India registered its highest ever fourthquarter gold jewellery demand as relatively stable prices and improving economic conditions paved the way for growth, the World Gold Council (WGC) said in its latest Gold Demand Trends report. Indian jewellery demand recovered in Q4 2017, gaining 4% yearon-year to reach 189.6 tonnes, the highest fourth quarter in the WGC’s 17-year series.

India’s gold jewellery demand for the full year 2017 grew 12% to 562.7 tonnes versus 504.5 tonnes in 2016. India’s investment demand (bar and coin) rose 2% to 164.2 tonnes, putting the country’s total consumer gold demand (jewellery + bar and coin) at 726.9 tonnes, an increase of 9%.

Rupee gold prices trended lower during the quarter, which proved positive for demand, WGC said. The economic backdrop helped bank loan growth. Demand was further supported by festival demand, the government’s decision to remove anti-money laundering regulation from jewellery, and improved rural sentiment.

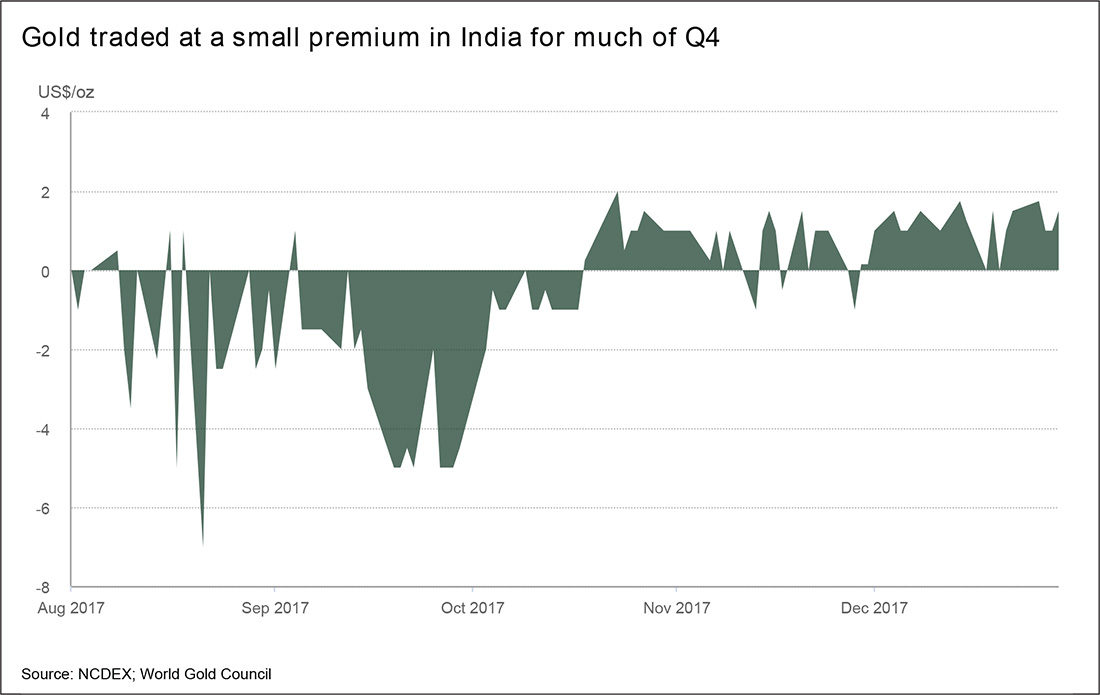

“In contrast with Q3, when the price was in almost permanent discount, the local price traded at a small premium to the international price for much of Q4. October started well: the Dhanteras festival – marking the start of the wedding season – coincided with a dip in prices, which encouraged demand,” the WGC said.

The report stated that Indian gold demand received an added boost when the government granted the gold market an exemption from anti-money laundering measures. The Prevention of Money Laundering Act (PMLA), which was extended to the gems and jewellery sector in August 2017, had negatively affected jewellery demand as consumers and retailers were faced with a heavy administrative burden to prove the veracity of cash transactions. The effect was most pronounced in rural areas, where cash is widely used. The removal of the PMLA from the sector therefore had a positive impact on demand, it added.

“Rural sentiment picked up in the fourth quarter, supporting a key element of the market. Consumers in rural areas are the driving force behind Indian gold jewellery demand. Positive sentiment among this demographic is quickly felt in certain areas of the economy, the gold jewellery market being one of them.

“Sentiment was vastly improved compared with Q4 2016, when these consumers were struggling with the drastic and unexpected demonetisation of the economy. A 6% increase in the minimum support price for kharif crops also helped. Strong growth in tractor sales bears out this improvement: Mahindra & Mahindra Ltd.’s Farm Equipment Sector (the world’s largest tractor manufacturer) announced 32% year-on-year growth in tractor sales during November and are upbeat in their outlook.”

The WGC said that organised retailers were able to increase their share of the jewellery market as they were best equipped to transition to the Goods and Services Tax (GST) system. “Looking forward, we expect a continued recovery in demand as the market increasingly accepts, and adapts to, GST. And the relative outperformance of chain stores and organised retailers is, in our view, likely to be a key feature of this recovery,” it stated.

International markets

Global full-year gold jewellery demand increased by 4% to 2,135.5 tonnes, the first year of growth since 2013. Demand for gold jewellery gained momentum in the final quarter of 2017, growing 3% year-onyear to a two-year high of 648.9 tonnes. A corresponding increase in full-year demand was primarily driven by recovery in India, the US and China. These three markets together accounted for 78 tonnes of the 82- tonne increase in global full-year demand.

China’s 6% growth in Q4 contributed to a 3% rise in annual jewellery demand – the first yearly increase since 2013. Demand for the full year increased to 646.9t thanks to a strong H2, which was buoyed by holiday purchases and a retail trade more effectively targeting consumer needs. WGC said the trend for lower-weight, better designed, highermargin ‘premium’ gold jewellery products continues to gather momentum in China.

Annual jewellery demand in the US gained 3% to 122.1 tonnes, as Q4 demand reached an eight-year high. The improving economic environment that buoyed sentiment – and demand – in Q3 continued to lift the market in the final quarter. Demand of 46.1 tonnes was the highest fourth quarter figure for US jewellery since 2009.

Online sales accounted for a growing share of jewellery demand, which played to the strengths of the larger, higher-end retailers. Tiffany & Co., for example, reported 8% growth in their holiday season sales. Luxury retail analysts at Cowen & Co confirmed that they remain enthusiastic on Tiffany in part because of their ‘tasteful blending of stores and online which should result in less friction in the buying process…’ In contrast, lower-end, massmarket retailers have suffered.

In 2017, Europe saw a third consecutive annual decline in jewellery demand, with losses persistent throughout the year. The 3% drop in regional demand (from 76.1 tonnes to 74 tonnes) was largely due to weakness in the UK market, which remained troubled by Brexit concerns. The lower-end of the market was worst hit, with 9-carat jewellery seeing the largest losses. Demand in the 22-karat niche was contrastingly resilient. Italian demand was also softer, although regional differences were noted: better than expected demand in northern Italy alleviated losses in the more traditional south.

Middle Eastern demand recovered in Q4, but H1 losses dominated: annual demand was down 1% year-on-year. Iran was the strongest performer in 2017: Q4 was its tenth consecutive quarter of year-onyear growth. Annual demand gained 12% to 45.4 tonnes, the highest since 2013. But the market lost momentum in the fourth quarter as worsening US-Iranian relations undermined consumer sentiment.