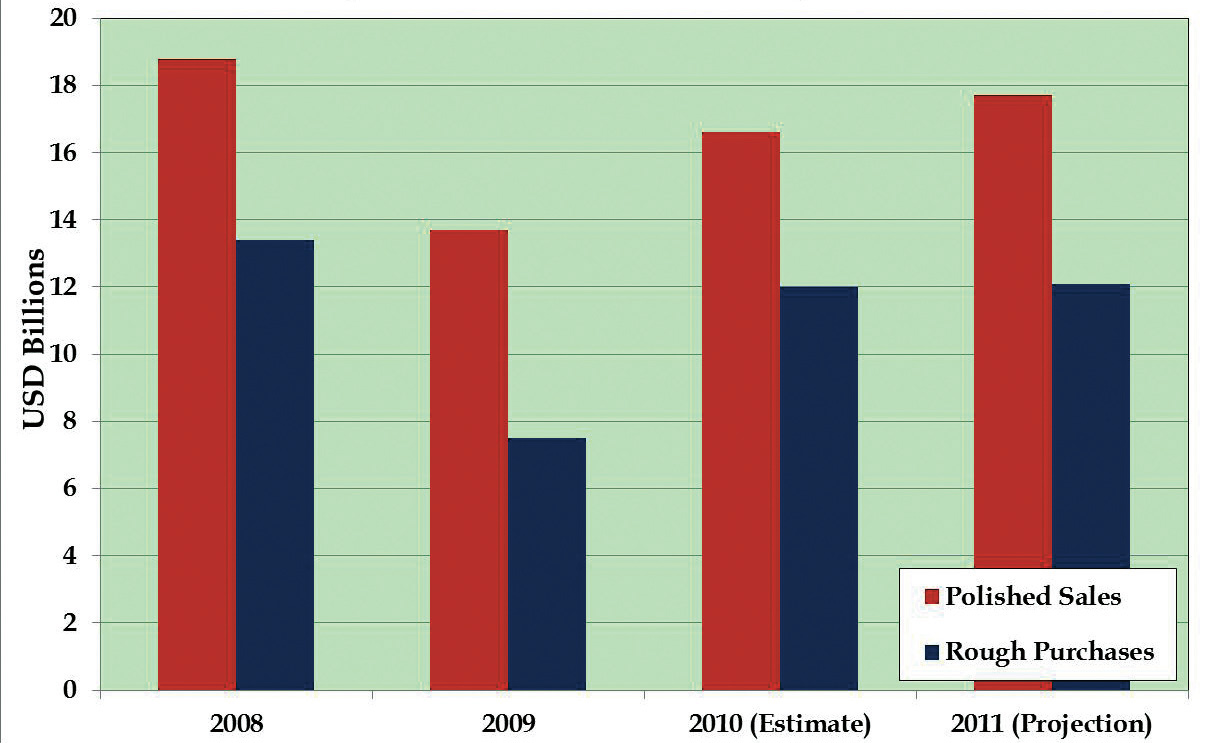

Industry-wide Polished Sales and Rough Purchase Estimates and Projections

The model serves as a good basis to understand the overall industry demand and supply. Prices, on the other hand, are much more specific to individual goods and have a dynamic of their own. Projecting prices is also much more difficult, as actions of individual companies and countries could greatly affect them in the short run.

Point to ponder

Generally, a drop in stock values is realised explicitly, either in a one-time write off or through negative margins on sales. However, the impact of stock appreciation is not easily recognised and also not fully realised for various reasons varying from customer reluctance to prices being reset only periodically. So the question you need to ask yourselves as traders is will your business be profitable even if prices were to remain static for one year, that is, without any stock appreciation?